A realistic debt payoff plan India is a structured approach where you repay debt consistently without extreme lifestyle cuts. It includes a fixed monthly repayment, a small “fun” budget (₹2,000–₹3,000), and an emergency fund (₹20,000–₹50,000) to prevent new debt. The focus is on sustainability over speed.

KEY TAKEAWAYS (12 min read)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

You can realistically clear ₹8–15 lakh debt in 3–6 years without cutting every expense.

Keeping a ₹2,000–₹3,000/month “fun budget” actually prevents burnout and binge spending.

Debt Snowball builds motivation, while Debt Avalanche saves more interest — choose based on your personality.

Building a ₹20,000–₹50,000 emergency fund alongside debt prevents setbacks from unexpected expenses.

Following a structured plan today can help you avoid long-term interest traps from credit cards and personal loans in India.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Realistic Debt Payoff Plan India (That You’ll Actually Stick To)

You’ve seen those stories.

“Paid off ₹10 lakh in 12 months. No eating out. No fun. No life.”

Sounds impressive. Also sounds… exhausting.

Here’s the problem — most people don’t fail at paying off debt because they’re lazy. They fail because the plan they’re following isn’t built for real life.

If you’re sitting on ₹8–15 lakh of debt — maybe a mix of credit cards, personal loans, or a bike EMI — this guide will show you how to pay it off without turning your life into punishment. And more importantly, how to stick with it long enough to actually finish.

Because honestly? Consistency beats intensity. Every single time.

What a Realistic Debt Payoff Plan India Actually Looks Like

Let me be direct with you.

Extreme plans look good on YouTube. They don’t survive real life in Hyderabad, Pune, or Bengaluru.

Rent goes up.

A wedding pops up.

Your bike needs repairs.

And suddenly — your “perfect plan” collapses.

Here’s where it gets interesting.

When your plan leaves zero room for being human, one bad month turns into quitting entirely.

A real example

Rohit, 32, works in Bengaluru earning ₹65,000/month.

He tried the “cut everything” method:

- No eating out

- No subscriptions

- No travel

It worked… for 2 months.

Then a ₹18,000 medical expense hit.

He used his credit card again.

Back to square one.

The lesson?

A plan that breaks under pressure isn’t a plan. It’s a trap.

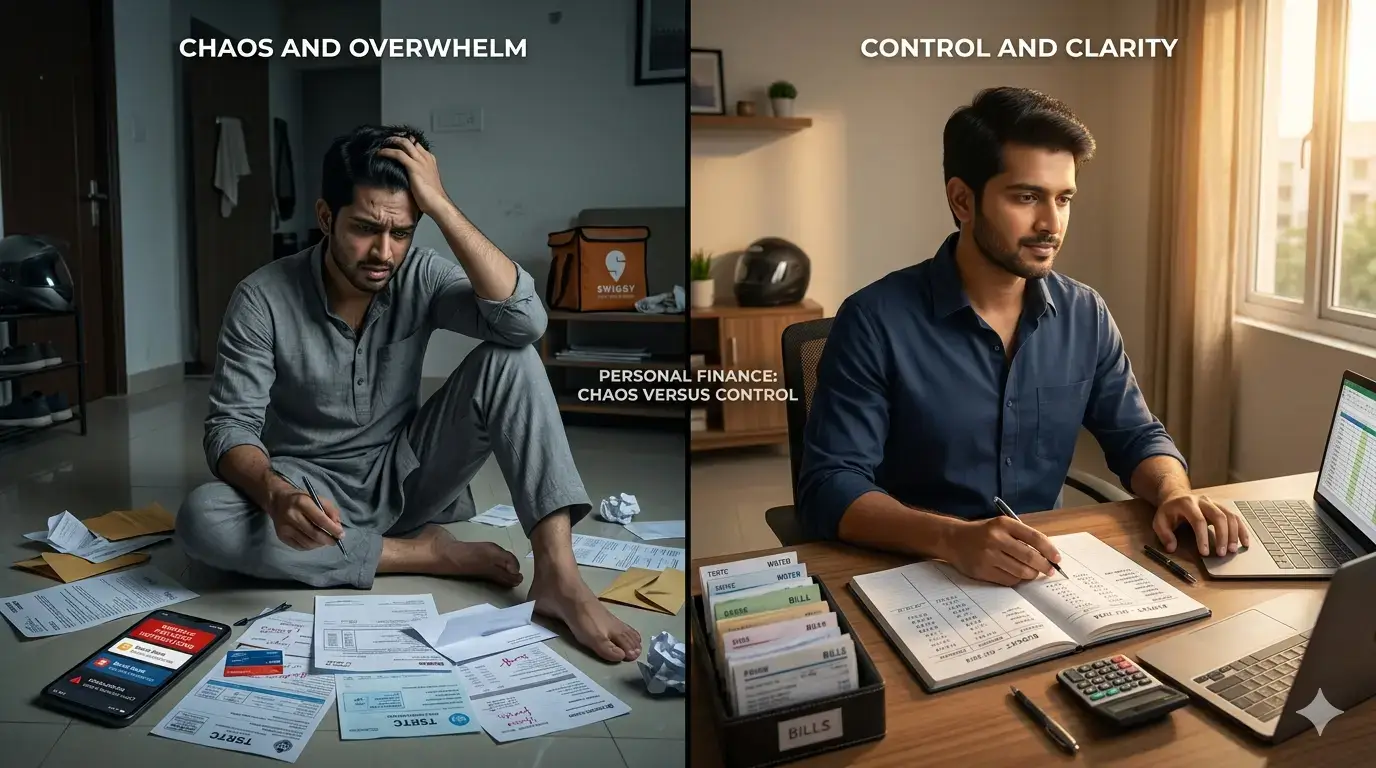

The Real-Life Budget That Actually Works

Now here’s the part most articles skip.

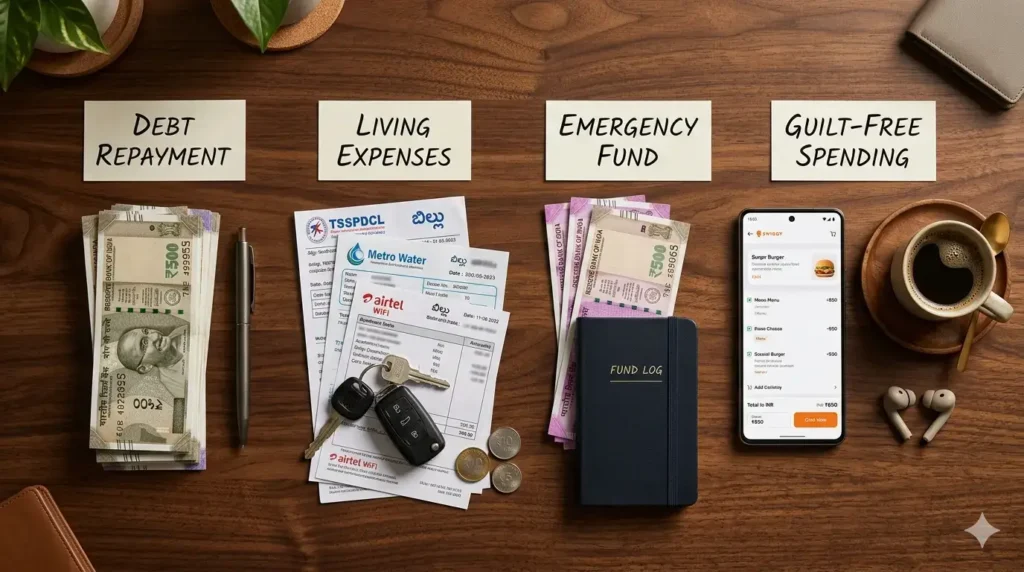

A realistic debt payoff plan isn’t about cutting everything. It’s about allocating money intentionally.

The “Guilt-Free” Spending Bucket

Yes — you need this.

Set aside:

₹2,000–₹3,000/month

For:

- Swiggy/Zomato

- Coffee outings

- Movies

Sounds counterintuitive?

It’s not.

Without this, you’ll eventually snap and spend ₹10,000 in one weekend out of frustration.

Small freedom prevents big mistakes.

The “Life Happens” Fund (Non-Negotiable)

Before aggressively paying debt, build:

₹20,000–₹50,000 buffer

Why?

Because life doesn’t wait for your EMI schedule.

Example:

- Bike repair: ₹8,000

- Medical expense: ₹12,000

Without a buffer → credit card

With buffer → no new debt

That’s the difference between progress and relapse.

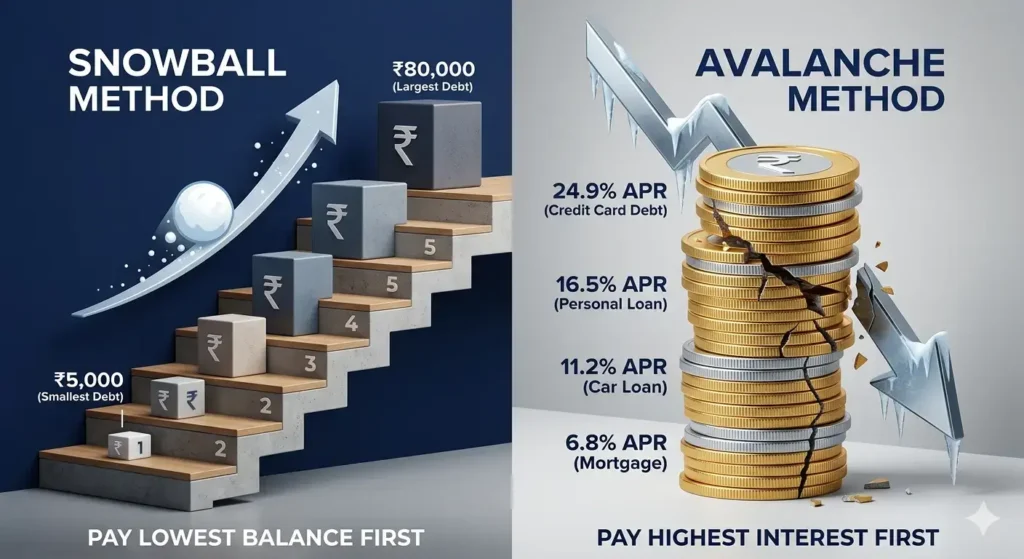

Debt Snowball vs Avalanche — Which One Should YOU Choose?

This is where most people overthink.

Let’s simplify.

Option 1: Debt Snowball (Motivation First)

You pay off the smallest loan first.

Example:

- Credit Card A: ₹40,000

- Personal Loan: ₹3 lakh

- Credit Card B: ₹1.2 lakh

You clear ₹40,000 first → quick win → motivation boost.

Option 2: Debt Avalanche (Math First)

You attack the highest interest loan first.

Typically:

- Credit cards (30–42% interest)

- Then personal loans

- Then lower-interest EMIs

This saves more money over time.

The truth is, a realistic debt payoff plan India isn’t about choosing the mathematically perfect method — it’s about choosing the one you’ll follow for the next 36–48 months.

So which one is better?

Honestly?

The one you won’t quit.

My take (and this matters)

If you’re feeling overwhelmed → start with Snowball

If you’re disciplined already → go Avalanche

Because saving interest doesn’t matter if you give up halfway.

Month 4–6 — The “Lull” That Nobody Warns You About

This is where most realistic debt payoff plan India journeys fail — not because of money, but because of lost momentum.

Month 1–2: Excitement

Month 3: Progress visible

Month 4–6: Motivation drops

Your debt is still big.

Your effort feels invisible.

And you start thinking:

“Is this even working?”

Stay with me — this next part matters most.

How to survive this phase:

- Track your progress weekly (not monthly)

- Celebrate small wins (₹10k paid = win)

- Don’t increase lifestyle just because income increased

Real story

Anita, 29, from Pune, had ₹9 lakh in combined debt.

Month 5 — she could only pay minimum due to a family emergency.

She felt like she failed.

But she didn’t quit.

That one decision?

That’s why she cleared her debt in 4 years.

Progress isn’t linear. And that’s okay.

The “Trade-Off” System That Makes This Sustainable

Here’s a simple shift that changes everything.

Instead of cutting — swap.

Examples:

| Expensive Habit | Smarter Alternative | Monthly Savings |

|---|---|---|

| ₹3,000 weekend dining | ₹1,200 home outings | ₹1,800 |

| ₹1,500 subscriptions | ₹500 shared plans | ₹1,000 |

| Daily ₹200 coffee | ₹50 homemade | ₹4,500 |

That’s ₹7,000+/month saved.

Without feeling miserable.

This is the part that changes everything.

You’re not restricting your life.

You’re redesigning it.

What a ₹10 Lakh Debt Payoff Actually Looks Like

Let’s make this real.

Assume:

- Debt: ₹10 lakh

- Interest: ~14% blended

- Monthly payment: ₹25,000

Timeline:

- Year 1: ₹3 lakh paid

- Year 2: ₹3 lakh paid

- Year 3: ₹4 lakh + interest cleared

Total: ~3–4 years

Now compare that to doing nothing.

You’ll still be paying EMIs… 5 years from now.

Maybe more.

The difference isn’t speed. It’s direction.

By now, you can see that a realistic debt payoff plan India is less about sacrifice and more about sustainability.

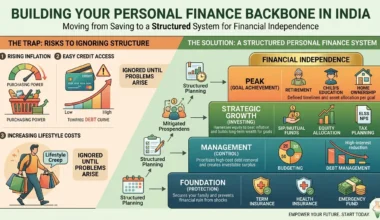

Explore Personal Finance Fundamentals in India (Ultimate 2026 Guide for Beginners) to give the next practical step.

Your Next Step (Do This Within 24 Hours)

Don’t overcomplicate this.

Here’s what to do today:

- List all your debts (amount + interest rate)

- Choose Snowball or Avalanche

- Set your “fun budget” (₹2–3k)

- Start a ₹20k emergency buffer

That’s it.

Not perfect. But real.

And here’s my question for you:

What’s the one expense you know you can reduce without feeling miserable?

Start your realistic debt payoff plan India today — not perfectly, but consistently. Because that’s what actually works.

Frequently Asked Questions

Can I pay off ₹10 lakh debt on a ₹60,000 salary?

Yes, but it requires structure. If you allocate ₹20,000–₹25,000 monthly toward debt and control lifestyle inflation, you can clear it in 3–5 years. The key is consistency, not extreme cuts.

Should I stop all spending while paying debt?

No. Completely cutting spending often leads to burnout and binge spending later. A small ₹2,000–₹3,000 monthly allowance keeps your plan sustainable and realistic.

Is Debt Snowball better than Avalanche in India?

Financially, Avalanche saves more interest. But Snowball works better psychologically for many Indians dealing with multiple loans. Choose based on your ability to stay consistent.

Should I invest while paying off debt?

If your debt interest is above 10–12% (like credit cards or personal loans), focus on clearing it first. You can start investing after reducing high-interest debt.

What if I miss a payment one month?

Missing a planned extra payment isn’t failure. Just resume the plan next month. The biggest mistake is quitting entirely after one setback.

About the Author

I’m Mahesh Reddy, the voice behind InvestingLens—a platform built from real financial mistakes, hard lessons, and the journey of getting back control. I’m still on this journey—not pretending to be perfect.

⚠️ Disclaimer: This article is for educational purposes only and does not constitute financial advice. Please consult a SEBI-registered financial advisor before making any investment decisions. Markets carry risk — past returns do not guarantee future performance.

External Links :

RBI financial literacy (https://www.rbi.org.in)

SEBI guidelines (https://www.sebi.gov.in)