Table of Contents

- What Is Personal Finance?

- Why Personal Finance Matters More in India

- The 5 Pillars of Personal Finance (Deep Breakdown)

- Personal Finance Lifecycle (Advanced Model)

- Case Study: Middle-Class Indian (Real Scenario)

- Debt Management Strategy

- Personal Finance Rules (Advanced Level)

- Power of Compounding (Critical Concept)

- Personal Finance for Different Income Levels

- Tools to Manage Personal Finance (Monetization Hub)

- Saving vs Investing (Clarity Section)

- Common Mistakes Every Indian Make

- FAQs

- Final Thoughts

Introduction

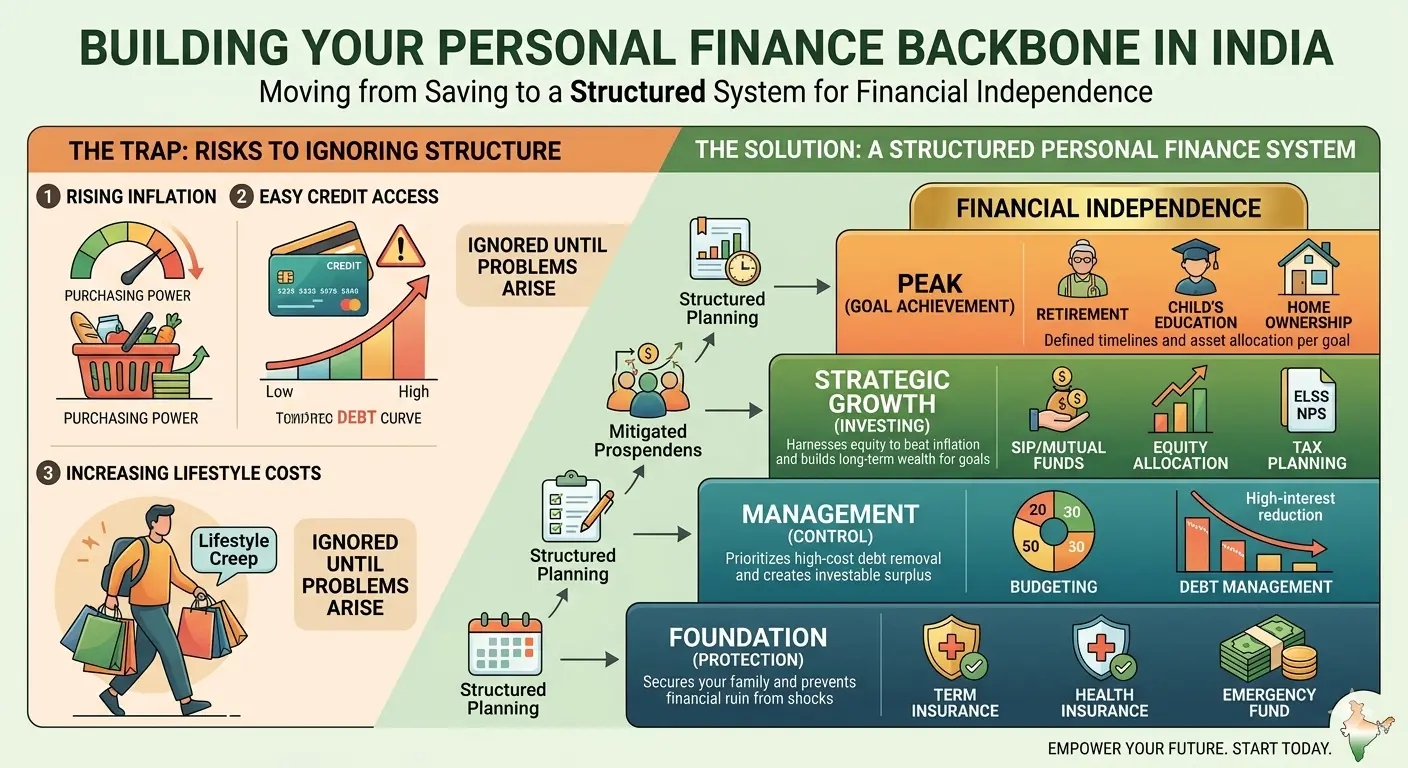

Personal finance is the backbone of financial independence—but in India, it is often misunderstood or ignored until problems arise.

From rising inflation and easy credit access to increasing lifestyle costs, managing money today requires more than just saving—it requires a structured system.

Whether you’re a salaried employee, freelancer, or business owner, mastering personal finance is the only way to:

- Avoid debt traps

- Build long-term wealth

- Achieve financial freedom

This guide goes beyond basics and gives you a practical, India-specific roadmap.

What Is Personal Finance?

Personal finance refers to the systematic management of your money, including:

- Income generation

- Expense tracking

- Saving

- Investing

- Risk protection

In professional terms:

Personal finance is the optimization of financial resources to maximize long-term wealth and minimize risk.

Why Personal Finance Matters More in India

India has unique financial realities:

1. High Inflation Impact

India’s inflation averages 5–7% annually, which silently reduces your money’s value.

₹1 lakh today ≠ ₹1 lakh in 10 years

2. Cultural Spending Pressure

- Weddings

- Festivals

- Family obligations

These can disrupt financial planning if unmanaged.

3. Limited Social Security

Unlike Western countries, India does not provide strong pension systems.

You are responsible for your own retirement.

4. Easy Credit Access

- Credit cards

- Buy Now Pay Later (BNPL)

- Personal loans

These create debt traps if misused.

The 5 Pillars of Personal Finance (Deep Breakdown)

1. Income Optimization (Wealth Starts Here)

Income is not just about earning—it’s about scaling earning capacity.

Types of income:

- Active (salary, business)

- Passive (investments, rent)

- Semi-passive (freelancing)

Case Study (India):

A ₹30,000/month salaried employee vs ₹30,000 salary + ₹10,000 freelancing:

Over 10 years, the second person builds 2–3x wealth faster

2. Budgeting (Cash Flow Engineering)

Budgeting is not restriction—it’s control.

Advanced Budgeting Rule:

- 50% Needs

- 20% Investments

- 20% Savings

- 10% Lifestyle

Example (Indian Salary ₹50,000/month):

- Needs: ₹25,000

- Investments: ₹10,000

- Savings: ₹10,000

- Lifestyle: ₹5,000

Recommended Tool :

To automate this, you can use apps like ET Money to track expenses and categorize spending efficiently.

3. Saving (Capital Preservation Layer)

Savings act as your financial shock absorber.

Emergency Fund Rule:

- Minimum: 3 months expenses

- Ideal: 6 months

- Advanced: 12 months (for freelancers)

Example:

Monthly expense = ₹30,000

Emergency fund = ₹1.8 lakh (6 months)

4. Investing (Wealth Multiplication Engine)

This is where real wealth is created.

Popular Investment Options in India:

| Asset | Returns | Risk |

| Fixed Deposit | 5–7% | Low |

| Mutual Funds | 10–14% | Medium |

| Stocks | 12–20%+ | High |

| Real Estate | Variable | Medium |

| Gold | 6–8% | Low |

To start investing, open a demat account with beginner-friendly platforms like Zerodha, Groww, or Upstox.

These platforms allow:

- Direct stock investing

- SIP in mutual funds

- Portfolio tracking

5. Protection (Risk Shield)

Ignoring this is the biggest mistake Indians make.

Must-have protections:

- Health Insurance (₹5–10 lakh cover minimum)

- Term Life Insurance (10–15x annual income)

Compare and buy affordable insurance plans using platforms like Policybazaar to find the best coverage.

Personal Finance Lifecycle (Advanced Model)

- Earn income

- Optimize income

- Control expenses

- Build emergency fund

- Invest aggressively

- Protect assets

- Plan retirement

Case Study: Middle-Class Indian (Real Scenario)

Profile:

- Salary: ₹40,000/month

- No savings

- Credit card debt: ₹80,000

Transformation Plan:

Month 1–3:

- Budget creation

- Expense tracking

- Debt repayment focus

Month 4–8:

- Build ₹1 lakh emergency fund

Month 9–24:

- Start ₹5,000 SIP monthly

Result After 3 Years:

- Debt-free

- ₹2–3 lakh savings

- Investment portfolio growing

Debt Management Strategy

Types of Debt:

| Good Debt | Bad Debt |

| Home loan | Credit card debt |

| Education loan | Personal loan |

| Business loan | BNPL |

Debt Elimination Strategy:

- Pay high-interest debt first

- Avoid minimum payments

- Consolidate loans if needed

Personal Finance Rules (Advanced Level)

Rule 1: 24-Hour Spending Rule

Avoid impulsive purchases.

Rule 2: 30% EMI Rule

EMIs should not exceed 30% of income.

Rule 3: 10x Insurance Rule

Life cover = 10x annual income.

Rule 4: 15% Investment Rule

Invest at least 15% of income consistently.

Power of Compounding (Critical Concept)

If you invest:

- ₹5,000/month

- At 12% return

After 20 years:

You get ₹50+ lakhs

Time in the market beats timing the market.

Personal Finance for Different Income Levels

Low Income (<₹25K/month)

- Focus: survival + saving

- Priority: emergency fund

- Avoid: loans

Middle Income (₹25K–₹1L/month)

- Focus: budgeting + investing

- Start SIPs

- Get insurance

High Income (>₹1L/month)

- Focus: wealth creation

- Diversify investments

- Tax optimization

Tools to Manage Personal Finance (Monetization Hub)

Here’s your optimized stack:

Budgeting Tools

- Walnut

- ET Money

Investment Platforms

- Zerodha

- Groww

- Upstox

Insurance Platforms

- Policybazaar

These tools simplify execution and improve consistency.

Saving vs Investing (Clarity Section)

| Factor | Saving | Investing |

| Risk | Low | Medium/High |

| Return | Low | High |

| Purpose | Safety | Growth |

Common Mistakes Every Indian Make

- Saving but not investing

- Buying insurance as investment

- Overusing credit cards

- Ignoring inflation

FAQs

How much should I invest monthly?

At least 15–20% of your income.

Is ₹1,000 enough to start investing?

Yes, Start small, scale later.

Should I buy insurance early?

Yes, premiums are cheaper when younger.

Final Thoughts

Personal finance is not about complexity—it’s about consistency.

If you:

- Spend wisely

- Save regularly

- Invest early

- Avoid unnecessary debt

You will achieve financial independence.