Introduction

For readers searching for this topic, the key point is if you’re stuck choosing between saving an emergency fund vs debt — here’s the truth.:

You should NOT blindly do one first. You need a strategy.

Most Indians get this wrong. They either:

- Save aggressively while drowning in 36% credit card interest

- OR repay loans fully and then panic during emergencies

Both approaches can quietly destroy your finances.

This guide will show you:

- Exactly what to prioritize first (step-by-step)

- How to balance emergency fund vs debt in India

- Real examples with Rs. calculations

- And the mistakes that are costing people lakhs

Let’s get uncomfortable for a minute.

If you’re paying high-interest debt and still ordering Rs. 500 Zomato dinners three times a week — you’re not “managing finances.”

You’re leaking money.

Key Takeaways Box

- You need BOTH emergency fund and debt repayment — but in the right order

- High-interest debt (credit cards, personal loans) must be attacked first

- Minimum emergency fund = 1–2 months expenses initially

- Ideal full emergency fund = 6 months expenses

- Ignoring emergencies leads to more debt traps

- Discipline matters more than income

Table of Contents

Why This Confusion Exists

Most financial advice online is imported from the US.

India is different.

- We have higher personal loan interest rates

- Less social safety net

- Heavy reliance on EMIs

- Cultural pressure to “manage everything”

So when advice says:

“Save 6 months emergency fund first”

It ignores one reality:

Your credit card is charging 30–42% interest.

That’s not a suggestion. That’s a financial fire.

The Real Problem: Cash Flow vs Interest

Here’s the real battle:

- Emergency fund = protection

- Debt repayment = damage control

You need both.

But timing matters.

Step-by-Step Plan (Emergency Fund vs Debt India)

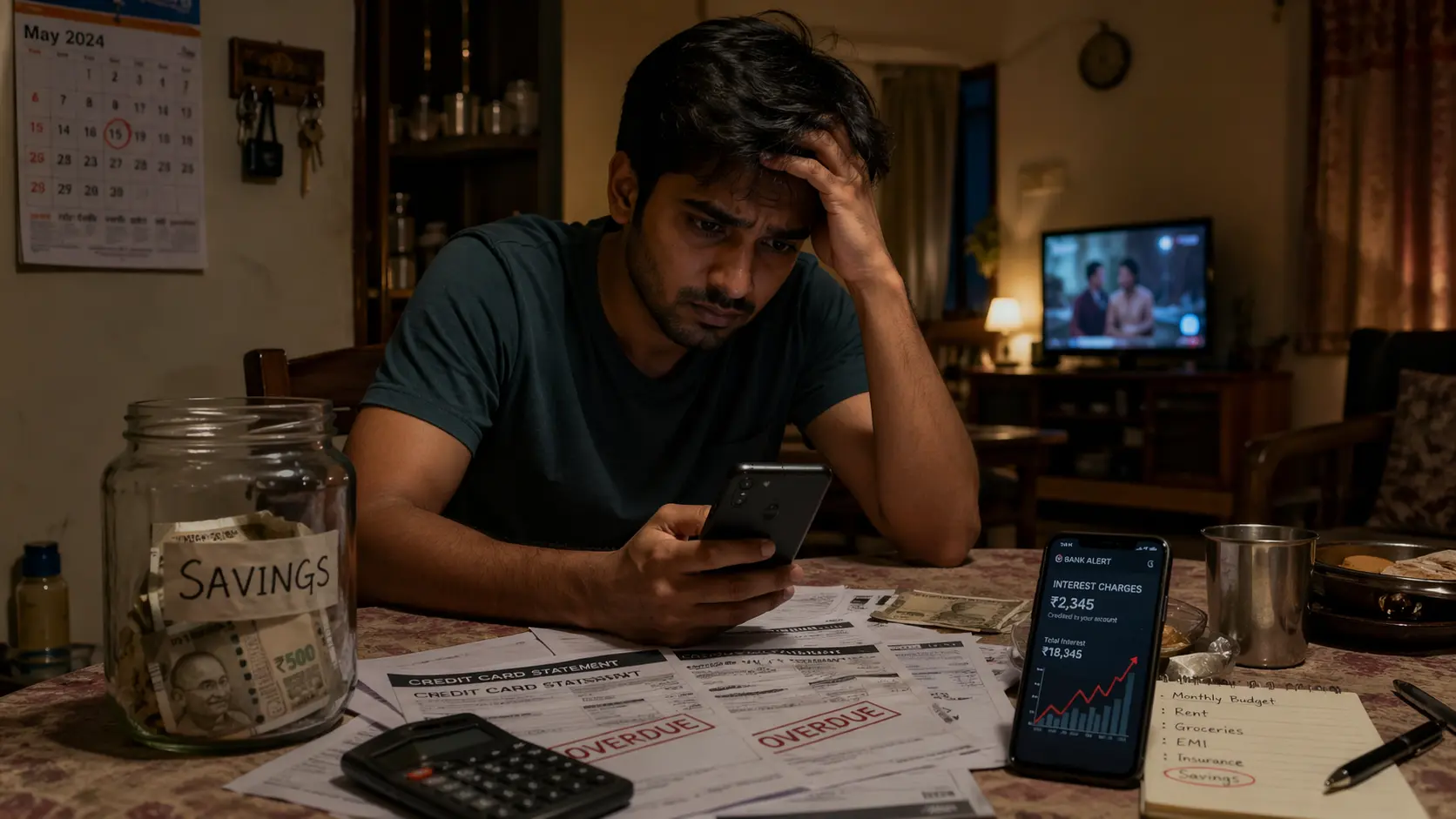

Step 1: Build a Mini Emergency Fund (₹25K–₹1 Lakh)

Before attacking debt fully:

Create a small buffer.

Why?

Because without it:

- One medical bill = new loan

- One job loss = credit card spiral

Example:

Priya (salary: ₹40,000/month)

Monthly expenses: ₹30,000

First goal: ₹60,000 emergency fund (2 months)

Not ₹3 lakh. Not ₹5 lakh.

Start small.

Step 2: Attack High-Interest Debt Aggressively

Now comes the uncomfortable part.

If you have:

- Credit card dues

- Personal loans

These are your enemies.

Let’s be blunt:

If your debt interest > 12%

It’s urgent.

Explore Debt Snowball vs Avalanche — 7 Proven Ways.

Step 3: Pay Minimum on Low-Interest Loans

Home loan? Education loan?

Don’t panic.

Focus energy where it matters.

Real Rs. Calculation (This Will Hit Hard)

Let’s take Ravi.

- Credit card debt: ₹1,00,000

- Interest: 36% annually (~3% monthly)

If Ravi pays only minimum:

After 1 year → ₹1,36,000+

Now imagine:

Instead of clearing debt, he saves ₹10,000/month.

He feels good.

But mathematically?

He’s losing.

Scenario Comparison

| Action | Result After 12 Months |

|---|---|

| Save ₹10K/month | ₹1,20,000 saved |

| Ignore debt | ₹36,000 interest paid |

Net loss: ₹36,000

This is why blind saving is dangerous.

Common Mistakes Indians Make

1. “Saving feels safe, debt feels stressful”

So they ignore debt.

Big mistake.

2. EMI Lifestyle Trap

Mahesh earns ₹70,000/month:

- ₹18K bike EMI

- ₹12K personal loan EMI

- ₹8K credit card minimum

Left with almost nothing.

Still goes on trips.

This is not lifestyle.

This is slow financial collapse.

3. No Emergency Fund at All

Then one hospital bill hits.

Guess what happens?

More loans.

Explore Get Out of Debt Fast India: Step-by-Step Plan 2026.

Before vs After Transformation

Before (Typical Case)

Amit:

- Salary: ₹50,000

- Debt: ₹2 lakh

- Savings: ₹0

Result:

- Stress

- Late payments

- Low CIBIL score

- Constant anxiety

After (Following Plan)

- Built ₹75,000 emergency fund

- Paid off credit cards in 10 months

- Started SIP ₹5,000

Result:

- Stability

- Control

- Confidence

Timeline Strategy (What to Do First)

Month 1–3

- Build mini emergency fund

Month 3–12

- Aggressively clear high-interest debt

Month 12–18

- Expand emergency fund to 6 months

After 18 months

- Start investing seriously

The Hard Truth

If you’re:

- Carrying credit card debt

- Ordering food 10 times a month

- Paying for subscriptions you don’t use

You don’t have a money problem.

You have a discipline problem.

And no financial plan works without fixing that.

Where RBI & System Matter

India’s financial system isn’t forgiving.

- Interest rates regulated by Reserve Bank of India still allow high credit card rates

- Missed payments affect your entire financial future

This isn’t a game.

FAQ Section

1. Emergency Fund vs Debt India – what should I prioritize?

Start with a small emergency fund, then aggressively pay high-interest debt.

2. How much emergency fund is enough in India?

Minimum: 2 months expenses

Ideal: 6 months expenses

3. Should I invest while having debt?

Only if debt interest is low (<10–12%). Otherwise, clear debt first.

4. Is credit card debt really that bad?

Yes. At 30–40% interest, it can double your financial problems quickly.

5. Can I skip emergency fund and focus only on debt?

No. One emergency will push you back into debt again.

Conclusion

Balancing emergency fund vs debt in India isn’t about choosing one.

It’s about sequencing.

- Build a cushion

- Kill toxic debt

- Then grow wealth

Simple.

Not easy.

But doable.

Start today — even if it’s ₹500.

Disclaimer: This content is for educational purposes only and not personalized financial advice. Always consider your individual financial situation before making decisions.

Author Bio

Mahesh Reddy

Founder, InvestingLens.com

Mahesh writes about personal finance the way it actually feels — messy, emotional, and real. His goal is simple: help Indians stop surviving financially and start taking control.