Introduction

What is debt consolidation?

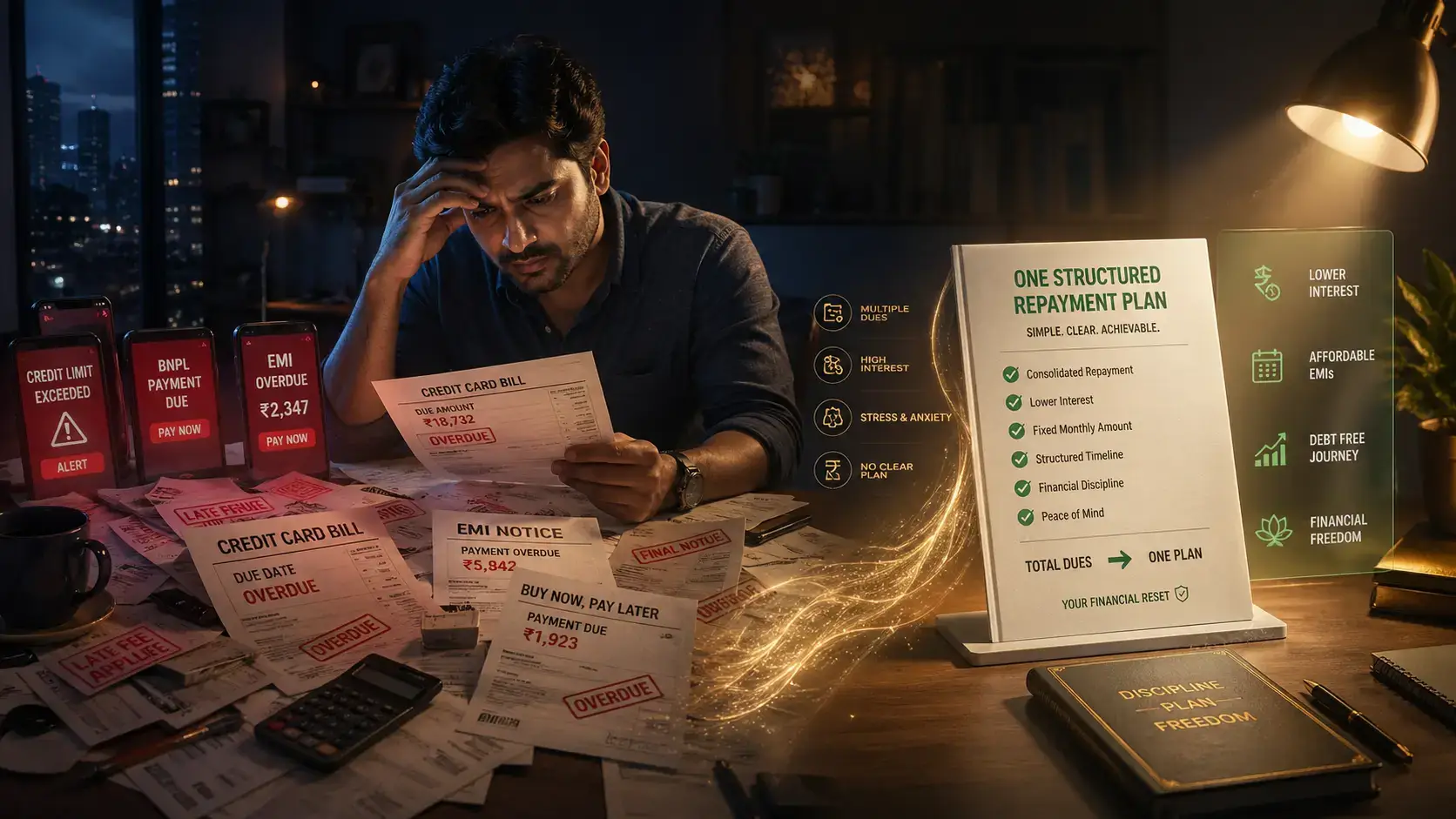

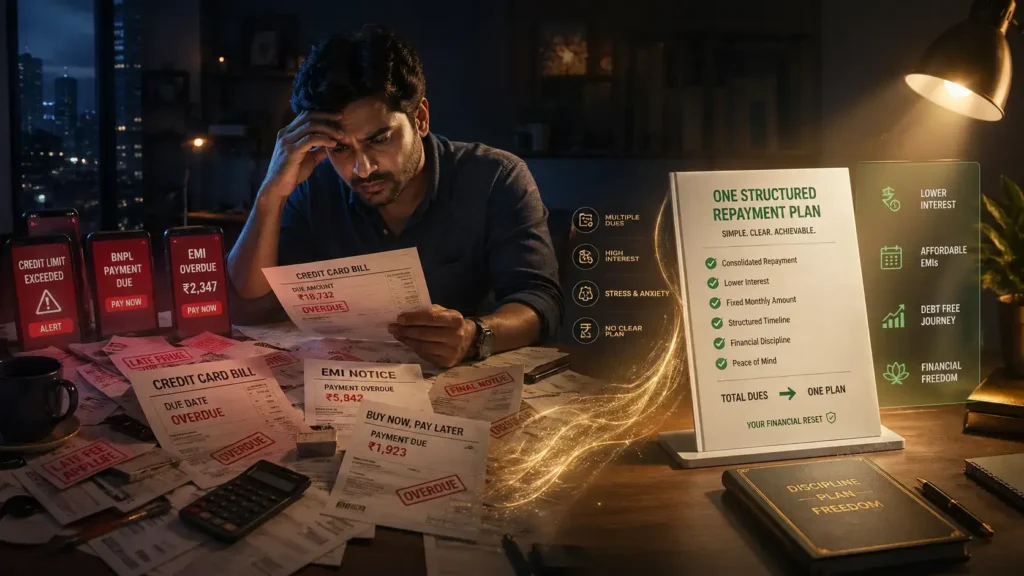

If you’re paying Rs. 12,000–Rs. 25,000 in EMIs every month and still watching your credit card balance barely move…

You’re not just “managing debt.”

You’re stuck in a system designed to keep you there.

Here’s the uncomfortable truth:

If your credit card charges 36–42% interest and you’re only paying minimum dues, you’re not reducing debt—you’re feeding it.

That’s exactly why understanding what is debt consolidation can be a turning point for many Indian salaried professionals.

Done right, it can:

- Reduce your EMI burden

- Cut your interest by lakhs

- Give you breathing space

Done wrong?

You’ll end up with one big loan + fresh debt—a worse situation than before.

Here’s the uncomfortable truth:

Paying minimum dues on a credit card charging 36–42% interest is not repayment. It’s slow financial damage.

And most salaried Indians don’t realise this until:

- Their savings are gone

- Their CIBIL score drops

- Banks start tightening access

That’s where debt consolidation enters the picture.

Done right, it can:

- Cut your interest burden

- Simplify your life into one EMI

- Help you recover control

Done wrong?

You’ll end up with one big loan + fresh credit card debt—a worse mess than before.

Let’s break this down properly. No fluff. Just reality.

Key Takeaways Box

- Debt consolidation = combining multiple debts into one loan

- Works best when replacing high-interest debt (30%+)

- Reduces EMI stress but does not fix bad habits

- Can improve CIBIL score over time

- Dangerous if you continue using credit after consolidation

What Is Debt Consolidation?

Debt consolidation means taking one new loan to pay off multiple existing debts.

Instead of managing:

- 2–3 credit cards

- Personal loans

- BNPL apps

You replace all of it with one single EMI at a lower interest rate.

Simple idea. Powerful impact.

But don’t confuse simplicity with safety.

Why Most Indians Need Debt Consolidation (But Don’t Admit It)

Let’s call it out.

The typical urban salaried setup:

- Swiggy + Amazon = lifestyle inflation

- Credit cards = convenience

- EMIs = “manageable”

Until it isn’t.

Real problem:

- Credit card interest: 36–42%

- Personal loan interest: 18–24%

You’re not borrowing.

You’re bleeding money.

And if you’re only paying minimum dues…

👉 Your debt can take years to clear.

Real Indian Scenarios (This Is Where It Gets Real)

Ravi (Software Engineer, Hyderabad)

- Salary: Rs. 70,000

- Credit Cards: Rs. 2 lakh total @ 38%

- Personal Loan EMI: Rs. 8,500

He was paying ~Rs. 18,000 monthly.

Still, total debt barely reduced.

Action: Took Rs. 2.5 lakh consolidation loan @ 14%

Result:

- EMI dropped to ~Rs. 10,500

- Interest burden reduced massively

- Became debt-free in 3 years

Priya (Marketing Executive, Bangalore)

- Debt: Rs. 1.5 lakh across cards + BNPL

- Took consolidation loan

Sounds smart, right?

Here’s what she did next:

- Continued shopping

- Used credit cards again

Result:

Now she has:

- Consolidation loan

- New credit card debt

👉 This is the trap nobody talks about.

Mahesh (Govt Employee, Vijayawada)

- Used loan against FD @ 8%

- Closed all high-interest debts

Result:

- Lowest cost solution

- No financial stress

Smart doesn’t mean complex.

Smart means disciplined.

Rs. Calculation: Before vs After (This Is Where Money Is Saved)

Let’s break a real scenario.

Before Consolidation

| Debt | Amount | Interest | EMI |

|---|---|---|---|

| Credit Card 1 | Rs. 1,20,000 | 36% | Rs. 6,000 |

| Credit Card 2 | Rs. 80,000 | 40% | Rs. 4,000 |

| Personal Loan | Rs. 1,00,000 | 18% | Rs. 5,500 |

Total EMI: Rs. 15,500

And most of it? Interest.

After Consolidation

- New Loan: Rs. 3,00,000

- Interest: 14%

- Tenure: 3 years

New EMI: ~Rs. 10,300

What Changed?

- Monthly savings: ~Rs. 5,200

- Interest saved: Rs. 60,000–Rs. 80,000 approx

That’s not small.

That’s your emergency fund right there.

Types of Debt Consolidation Options in India

1. Personal Loan

- Fast approval

- Most common option

- Moderate interest

2. Balance Transfer Credit Cards

- Low initial interest

- Dangerous if misused

3. Loan Against Property

- Lower interest

- High risk (you’re pledging your home)

4. Loan Against FD

- Cheapest option (7–9%)

- Best for disciplined people

When Debt Consolidation Works

It works if:

- You stop new borrowing

- You follow a repayment plan

- You control expenses

Simple rules. Hard to follow.

Explore Debt Snowball vs Avalanche — 7 Proven Ways

When It Backfires (Reality Check)

Let’s be brutally honest.

Debt consolidation fails when:

- You treat it like “extra money”

- You keep swiping credit cards

- You don’t track spending

Hard Truth:

If you’re spending Rs. 8,000/month on food delivery while paying 36% interest…

You’re not in a debt problem.

You’re in a behaviour problem.

Impact on CIBIL Score

Your CIBIL score reacts like this:

Short-term:

- Small dip due to new loan

Long-term:

- Improves with consistent EMI payments

Key factor:

Lower credit utilization = higher score

Step-by-Step: How to Consolidate Debt in India

Step 1: List everything

Every loan. Every card. No hiding.

Step 2: Check your credit score

Below 650? Expect higher interest.

Step 3: Compare lenders

Look beyond EMI:

- Processing fees

- Prepayment penalties

Step 4: Close all old debts immediately

No delays. No excuses.

Step 5: Cut access to easy credit

- Reduce limits

- Remove saved cards

- Uninstall shopping apps

Yes, it sounds extreme.

That’s because your situation probably is.

Before vs After Transformation (Mindset Shift)

Before:

- Multiple EMIs

- Constant stress

- No savings

After:

- One EMI

- Clear plan

- Financial breathing room

But only if you stay disciplined.

FAQ Section

1. What is debt consolidation in simple terms?

Debt consolidation means combining multiple debts into one loan with a single EMI and lower interest rate.

2. Is debt consolidation a good idea in India?

Yes, if used to replace high-interest debt and followed with disciplined repayment.

3. Will debt consolidation hurt my CIBIL score?

Short-term dip, but long-term improvement if managed well.

4. Can I consolidate only credit card debt?

Yes, and that’s the most common use case due to high interest rates.

5. Is what is debt consolidation the same as a personal loan?

Loan against FD is cheapest, personal loan is most accessible.

Conclusion

Now that you understand what is debt consolidation.

Your behavior is.

This is just a tool.

Used right → it can save you lakhs

Used wrong → it will bury you deeper

So don’t just ask:

“What is debt consolidation?”

Ask:

“Am I ready to fix my financial habits?”

Start today:

- List your debts

- Calculate your real interest

- Take control

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Consult a certified financial advisor before making borrowing decisions.

Author Bio

Mahesh Reddy

Founder, InvestingLens.com

Mahesh writes for Indians who are tired of financial confusion and want clear, honest money advice. His work focuses on debt traps, behavior change, and practical wealth-building strategies.