⏱️ Key Takeaways (7-min read)

Your CIBIL score is directly impacted by unpaid dues

Credit card debt in India carries 30%–45% annual interest

Minimum payments are designed to keep you in debt longer

Smart repayment strategies can cut years off your timeline

Advanced tactics like balance transfer & consolidation reduce costs

Table of Contents

- Introduction

- What Is Credit Card Debt (Simple Explanation)

- Why Credit Card Debt Is So Dangerous

- Real Indian Case Study

- Step-by-Step Plan to Get Out of Credit Card Debt

- Advanced Strategies to Eliminate Debt Faster

- Impact on Your CIBIL Score

- Smart Habits to Stay Debt-Free Forever

- Psychological Side of Debt (Underrated but Critical)

- When Should You Seek Professional Help?

- Conclusion

- FAQs

Introduction

Here’s the uncomfortable truth.

Credit cards are one of the most useful financial tools in India…

but also one of the easiest ways to fall into a debt trap.

A swipe today can quietly turn into a long-term burden tomorrow.

And because interest compounds monthly, even a small unpaid balance can grow faster than your salary.

But here’s the flip side:

If you understand how the system works, you can beat it.

This guide breaks down everything you need to know about credit card debt in India—from basics to advanced strategies—with real ₹ examples and actionable steps.

What Is Credit Card Debt (Simple Explanation)

Credit card debt occurs when you don’t pay your total outstanding balance by the due date.

Instead, the unpaid amount is carried forward—and interest is charged on it.

₹ Example (Indian Context)

Amit from Hyderabad spends ₹60,000 on his card.

- Total bill: ₹60,000

- Minimum due: ₹3,000

- Remaining: ₹57,000

At ~3.5% monthly interest:

Interest in 1 month ≈ ₹2,000

Next month, interest applies again—on a slightly higher amount.

That’s compounding in action.

Why Credit Card Debt Is So Dangerous

1. High Interest Rates (The Silent Killer)

Most Indian credit cards charge:

- 3%–3.75% per month

- = 36%–45% annually

Compare that to:

- Home loan: ~8–9%

- Personal loan: ~12–18%

This is why credit card debt grows aggressively.

2. Minimum Payment Trap Explained

Paying only the minimum due gives a false sense of safety.

But here’s what actually happens:

- 70–80% of your payment goes toward interest

- Only a small part reduces principal

Result: Debt stays for years.

3. Compound Interest Works Against You

Every month:

- Interest gets added

- Next month’s interest is calculated on a higher amount

It’s like a snowball rolling downhill—getting bigger fast.

Real Indian Case Study

Neha, a software engineer in Bengaluru:

- Credit card dues: ₹1,50,000

- Monthly payment: ₹7,000

After 1 year:

- Paid: ~₹84,000

- Remaining balance: still ~₹1,20,000

She paid a lot—but barely reduced debt.

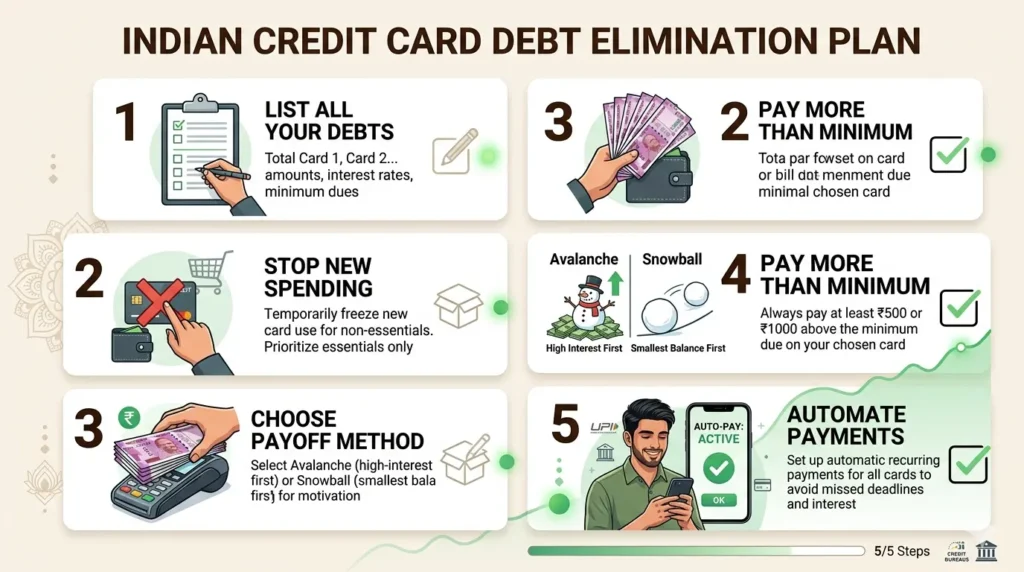

Step-by-Step Plan to Get Out of Credit Card Debt

Step 1: Stop Using Your Credit Card

This is non-negotiable.

- Switch to UPI or debit card

- Remove saved cards from apps

- Avoid “No-cost EMI” traps

You can’t fix debt while adding more.

Step 2: List All Your Debts

Create a simple table:

| Card | Outstanding | Interest Rate | Minimum Due |

|---|

This gives clarity—and control.

Step 3: Choose the Right Repayment Strategy

🔹 Snowball Method (Best for Beginners)

- Pay smallest balance first

- Builds confidence

Example:

- ₹15,000 → ₹40,000 → ₹90,000

🔹 Avalanche Method (Best for Saving Money)

- Pay highest interest first

Example:

- 42% → 38% → 30%

Saves thousands in interest.

Step 4: Increase Monthly Payments

Let’s compare:

- ₹5,000/month → 4+ years repayment

- ₹10,000/month → ~2 years

Doubling payment can halve your debt duration

Step 5: Cut Expenses Aggressively (Temporary)

Think of this as a short-term mission.

- Reduce Swiggy/Zomato orders

- Pause subscriptions

- Avoid shopping sales

Even saving ₹5,000/month makes a big difference.

Advanced Strategies to Eliminate Debt Faster

Now let’s move beyond basics.

These are pro-level tactics.

1. Debt Stacking (Hybrid Strategy)

Debt stacking combines:

- Avalanche (interest optimization)

- Snowball (psychological wins)

You focus on high-interest debt while clearing small balances quickly.

₹ Example:

Ravi has:

- ₹10,000 (35%)

- ₹80,000 (42%)

- ₹25,000 (30%)

Strategy:

- Clear ₹10K first (quick win)

- Then aggressively attack ₹80K

2. Balance Transfer Strategy

Banks offer:

- 0%–1% interest for 3–6 months

You move your debt to a new card.

Benefits:

- Lower interest temporarily

- Faster repayment window

Risks:

- Processing fees (1–3%)

- Interest jumps after offer ends

Only use if you can repay quickly.

3. Convert Credit Card Debt to Personal Loan

This is called debt consolidation.

Why it works:

- Lower interest (12–18%)

- Fixed EMI

- Clear timeline

₹ Example:

₹1,00,000 debt:

- Credit card: ~40% interest

- Personal loan: ~14%

You save ₹20,000+ in interest

4. Settlement vs Full Payment (Important Warning)

Some people consider settlement.

Let’s be clear:

❌ Debt Settlement

- Bank agrees to accept lower amount

- Remaining is written off

🚨 Risks:

- Severe CIBIL score damage

- Future loans become difficult

- Marked as “settled”, not “closed”

Use only as a last resort.

Impact on Your CIBIL Score

Credit card debt directly affects your credit score.

How it drops:

- High credit utilization (>30%)

- Missed payments

- Settlements

₹ Example:

Arjun had:

- CIBIL: 780

- Missed 3 payments

New score: ~650

This affects:

- Loan approvals

- Interest rates

- Credit limits

How to Improve It

- Pay on time (no exceptions)

- Keep usage below 30%

- Avoid frequent card applications

To fully master your finances, you should also read:

- How Credit Cards Work in India (Beginner Guide)

- What Is CIBIL Score & How to Improve It Fast

- Personal Loan vs Credit Card: Which Is Better?

- Best Budgeting Methods for Indian Salaries

- Emergency Fund Guide (₹50K to ₹5L Planning)

These topics help you prevent future debt—not just fix current problems.

Smart Habits to Stay Debt-Free Forever

Once you’re out of debt, your goal is simple:

Never go back.

Build These Habits:

- Pay full bill every month

- Keep spending under control

- Track expenses weekly

- Maintain emergency fund

Golden Rule:

If you can’t pay in full, don’t swipe.

Psychological Side of Debt (Underrated but Critical)

Debt is not just financial—it’s emotional.

Common Patterns:

- Stress spending

- “I deserve this” purchases

- Ignoring statements

Fix:

- Track spending awareness

- Delay purchases by 24 hours

- Focus on long-term goals

When Should You Seek Professional Help?

If:

- Debt > 50% of annual income

- You’re missing payments regularly

- You feel stuck despite efforts

Options:

- Credit counselling agencies

- Financial planners

- Structured repayment plans

Conclusion

Credit card debt feels overwhelming—but it’s not permanent.

With the right approach:

- You can reduce interest

- Speed up repayment

- Rebuild your financial life

Start today.

Not next month. Not next salary.

👉 Today.

Because the earlier you act, the less you pay.

FAQs

1. How long does it take to clear credit card debt?

Depends on your payment size, but typically 6 months to 3 years with a proper plan.

2. Is paying minimum due enough?

No. It keeps you in debt longer and increases total interest paid.

3. Should I take a personal loan to clear credit card debt?

Yes—if the interest is lower and you follow strict repayment discipline.

4. What happens if I don’t pay credit card bills in India?

-> Late fees + high interest

-> CIBIL score drop

-> Recovery actions

5. Can I negotiate credit card debt?

Yes, but settlement impacts your credit score. Use cautiously.