Key Takeaways

Personal Finance Fundamentals in India can change any time

Your financial story can change — anytime

Most financial problems come from lack of awareness, not low income

Debt builds silently when you don’t track money

Emergency fund + budgeting = foundation

Investing works only after financial discipline

Table of Contents

- My Story — How Lack of Financial Knowledge Led Me Into Debt

- What Personal Finance Really Means (Beyond Definitions)

- The Personal Finance Framework (Big Picture)

- Pillar 1: Budgeting (The System That Changes Everything)

- Pillar 2: Emergency Fund (Your Financial Safety Net)

- Pillar 3: Debt Management (The Most Misunderstood Area)

- Good Debt vs Bad Debt

- The Real Danger of Credit Cards

- The Debt Cycle Explained

- How to Break the Cycle

- Pillar 4: Saving — The Habit That Separates Stability From Stress

- Why Saving Feels Difficult (Real Reason)

- The Biggest Mindset Shift

- The “Pay Yourself First” System

- Where Should You Keep Savings?

- Real-Life Insight

- Pillar 5: Investing — The Engine of Wealth Creation

- Why Most Beginners Get Investing Wrong

- What Is Investing (Simple Definition)

- The Power of Compounding (This Changes Everything)

- Best Investment Options in India (Detailed)

- 1. Mutual Funds (SIP) — Best for Beginners

- 2. Public Provident Fund (PPF)

- 3. Stocks (Direct Investing)

- 4. Fixed Deposits (FD)

- Asset Allocation (Most Important Concept)

- When Should You Start Investing?

- Pillar 6: Income Growth — The Most Underrated Factor

- The Personal Finance Flywheel (How Everything Connects)

- Behavioral Finance — Why People Still Fail

- The 90-Day Financial Reset Plan

- Pillar 8: Insurance — Protection Before Wealth

- Pillar 9: Advanced Investing (For Long-Term Growth)

- Pillar 10: Financial Freedom (Realistic Indian Roadmap)

- Tools & Apps (India-Friendly)

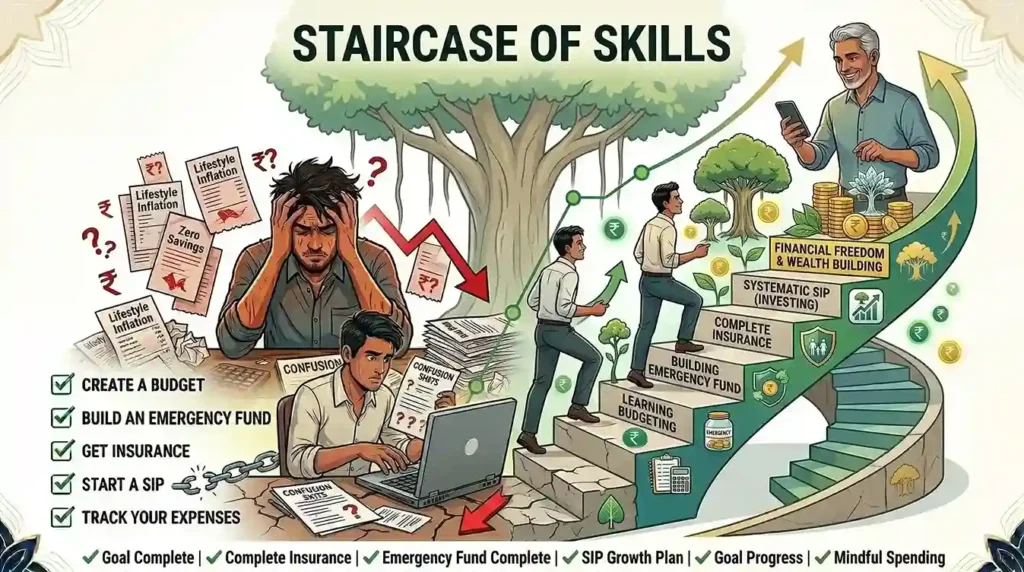

- The Ultimate Personal Finance Checklist

- Final Thoughts — The Truth About Personal Finance

- FAQs

Introduction — Why This Guide Is Different

Most personal finance articles will tell you:

- “Invest in SIP”

- “Save money”

- “Avoid debt”

But they miss something important.

👉 They don’t tell you why people fail even after knowing this

This guide is different.

Because it combines:

- Real-life experience

- Practical Indian examples

- Deep understanding of behavior

And most importantly—

👉 It starts where most people actually are: confused and struggling.

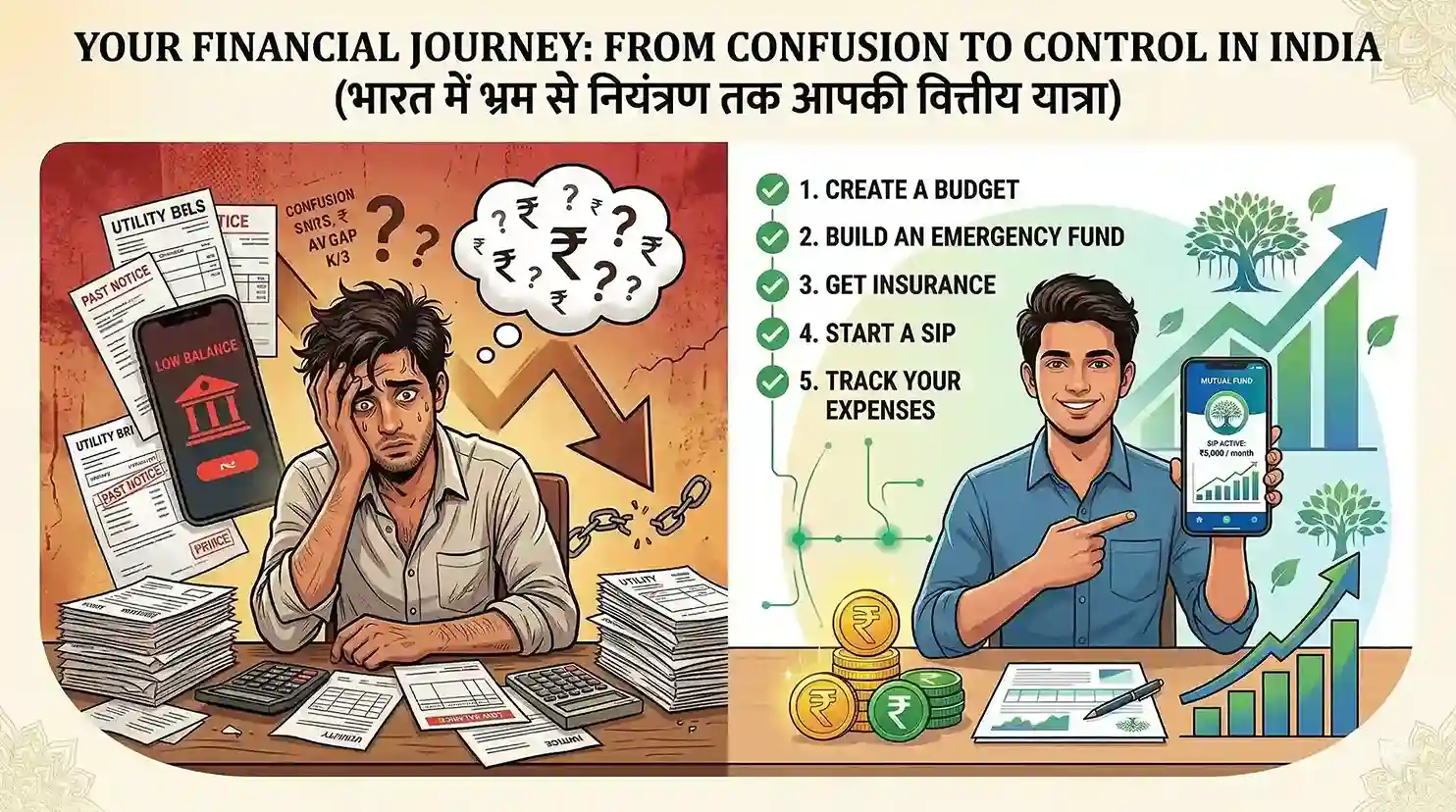

My Story — How Lack of Financial Knowledge Led Me Into Debt

Let’s not start with theory.

Let’s start with reality.

When I first started earning, my income was around ₹30,000 per month.

At that time, it felt like I had “made it”.

No more asking for money.

No more restrictions.

Just freedom.

The Lifestyle Shift (Without Realizing It)

Slowly, my spending increased:

- Ordering food frequently

- Going out on weekends

- Buying things I didn’t really need

- Paying small EMIs

Nothing felt extreme.

Everything felt normal.

The Invisible Problem

Here’s what I didn’t realize:

I wasn’t tracking anything.

So I had no idea:

- How much I was spending

- Where my money was going

- Whether I was saving anything

The Numbers (Reality Check)

Income: ₹30,000

Expenses:

- Rent + food → ₹15,000

- Lifestyle → ₹6,000

- EMI → ₹5,000

- Misc → ₹5,000

Total: ₹31,000+

👉 I was already in deficit.

The Entry Point of Debt

To manage this gap, I started using:

- Credit cards

- Buy Now Pay Later

- Small personal loans

At first, it felt helpful.

The Trap

Minimum payment = relief

Next month = bigger bill

And slowly:

- ₹20,000 became ₹30,000

- One loan became multiple

- Stress became constant

The Breaking Point

Despite earning every month—

👉 I had no money.

That’s when it hit me:

I didn’t have a money problem.

I had a knowledge problem.

What Personal Finance Really Means (Beyond Definitions)

Most definitions say:

“Personal finance is managing money.”

That’s incomplete.

Real Definition (Practical)

Personal finance is the system you use to:

- Control your money

- Avoid financial stress

- Build long-term stability

- Create freedom over time

Simple Analogy

Think of money like water.

If you don’t control its flow:

- It leaks

- It floods

- It disappears

Personal finance is building the pipes.

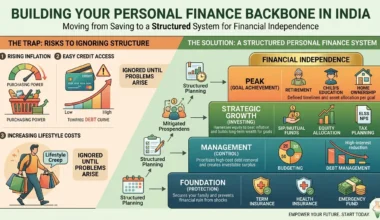

The Personal Finance Framework (Big Picture)

To truly master personal finance, you need to understand three layers:

Layer 1: Survival

- Budgeting

- Emergency fund

- Debt control

Layer 2: Stability

- Consistent saving

- Controlled spending

- Basic investing

Layer 3: Growth

- Wealth creation

- Multiple income streams

- Financial independence

👉 Most people skip Layer 1 and jump to investing.

That’s why they fail.

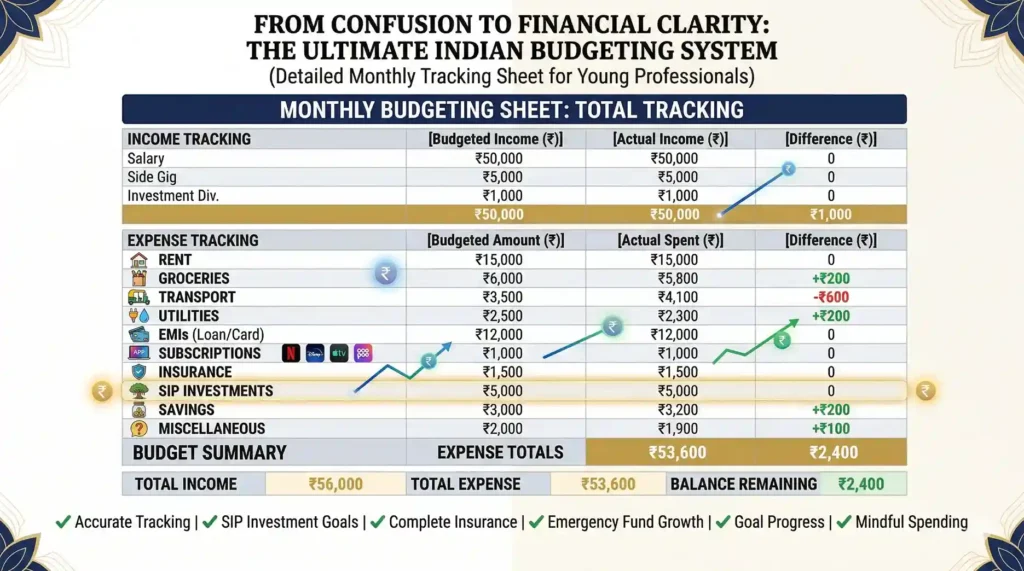

Pillar 1: Budgeting (The System That Changes Everything)

Budgeting is where everything starts.

Not investing. Not saving.

Budgeting.

Why Budgeting Fails for Most People

Because they think:

👉 Budget = restriction

In reality:

👉 Budget = clarity

The Psychology Behind Spending

When you don’t track money:

- Small expenses feel invisible

- Spending feels harmless

- Reality gets ignored

The ₹100 Problem

You spend:

- ₹100 on snacks

- ₹200 on delivery

- ₹300 on random items

Feels small.

But monthly?

👉 ₹6,000–₹10,000 gone.

Types of Budgeting Methods (India Context)

1. 50-30-20 Rule (Simplified)

- 50% Needs

- 30% Wants

- 20% Savings

2. Zero-Based Budget

Every rupee gets a job.

Income = Expenses + Savings = Zero leftover.

3. Reverse Budgeting

Save first → spend the rest.

What Actually Works (From Experience)

Forget complexity.

Start with this:

- Track expenses daily

- Review weekly

- Cut obvious waste

That alone can change your finances in 30 days.

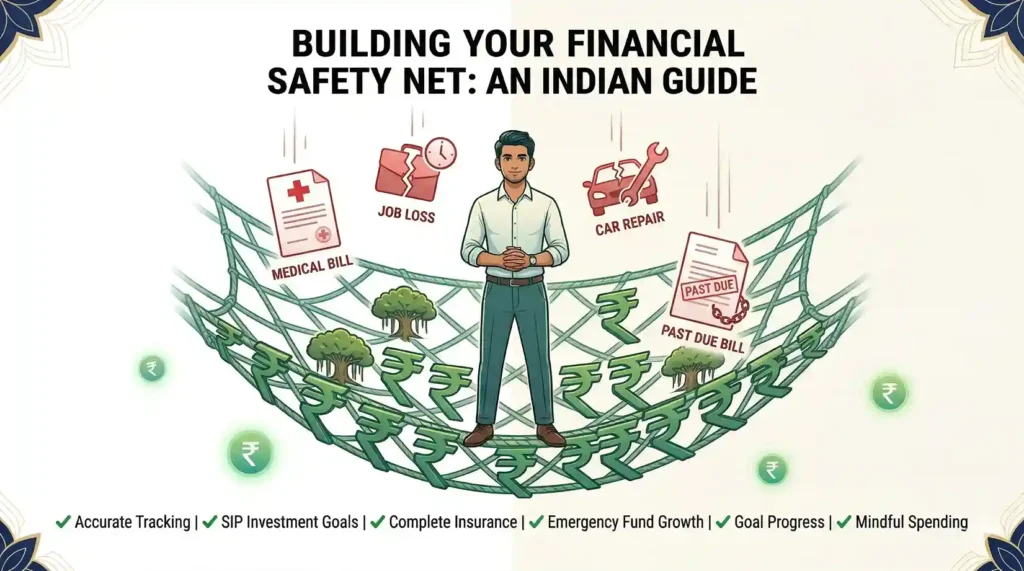

Pillar 2: Emergency Fund (Your Financial Safety Net)

This is the pillar most people ignore—

Until it’s too late.

Why Emergency Fund Is Non-Negotiable

Because life is unpredictable.

- Job loss

- Medical expenses

- Family emergencies

Without savings—

👉 Debt becomes your only option.

Real Scenario

Unexpected expense: ₹15,000

Without emergency fund:

→ Credit card

With emergency fund:

→ No stress

How Much Should You Save?

- Minimum: 3 months

- Ideal: 6 months

Where to Keep It

- Savings account

- Liquid funds

NOT:

- Stocks

- Long-term investments

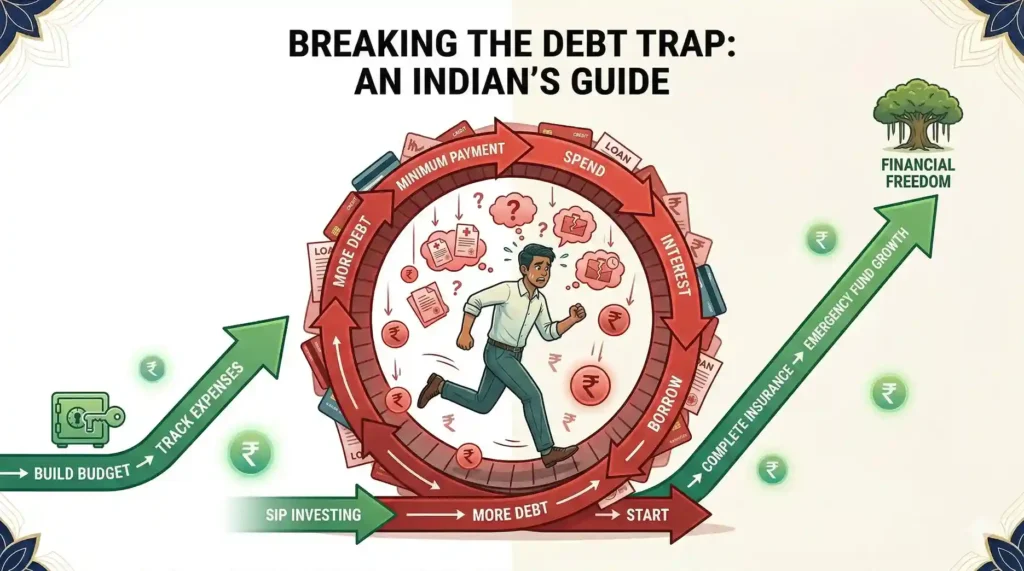

Pillar 3: Debt Management (The Most Misunderstood Area)

Debt is not always bad.

But most people use it incorrectly.

Good Debt vs Bad Debt

Good Debt:

- Education loan

- Home loan

Bad Debt:

- Credit cards

- Personal loans

- BNPL

The Real Danger of Credit Cards

Interest: 36%–42%

That means:

👉 Your money is working against you.

The Debt Cycle Explained

- Spend more than income

- Use credit

- Pay minimum

- Interest grows

- Repeat

How to Break the Cycle

- Stop new debt

- Pay highest interest first

- Track everything

- Build small savings

👉 This is where most people either fix their life… or get stuck for years.

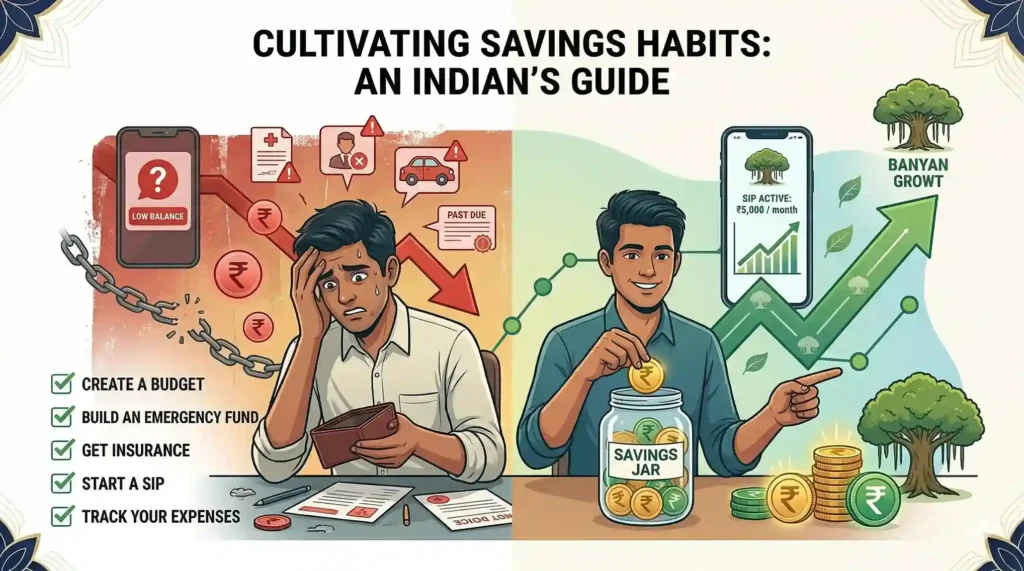

Pillar 4: Saving — The Habit That Separates Stability From Stress

Saving sounds simple.

But here’s the truth:

👉 Most people don’t fail because they can’t save

👉 They fail because they don’t prioritize saving

Why Saving Feels Difficult (Real Reason)

When you first start earning:

- You want to upgrade lifestyle

- You feel you “deserve” better things

- You think saving can wait

And slowly—

Saving becomes optional.

The Biggest Mindset Shift

This one change can fix your finances:

👉 Saving is not what’s left after spending

👉 Saving is what you take before spending

The “Pay Yourself First” System

This is what actually works in real life.

Example:

Income = ₹30,000

- Automatically move ₹6,000 to savings

- Live on ₹24,000

No decision-making required.

No willpower needed.

Where Should You Keep Savings?

Not all savings are the same.

1. Short-Term Savings (0–2 years)

- Savings account

- Liquid funds

2. Medium-Term Savings (2–5 years)

- Recurring Deposits (RD)

- Short-term mutual funds

3. Long-Term Savings (5+ years)

- Equity mutual funds

- PPF

Real-Life Insight

When I didn’t save:

- Every expense felt heavy

- Every emergency felt stressful

When I started saving:

- Even small expenses felt manageable

- Confidence increased

👉 Saving gives mental peace before financial growth

Pillar 5: Investing — The Engine of Wealth Creation

Let’s clear one thing:

👉 Saving protects money

👉 Investing grows money

Why Most Beginners Get Investing Wrong

Because they start with:

- Stock tips

- Crypto hype

- “Get rich quick” mindset

Instead of:

- Discipline

- Consistency

- Long-term thinking

What Is Investing (Simple Definition)

Investing means using your money to generate returns over time.

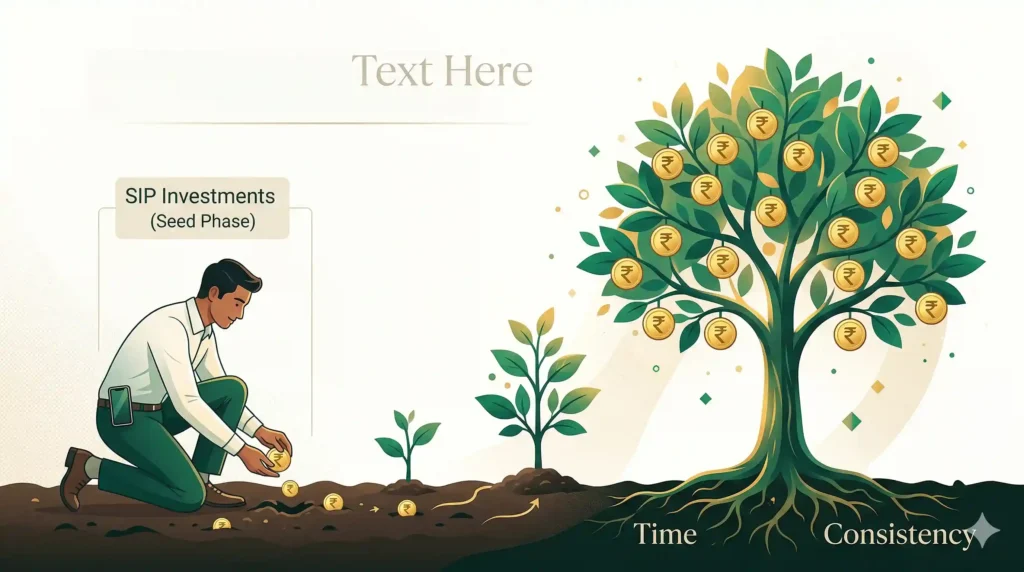

The Power of Compounding (This Changes Everything)

Compounding is when:

👉 Your returns start generating returns

Example:

₹5,000/month SIP

Return: 12%

- 5 years → ~₹4.1 lakh

- 10 years → ~₹11.5 lakh

- 20 years → ~₹50 lakh+

👉 Time matters more than amount

Best Investment Options in India (Detailed)

1. Mutual Funds (SIP) — Best for Beginners

Why?

- Professionally managed

- Diversified

- Easy to start

Types:

- Large Cap → Stable

- Mid Cap → Growth

- Index Funds → Low cost

Real Example:

Rohit invests ₹3,000/month

After 10 years → ~₹7 lakh

2. Public Provident Fund (PPF)

- Government-backed

- Safe

- 15-year lock-in

👉 Best for conservative investors

3. Stocks (Direct Investing)

- High risk

- High return

- Requires knowledge

👉 Not for beginners without learning

4. Fixed Deposits (FD)

- Safe

- Low return

- Good for short-term

Asset Allocation (Most Important Concept)

Don’t put everything in one place.

Example Allocation:

- 60% Equity (growth)

- 30% Debt (stability)

- 10% Cash (liquidity)

👉 This reduces risk and improves consistency

When Should You Start Investing?

Only after:

- Emergency fund ready

- Debt under control

- Basic budgeting done

👉 Skip this order → financial stress

Pillar 6: Income Growth — The Most Underrated Factor

Here’s something most finance advice ignores:

👉 You can’t save your way to wealth forever

At some point—

You must increase income.

Why Income Growth Matters

If you earn ₹20,000:

- Saving 20% = ₹4,000

If you earn ₹50,000:

- Saving 20% = ₹10,000

Same habit. Different results.

Ways to Increase Income (India Context)

1. Skill Upgrade

- Digital marketing

- Coding

- Design

- AI tools

2. Freelancing

- Content writing

- Video editing

- Social media

Even ₹5,000 extra matters.

3. Side Hustles

- YouTube

- Blogging

- Online selling

4. Job Switching

Often fastest way to increase salary in India.

Real Insight

When income increased slightly—

Everything became easier:

- Saving improved

- Investing increased

- Stress reduced

👉 Income is a multiplier

The Personal Finance Flywheel (How Everything Connects)

This is where most people finally “get it”.

Step-by-Step Flow:

- Income increases

- Savings increase

- Investments increase

- Returns grow

- Financial confidence improves

👉 Then cycle repeats

Behavioral Finance — Why People Still Fail

Even after knowing everything…

People still struggle.

Why?

1. Instant Gratification

- “I want it now” mindset

- Leads to overspending

2. Social Pressure

- Comparing lifestyles

- Trying to “match” others

3. Lack of Awareness

- Not tracking money

- Ignoring reality

4. Financial Illiteracy

- No knowledge of basics

- Blind decisions

👉 This is exactly how debt starts (as you experienced earlier)

The 90-Day Financial Reset Plan

If someone is struggling right now, this works.

Month 1:

- Track all expenses

- Stop unnecessary spending

Month 2:

- Build ₹10,000–₹25,000 emergency fund

- Start saving habit

Month 3:

- Start SIP (₹500–₹2,000)

- Plan debt repayment

👉 Simple. Practical. Effective.

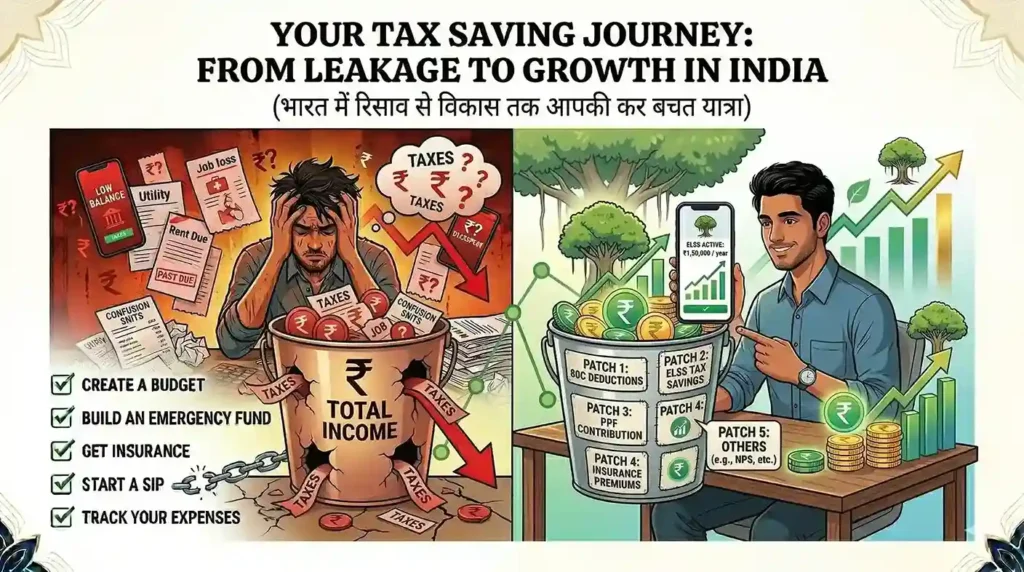

Pillar 7: Tax Saving in India (Without Confusion)

Let’s be honest.

Most people only think about tax saving in March.

That’s a mistake.

Why Tax Planning Matters

If you don’t plan taxes:

👉 You lose money legally.

Section 80C (Most Important)

You can save tax on up to ₹1.5 lakh/year

Popular Options:

- PPF

- ELSS Mutual Funds

- EPF

- Life insurance premium

What Most People Do Wrong

- Buy random insurance policies just to save tax

- Invest without understanding lock-in

👉 Best approach:

- Use ELSS + PPF combination

Section 80D (Health Insurance)

- Self + family → up to ₹25,000 deduction

- Parents → additional ₹25,000–₹50,000

👉 This is why insurance + tax planning go together

Simple Tax Strategy

- Start planning from April

- Invest monthly (not last minute)

- Choose tax-saving + wealth-building options

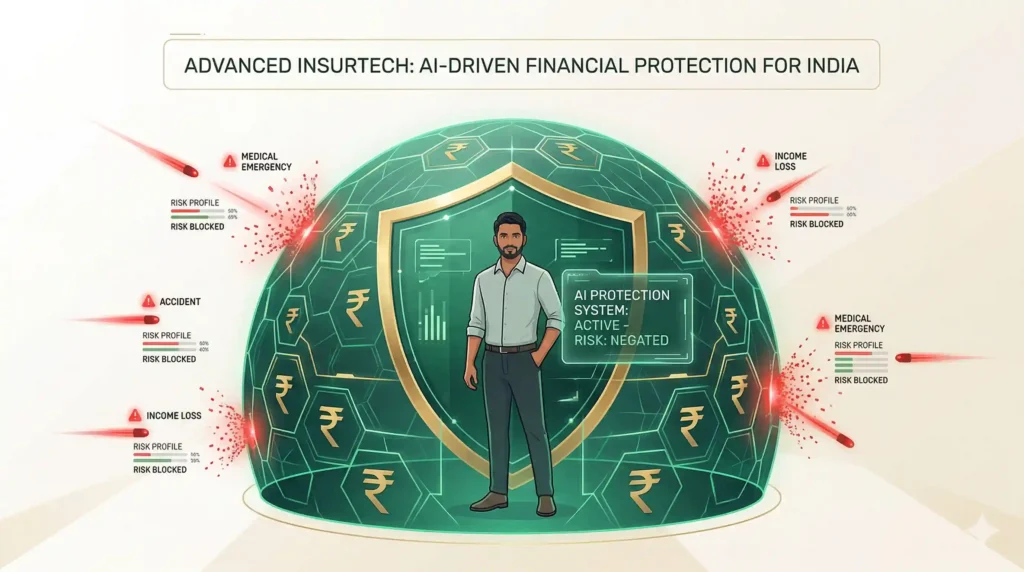

Pillar 8: Insurance — Protection Before Wealth

This is where most Indians make expensive mistakes.

What Insurance Is (And What It Is Not)

Insurance is:

👉 Protection against financial loss

Insurance is NOT:

👉 Investment

Must-Have Insurance

1. Health Insurance

- Covers hospital bills

- Minimum: ₹5 lakh cover

2. Term Life Insurance

- For earning individuals

- Example: ₹1 crore cover

Premium: ~₹500–₹1,000/month

What to Avoid

- ULIPs (investment + insurance mix)

- Endowment plans

👉 Keep insurance and investing separate

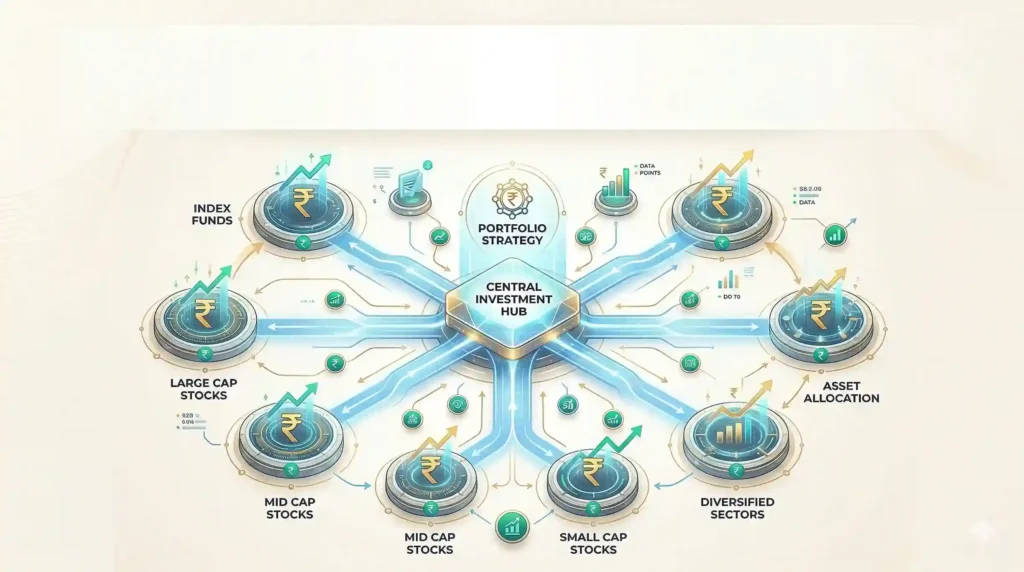

Pillar 9: Advanced Investing (For Long-Term Growth)

Once your basics are strong—

You can optimize.

Index Fund Investing (Powerful Strategy)

- Tracks Nifty 50 / Sensex

- Low cost

- Consistent performance

Why It Works

- No stock picking stress

- Long-term growth aligned with economy

Diversification Strategy

Don’t depend on one asset.

Example Portfolio:

- 50% Index funds

- 20% Mid-cap funds

- 20% Debt instruments

- 10% Gold

👉 This balances risk and return

Mistakes to Avoid

- Chasing “hot stocks”

- Overtrading

- Panic selling

Pillar 10: Financial Freedom (Realistic Indian Roadmap)

Financial freedom doesn’t mean:

- Being a crorepati

- Quitting your job instantly

Real Definition

👉 Having enough money to cover your expenses without stress

The Formula

Financial Freedom Number =

👉 Monthly expenses × 12 × 25

Example:

Monthly expense = ₹30,000

Freedom number = ₹90 lakh

How to Reach It

- Increase income

- Invest consistently

- Avoid lifestyle inflation

👉 It’s slow. But powerful.

Tools & Apps (India-Friendly)

To make this practical:

Expense Tracking

- Walnut

- Money Manager

Investing

- Zerodha

- Groww

Budgeting

- Excel / Google Sheets

👉 Tools don’t create discipline.

But they make it easier.

The Ultimate Personal Finance Checklist

Use this as your action plan:

Foundation

- Track expenses

- Create budget

- Save ₹10,000 emergency fund

Stability

- Build 3–6 month emergency fund

- Get health insurance

- Avoid new debt

Growth

- Start SIP

- Increase income

- Diversify investments

Optimization

- Save tax smartly

- Review finances yearly

- Set long-term goals

Final Thoughts — The Truth About Personal Finance

After everything—

Here’s what really matters:

You don’t need:

- A huge salary

- Perfect timing

- Complex strategies

You need:

👉 Awareness

👉 Discipline

👉 Consistency

And most importantly—

👉 You need to start

Because the biggest mistake is not:

- Debt

- Low income

- Wrong investments

It’s this:

👉 Doing nothing.

FAQs

What are personal finance fundamentals?

Personal finance fundamentals include budgeting, saving, investing, debt management, and financial protection.

How do beginners start personal finance in India?

Start by tracking expenses, creating a budget, building an emergency fund, and then investing through SIP.

How much should I save every month?

Ideally 20% of your income, but even 10% is a good start.

Is SIP better than FD?

SIP offers higher long-term returns, while FD provides safety. Both serve different purposes.

What is the biggest financial mistake?

Not tracking expenses and relying on credit.