If you’re stuck choosing between debt settlement vs debt consolidation, here’s the blunt truth:

Debt consolidation helps you repay smarter. Debt settlement helps you escape when you can’t repay at all..

Explore What Is Debt Consolidation? Stop Paying 36% Interest on Credit Cards in India to give readers the next practical step.

Both can reduce stress. But they come with very different long-term consequences — especially for your CIBIL score and financial future.

Understanding debt settlement vs debt consolidation can save you lakhs in the long run.

Ravi from Hyderabad thought he was doing everything right. A decent Rs. 60,000 salary. Two credit cards. One personal loan. Then one missed payment turned into three. And suddenly, he was staring at Rs. 3.2 lakh in debt, with no clear way out.

This guide breaks it down in simple terms, with real Indian examples, so you can decide what actually works for your situation — not just what sounds easy.

Key Takeaways

Banks trust consolidation. They flag settlement as a risk

Debt consolidation = combining loans into one EMI (less interest, better control)

Debt settlement = negotiating to pay less than total dues (hurts CIBIL badly)

Settlement is usually a last resort, not a strategy

Consolidation works best if your income is still stable

Table of Contents

What is Debt Consolidation?

Debt consolidation is simple:

You take one new loan to pay off multiple debts.

Instead of juggling 5 EMIs…

You now handle just one EMI.

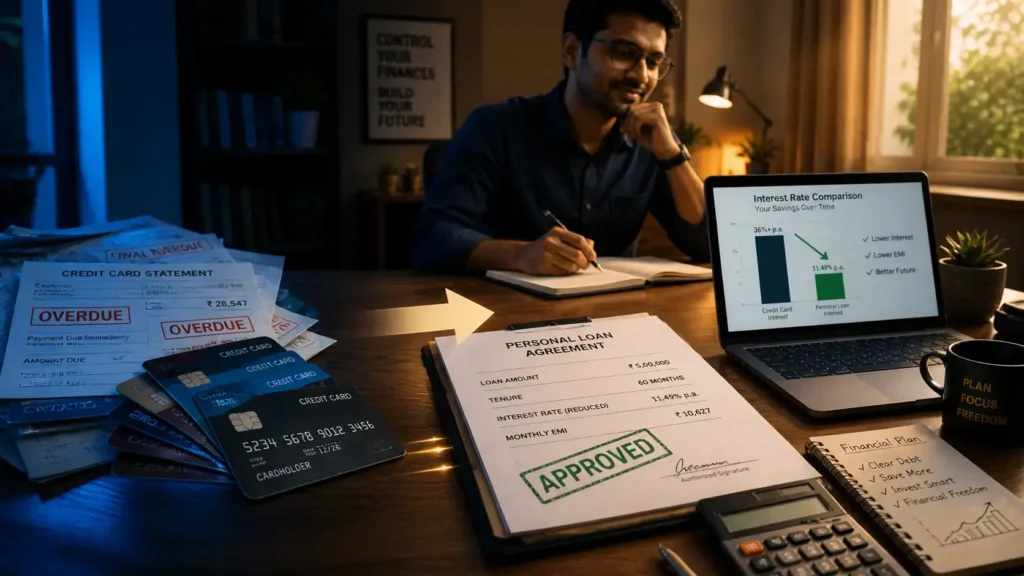

Example: Ravi’s Situation

Ravi, a 32-year-old IT employee in Hyderabad:

- Credit Card 1: Rs. 80,000 @ 36% interest

- Credit Card 2: Rs. 60,000 @ 42% interest

- Personal Loan: Rs. 1,50,000 @ 16% interest

Total debt: Rs. 2,90,000

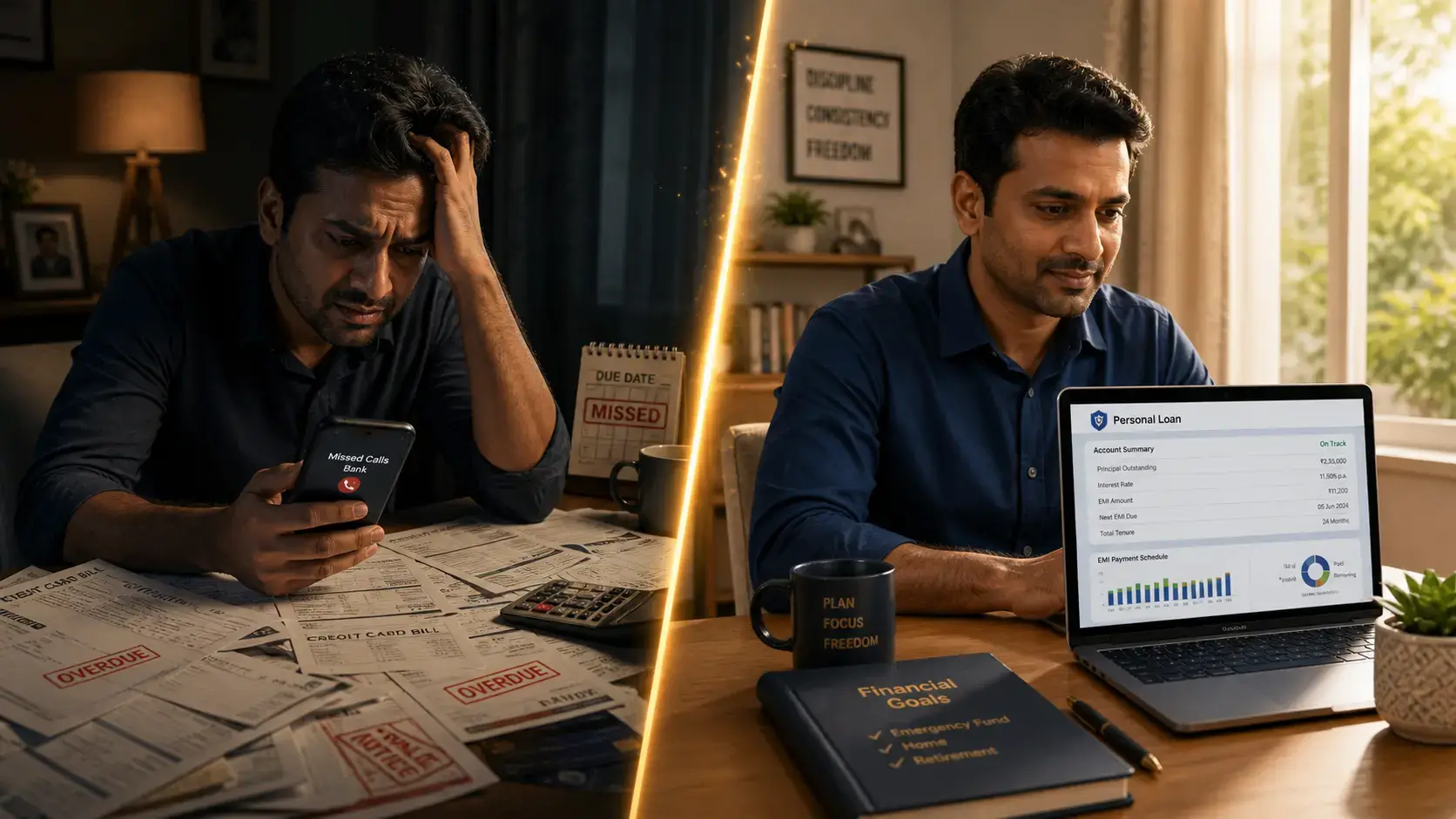

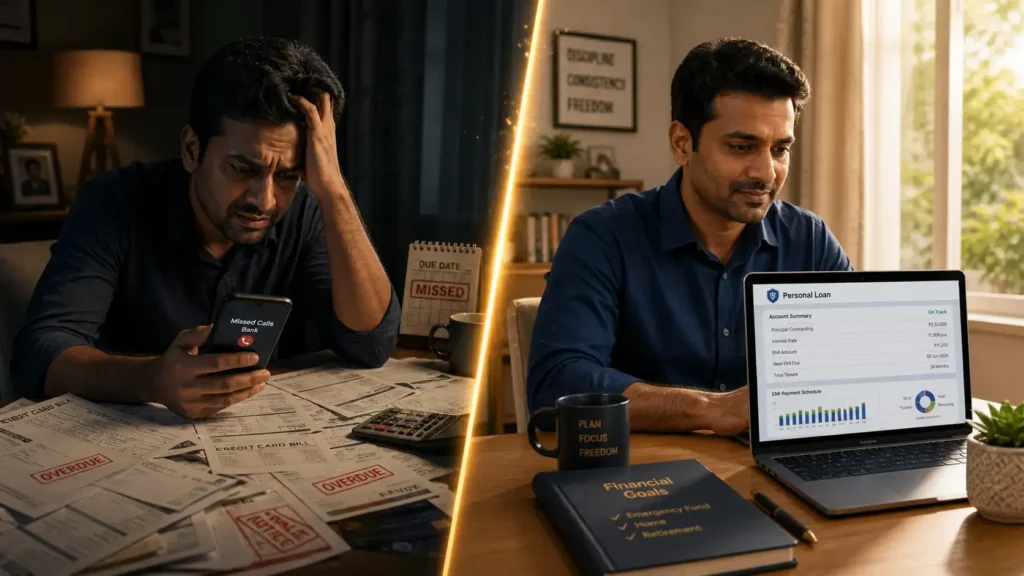

Monthly EMIs? Messy. Stressful. Expensive.

What Ravi Does

He takes a debt consolidation personal loan:

- Loan Amount: Rs. 3,00,000

- Interest: 14%

- Tenure: 3 years

Now:

- One EMI

- Lower interest

- Clear timeline

Why This Works

- Credit cards charge insane interest (30–45%)

- Consolidation reduces that burden

- You stay financially responsible in the system

Banks like this behaviour.

What is Debt Settlement?

Debt settlement is a completely different game.

You tell the bank:

“I cannot repay the full amount. Let’s settle.”

Bank agrees to take less than what you owe.

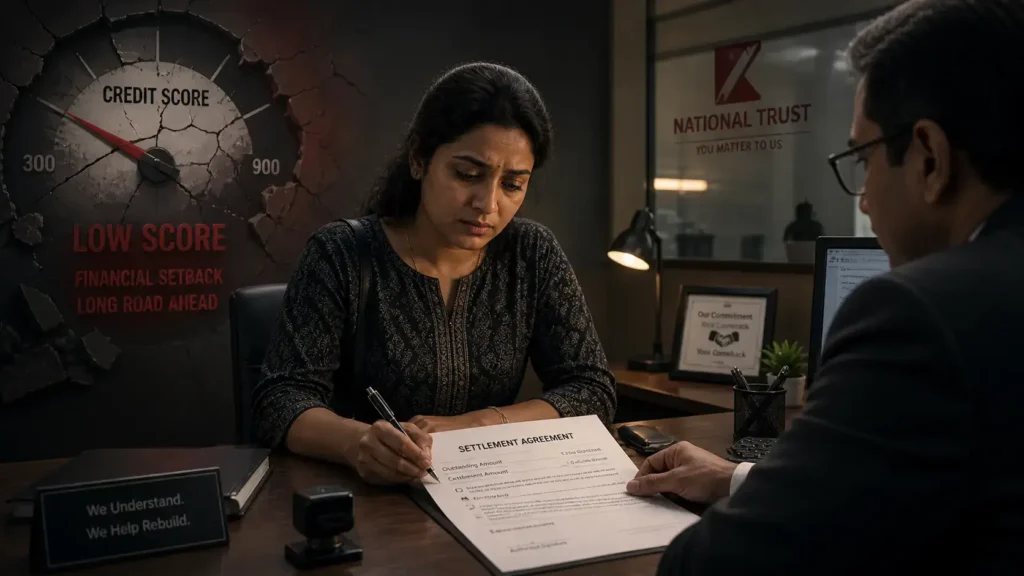

Example: Priya’s Situation

Priya, working in retail:

- Credit Card Debt: Rs. 2,00,000

- Lost job, unable to pay

After months of default:

Bank offers settlement:

Pay Rs. 1,20,000 → account closed

Sounds like a win?

Not really.

The Hidden Cost

Her credit report with CIBIL now shows:

“Settled” instead of “Closed”

This is a red flag.

Debt Settlement vs Debt Consolidation (Core Differences)

| Factor | Debt Consolidation | Debt Settlement |

|---|---|---|

| Purpose | Manage debt | Escape debt |

| Credit Score | Improves over time | Drops sharply |

| Bank View | Responsible | Risky borrower |

| Loan Eligibility | Easier later | Difficult |

| Interest | Reduced | Not applicable |

| Impact Duration | Short-term | Long-term damage |

True Indian Scenarios

1. Mahesh – The EMI Juggler

Salary: Rs. 75,000

EMIs: Rs. 38,000

He chose consolidation.

Outcome after 2 years:

- Stable finances

- CIBIL improved from 690 → 760

- Eligible for home loan

2. Suresh – The Shortcut Taker

Salary: Rs. 50,000

Debt: Rs. 3 lakh

He went for settlement.

5 years later:

- Loan rejected twice

- Car loan interest higher

- CIBIL stuck at 620

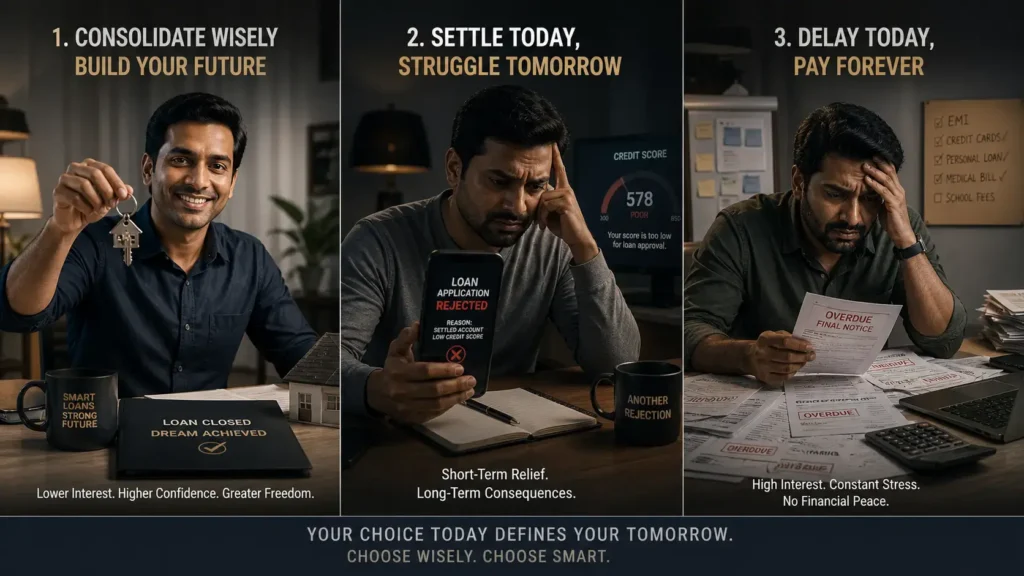

3. Neha – The Confused Middle

She delayed decision.

Result?

- Late fees piled up

- Harassment calls

- Eventually forced into settlement

Here’s the uncomfortable truth:

Indecision is costlier than wrong decisions.

Detailed Rs. Calculation (This Will Open Your Eyes)

Let’s compare both options:

Scenario: Rs. 3,00,000 Debt

Option 1: Debt Consolidation

- Interest: 14%

- Tenure: 3 years

EMI ≈ Rs. 10,260

Total Paid ≈ Rs. 3,69,360

Option 2: Debt Settlement

- Settlement Amount: Rs. 2,00,000

You save Rs. 1,00,000.

Sounds great? Wait.

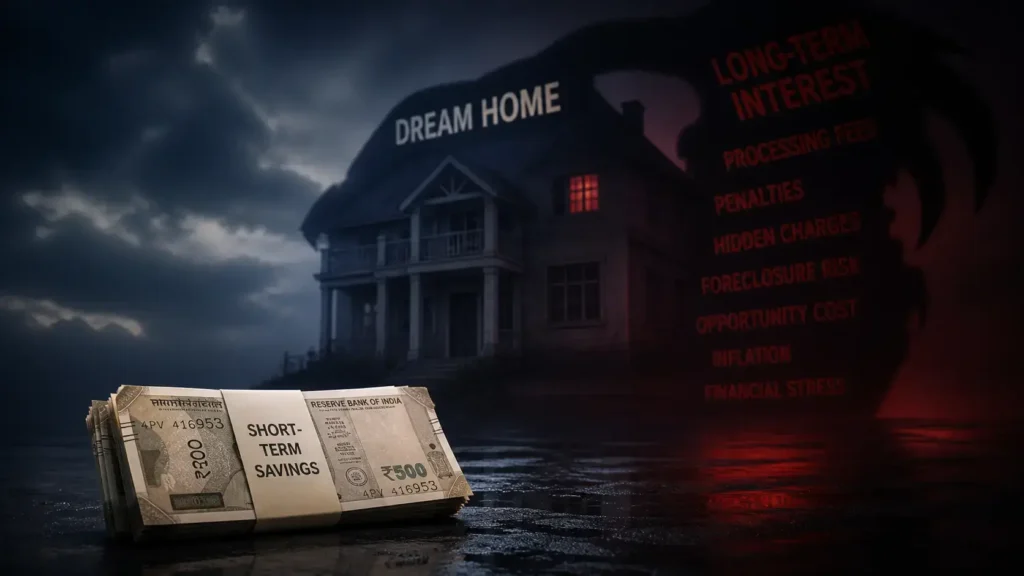

Hidden Financial Loss

Because of low CIBIL:

Future loan interest increases by even 3%

On a home loan of Rs. 40 lakh:

Extra interest paid = Rs. 8–10 lakh

You saved Rs. 1 lakh today…

but lost Rs. 10 lakh tomorrow.

That’s how settlement traps you.

CIBIL Score Impact

Your credit report is maintained by CIBIL under RBI-regulated systems like Reserve Bank of India.

Debt Consolidation Impact

- Slight dip initially

- Improves with timely payments

- Seen as positive behavior

Debt Settlement Impact

- Score drops drastically (100–150 points)

- Mark stays for years

- Banks see you as high risk

Let’s be blunt:

Settlement tells lenders — “This person didn’t pay fully.”

That label sticks.

When Should You Choose Debt Consolidation?

Choose this if:

- You still have a stable income

- You can pay EMIs (even if tight)

- You want to protect your credit future

Ideal for:

- Salaried professionals

- Young borrowers

- People planning home loans

When Debt Settlement Makes Sense

Let’s not pretend it’s always bad.

Sometimes, it’s the only option left.

Choose settlement if:

- You lost income completely

- You’re already defaulting

- Recovery agents are involved

- Mental stress is unbearable

But understand:

It’s damage control, not a strategy.

Common Mistakes Indians Make

Mistake 1: Ignoring the Problem

“If I don’t answer calls, it will go away.”

No. It will grow.

Mistake 2: Minimum Payment Trap

Paying Rs. 5,000 on Rs. 2 lakh credit card debt?

You’re feeding interest, not reducing debt.

Mistake 3: Lifestyle Denial

If you earn Rs. 40,000 but spend like Rs. 80,000…

Debt is inevitable.

Hard truth:

Your habits created the debt.

Your discipline will remove it.

FAQ Section

1. Is debt settlement legal in India?

Yes, but regulated indirectly through banks under Reserve Bank of India guidelines.

2. Does debt settlement affect CIBIL?

Yes. It negatively impacts your score and stays for years.

3. Is debt consolidation better than settlement?

In most cases, yes — especially if you can still repay.

4. Can I get a loan after settlement?

Possible, but difficult and expensive.

5. Which is cheaper: settlement or consolidation?

Settlement looks cheaper short-term.

Consolidation is cheaper long-term.

Conclusion

Debt settlement vs debt consolidation is not just a financial choice.

It’s a character signal to lenders.

One says:

“I struggled, but I paid.”

The other says:

“I couldn’t pay fully.”

That difference matters. A lot.

If you’re still earning, still capable…

Choose consolidation. Protect your future.

If you’re already drowning…

Choose settlement — but accept the consequences.

Disclaimer: This content is for educational purposes only. Financial decisions depend on individual circumstances. Consult a certified financial advisor before taking action.

Mahesh Reddy

Founder, InvestingLens.com

Mahesh writes about money the way it actually behaves in Indian households — messy, emotional, and real. His goal is simple: help Indians avoid financial regrets before they happen.