how It Begins Quietly, Why It Feels Impossible to Escape, and What Actually Helps

Most people don’t get into debt because they are reckless.

They get into debt because they were trying to solve a problem.

A medical bill. A sudden expense. A period where income didn’t match responsibilities.

At that moment, debt feels less like danger and more like relief. Something that helps you breathe again — temporarily.

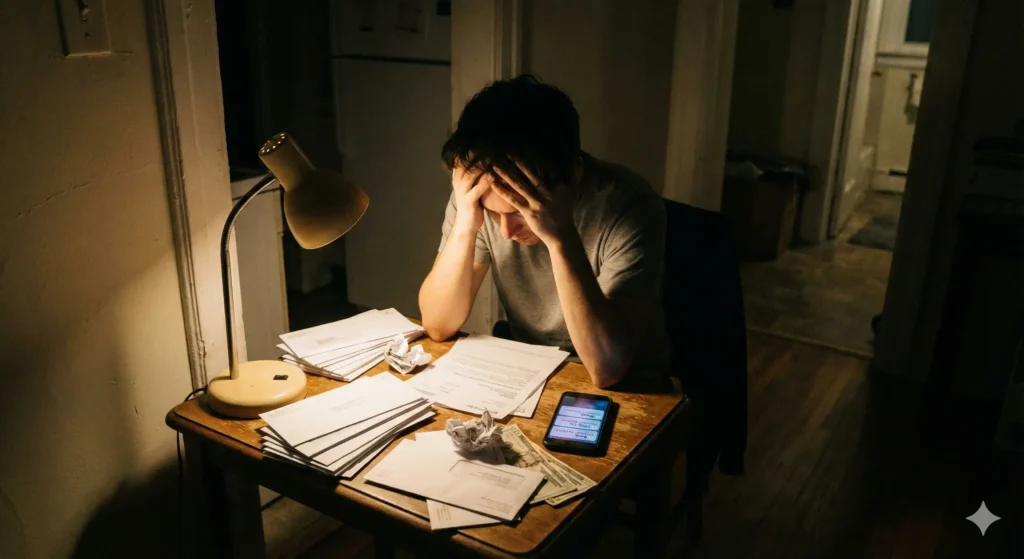

The problem is that debt rarely announces when it stops being helpful. By the time it becomes overwhelming, you’re already inside what many people experience as a debt trap.

This article is written for people who feel stuck, confused, or quietly ashamed about money — even though they’ve been trying their best.

We’ll talk about:

What a debt trap really means in real life

How people fall into it without noticing

Why debt often grows even when payments are made

And what actually helps when you want to get out — step by step

No shortcuts. No motivation speeches. Just clarity.

It’s about how debt starts controlling your choices.

You’re in a debt trap when borrowing is no longer helping you move forward — it’s only helping you survive the present moment. Payments are made, but the total doesn’t seem to come down in any meaningful way.

Over time, something shifts:

You plan life around due dates

New expenses cause panic

Future goals feel unrealistic

At that point, money stops being a tool and starts becoming a source of constant pressure.

Credit cards, personal loans, and buy-now-pay-later options are designed to feel easy at the beginning. They offer quick relief when stress is high — and when stress is high, long-term thinking becomes difficult.

That doesn’t make you careless. It makes you human.

The danger isn’t the first loan. It’s what quietly follows after.

The Cycle That Keeps People Stuck

Debt traps don’t happen overnight. They form through a pattern that slowly tightens.

It often looks like this:

A loan or credit card solves an immediate problem

Monthly payments reduce what’s left for daily life

Small gaps appear in the budget

Credit is used again to fill those gaps

Interest keeps accumulating in the background

Stress increases, clarity decreases

Eventually, financial decisions stop being strategic. They become reactive.

At that point, people aren’t borrowing to improve their lives — they’re borrowing to keep things from falling apart.

That’s the trap.

Why Debt Doesn’t Reduce Even When You’re Paying

This is one of the most frustrating and emotionally draining parts.

Many people ask: “Why am I paying every month, yet nothing seems to change?”

There are a few reasons this happens.

Interest Works Quietly

In many loans and credit cards, interest takes priority. Especially early on, a large part of your payment doesn’t reduce the actual balance by much.

Minimum Payments Create an Illusion

Minimum payments are designed to feel manageable. But they stretch repayment over years, keeping interest active for as long as possible.

Multiple Debts Drain Mental Energy

When several payments are due each month, tracking progress becomes exhausting. People stop looking closely — not because they don’t care, but because it feels overwhelming.

One New Loan Can Undo Months of Effort

Even a small new debt can erase progress, making it feel like nothing you do is working.

Over time, this creates a sense of helplessness — even when effort is being made.

Signs You Might Be in a Debt Trap

You don’t need a spreadsheet to recognize it.

You might be stuck in a debt trap if:

Credit is used for basic needs

One loan is taken to manage another

You avoid checking total balances

Due dates cause anxiety or fear

Income improves, but savings never appear

Money feels emotionally heavy all the time

If you recognize yourself here, pause.

This is not a personal failure. It’s a system working exactly as designed.

The Emotional Side of Debt (Often Ignored)

Debt doesn’t only affect finances.

It affects how people:

Sleep

Communicate with family

Make decisions

See themselves

Many people carry quiet guilt, believing they “should have known better.” But stress, urgency, and lack of guidance change how the brain works. Clear thinking is harder when survival feels uncertain.

Debt grows faster in silence. Understanding weakens its grip.

What Actually Helps When You Want to Get Out

There is no single trick that fixes debt. But there is a process that works more reliably than panic or pressure.

1. Stop Adding New Debt (If Possible)

This alone creates breathing room. Even small new borrowing slows recovery more than most people realize.

2. Get the Full Picture — Gently

Write down every debt: balance, interest rate, and minimum payment. Not to judge yourself — but to remove uncertainty.

Fear often comes from not knowing.

3. Stabilize Before Aggressive Repayment

If essentials aren’t secure, debt tends to return. Even a small emergency buffer reduces the need for future borrowing.

4. Choose a Simple Repayment Method

Complex strategies aren’t required. What matters most is consistency and sustainability.

5. Reduce Emotional Dependence on Credit

This takes time. But real freedom begins when credit stops being the first solution to stress.

What Progress Really Feels Like

Getting out of a debt trap doesn’t feel dramatic.

It feels quiet.

Less panic around money

Slightly better sleep

Decisions made with more calm

A sense that the future isn’t closed anymore

Progress is often slow — but it’s real.

One Final Thing You Should Know

Being in debt does not mean you are irresponsible. It does not mean you lack discipline. It does not mean you’ve failed.

It means you’re navigating a complex financial world without enough support or clarity.

Debt is a chapter — not the whole story.

With patience, understanding, and structure, it can be reduced. And life after it can feel lighter than you expect.

Where to Go From Here

If this article resonated with you, the next helpful steps are:

Understanding how credit cards really keep balances alive

Learning why “easy” payment options often cost more later

Building stability before chasing financial growth

You don’t need extreme solutions. You need clear, honest information.