Best Balance Transfer Cards

If your credit card bill is spiralling out of control, Best Balance Transfer Cards can buy you breathing room before interest turns into financial quicksand. Thousands of Indian salaried professionals are paying 36% to 45% annualized interest without realizing that one smart balance transfer can slash that burden dramatically.

A lot of people think the minimum due shown on the statement is “manageable.” That’s exactly how ₹75,000 quietly becomes ₹1.9 lakh over a few years.

That’s why understanding Best Balance Transfer Cards matters in 2026.

Banks like SBI Card, HDFC Bank, ICICI Bank, Axis Bank, and IDFC FIRST Bank are aggressively competing in the balance transfer segment. Some offer temporary 0% interest periods. Some convert dues into EMI structures. Others reduce repayment pressure with longer tenures.

But here’s the trap nobody talks about:

A balance transfer only works if you stop treating the new card like free money.

According to RBI guidelines, issuers must disclose interest, penalties, and processing fees transparently, but most borrowers still focus only on the EMI amount instead of the total repayment cost. RBI Credit Card Guidelines matter more than flashy cashback ads.

Throughout this guide, we’ll break down the Best Balance Transfer Cards available in India, compare actual costs, show real Indian salary-based examples, explain CIBIL impact, and reveal the biggest mistakes middle-class families make while trying to escape credit card debt.

Key Takeaways

- Best Balance Transfer Cards help move expensive credit card debt to a lower-interest card.

- SBI Card offers temporary 0% balance transfer options for shorter periods.

- HDFC Bank provides longer EMI-based balance transfer structures.

- Processing fees can quietly destroy your savings if ignored.

- A good CIBIL score usually improves approval odds and lowers rates.

- Missing even one EMI after transfer can spike costs sharply.

- Balance transfers work best for disciplined borrowers, not impulse spenders.

- RBI regulations require banks to disclose key charges, but borrowers must still compare carefully.

- Debt consolidation without spending control becomes a financial trap.

- Choosing the wrong tenure often increases total repayment cost.

Why Best Balance Transfer Cards Are Exploding in India

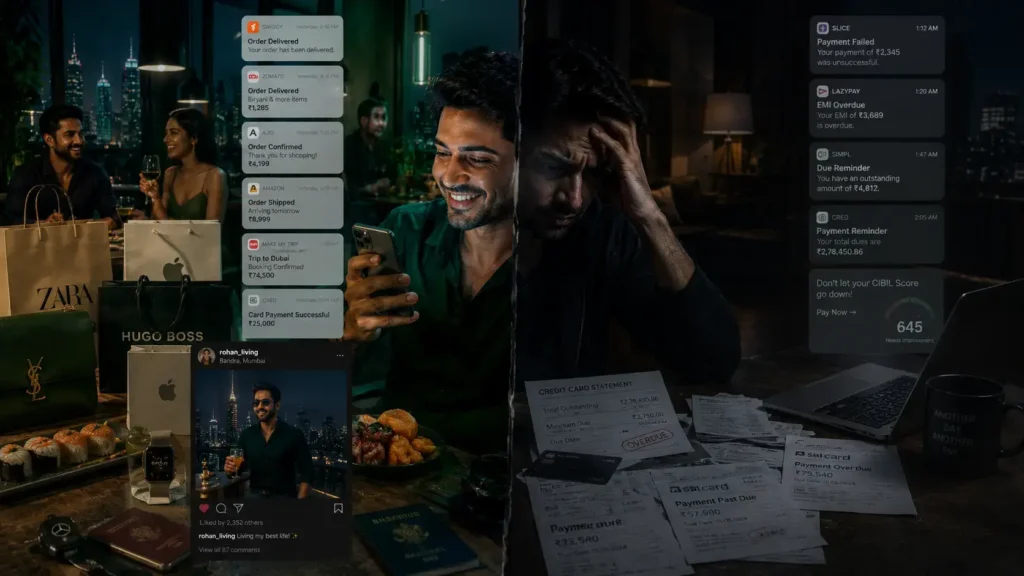

India’s middle-class credit card problem has become brutally visible after the post-pandemic spending boom.

Swiggy orders. Amazon EMI purchases. Goa trips on “No Cost EMI.” iPhone upgrades. Wedding shopping.

None of it feels dangerous in isolation.

But combine three or four credit cards charging 3.5% monthly interest, and suddenly a ₹1 lakh outstanding becomes a full-blown financial emergency.

That’s exactly why searches for Best Balance Transfer Cards have exploded across India in 2025 and 2026.

According to issuer comparison data, banks like SBI Card, HDFC Bank, ICICI Bank, and Axis Bank are aggressively promoting balance transfer facilities because customers are struggling with revolving credit debt.

The Indian Reality Nobody Talks About

Take Rohit from Hyderabad.

Age: 34

Salary: ₹92,000/month

Family: Wife + 1 child

Credit Cards: SBI, HDFC, ICICI

Rohit never considered himself irresponsible.

But over two years:

- ₹1.2 lakh wedding travel expenses

- ₹48,000 medical emergency

- ₹65,000 furniture purchase

- ₹22,000 IPL betting losses he hid from his wife

Total outstanding quietly crossed ₹2.6 lakh.

Minimum due looked manageable at ₹11,000 monthly.

The actual problem?

At 3.5% monthly interest, he was paying almost ₹9,100 monthly in interest alone.

Meaning:

Most of his payment wasn’t reducing debt.

It was feeding the bank.

That’s where Best Balance Transfer Cards become powerful.

Instead of continuing at 36%–45% annualized rates, balance transfer facilities can temporarily reduce repayment costs significantly. Some SBI Card offers even provide 0% short-term windows.

But here’s the Devil Advisor truth:

Most Indians use balance transfers emotionally instead of strategically.

They transfer debt…

Then continue spending again on the old card.

Now they have:

- Old debt

- New EMI

- New purchases

- Double financial stress

That’s not debt management.

That’s financial self-destruction with better packaging.

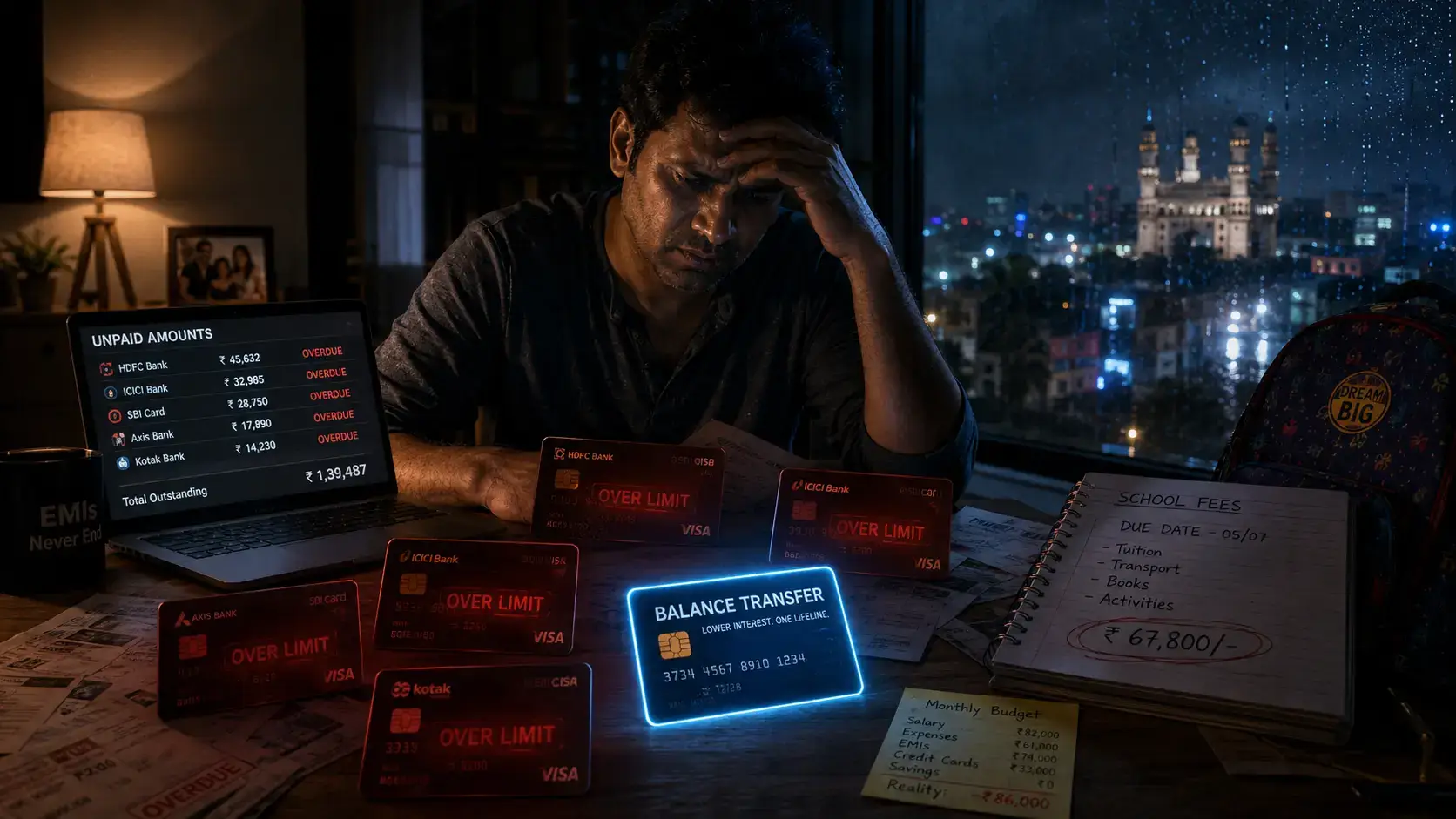

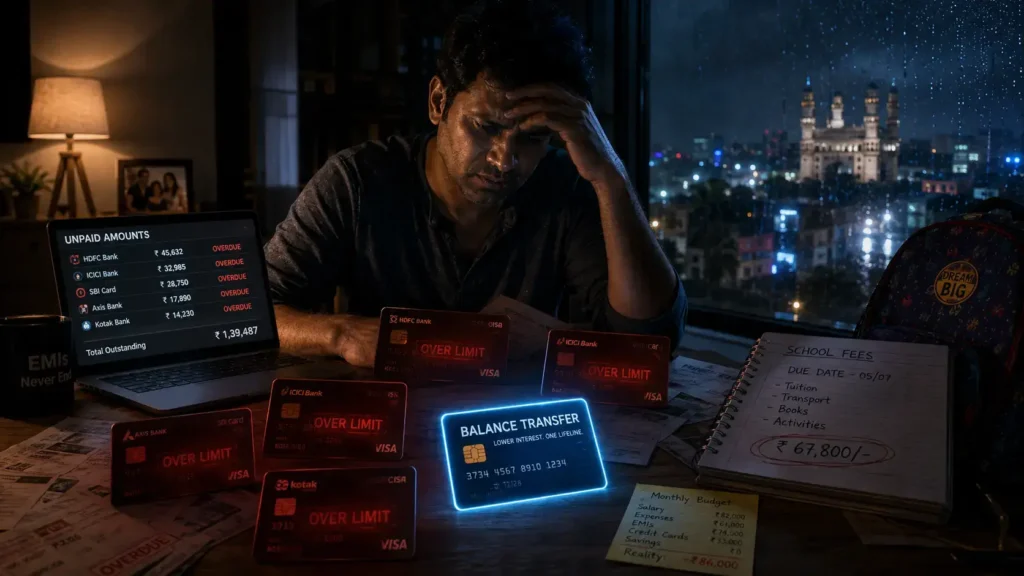

Real Cost Comparison: Minimum Due vs Balance Transfer

| Scenario | Outstanding | Interest Rate | Monthly Payment | Total Repayment |

|---|---|---|---|---|

| Minimum Due Trap | ₹2,00,000 | 42% p.a. | ₹10,000 | ₹3.9 lakh+ |

| Balance Transfer EMI | ₹2,00,000 | 14% p.a. | ₹18,200 | ₹2.18 lakh |

| SBI Short-Term BT | ₹2,00,000 | Promotional | Depends on tenure | Lower short-term burden |

The math is ugly.

Most borrowers underestimate compounding when it works against them.

This is why Best Balance Transfer Cards are not just “credit card hacks.” They’re damage-control tools.

Still, they only work if:

- Spending stops immediately

- EMI payments remain disciplined

- Old cards are not reused recklessly

- Processing fees are calculated upfront

Understanding Credit Utilization becomes essential here because balance transfers also affect your CIBIL score.

You should also understand How Credit Card Interest Works before transferring balances blindly.

RBI’s Warning Signs Indians Ignore

The Reserve Bank of India has repeatedly highlighted rising unsecured retail debt risks. Credit card outstanding levels have surged dramatically in urban India. RBI Official Website

And here’s the scary part:

Many borrowers don’t even know their effective annual interest rate.

They only see:

“Minimum Due: ₹4,287”

That number is psychologically designed to feel manageable.

The bank earns more when you stay in debt longer.

That’s why the smartest users of Best Balance Transfer Cards don’t focus only on EMI affordability.

They focus on:

- Total interest paid

- Processing fee

- Tenure length

- Credit utilization

- Prepayment flexibility

- Post-promo interest rate

IL Advisor Callout

If you cannot stop discretionary spending for even six months, balance transfer cards may actually worsen your financial situation.

Harsh truth:

A balance transfer is not a debt cure.

It is temporary oxygen.

If your lifestyle habits remain unchanged, you’ll eventually suffocate financially again — just on a different card.

Best Balance Transfer Cards Compared in India for 2026

Choosing among the Best Balance Transfer Cards is not about flashy reward points.

It’s about survival math.

Most Indians compare:

- Cashback

- Lounge access

- Joining bonuses

Wrong priorities.

When debt pressure is high, your focus should be:

- Lowest effective interest cost

- Lowest processing fee

- Repayment flexibility

- Fast approval

- CIBIL compatibility

After researching issuer websites, bank disclosures, and comparison platforms, these are currently among the strongest contenders in India.

SBI Card Balance Transfer

SBI remains one of the strongest names in the Best Balance Transfer Cards category because of its short-term promotional structure.

Key highlights:

- 0% interest for selected short tenures

- 180-day repayment options

- Transfer up to 75% of credit limit

- Apply through SMS, app, or online portal

Verified issuer details show:

- 0% for 60-day option

- Around 1.7% monthly for longer tenure plans

- Processing fee applicable depending on tenure

Priya’s ₹1.4 Lakh Escape Story

Priya from Pune worked in HR earning ₹78,000 monthly.

Her mistake:

Using one card to pay another card.

Classic debt spiral.

She finally transferred ₹1.4 lakh outstanding to SBI’s balance transfer facility and aggressively repaid over six months.

Here’s what changed:

| Before Transfer | After Transfer |

| Interest burden: ₹4,800/month | Reduced temporarily |

| Minimum due cycle | Structured repayment |

| Credit score falling | Stabilized after regular payments |

| Anxiety-driven spending | Budget discipline |

But the hidden hero was not the card.

It was behavioral change.

HDFC Bank Balance Transfer on EMI

HDFC dominates among Best Balance Transfer Cards for borrowers needing longer repayment structures.

Features include:

- 9–48 month tenure

- EMI-based structure

- Quick digital approval

- Minimal documentation

This works better for salaried professionals who cannot aggressively repay within 2–3 months.

Example Calculation

Suppose:

- Outstanding debt = ₹3 lakh

- Interest = 1.1% monthly

- Tenure = 24 months

Approx EMI:

₹14,100–₹14,500 monthly

Without balance transfer:

Typical revolving interest could exceed ₹5 lakh total repayment over time.

That’s the brutal difference.

IDFC FIRST Bank CreditPro

IDFC FIRST is becoming increasingly visible in the Best Balance Transfer Cards market because of its “up to 105 interest-free days” positioning.

Key features:

- Up to 105 interest-free days

- Digital activation

- 2% processing fee

- APR applies after free period

This setup works better for:

- Short-term cash flow mismatch

- Salaried professionals expecting bonuses

- Borrowers with temporary liquidity crunch

But there’s a catch.

If repayment discipline fails after the promo period, regular APR kicks in aggressively.

Axis Bank Balance Transfer

Axis Bank offers:

- EMI tenure options

- Competitive rates from around 1% monthly

- Flexible repayment structures

Good fit for:

- Existing Axis customers

- Mid-income salaried users

- Borrowers consolidating multiple smaller cards

IL Advisor Warning

Never choose among the Best Balance Transfer Cards based only on “0% interest.”

Ask:

- For how long?

- What is the processing fee?

- What happens after promo ends?

- Is GST added?

- Can you prepay without penalty?

- Will your old card tempt you into spending again?

That last question destroys more financial recoveries than interest rates ever do.

Best Balance Transfer Cards Comparison Table

| Card Provider | Interest Structure | Tenure | Processing Fee | Best For |

| SBI Card | 0% short-term / 1.7% monthly | 60–180 days | Varies | Fast payoff |

| HDFC Bank | Around 1.1% monthly | 9–48 months | 1%+ | Long tenure |

| Axis Bank | Starts near 1% monthly | Flexible | 1.5% | EMI flexibility |

| ICICI Bank | Bank-dependent | 3–6 months | Variable | Existing customers |

| IDFC FIRST | 105-day structure | Short-term | 2% | Temporary relief |

Before applying for any of these Best Balance Transfer Cards, check your latest credit report and repayment ratio.

You should also read:

For official disclosures and grievance policies:

How to Choose Best Balance Transfer Cards Without Falling Into Another Debt Trap

Most Indians searching for Best Balance Transfer Cards are already under financial pressure.

That pressure changes decision-making.

When panic enters the picture, people stop comparing the total repayment cost and start focusing only on:

- “How low is the EMI?”

- “Can I get approval quickly?”

- “How much temporary relief will I get this month?”

That mindset is dangerous.

Banks know stressed borrowers think emotionally.

That’s why many balance transfer offers are designed to look cheaper upfront while quietly increasing long-term repayment burden through:

- Processing fees

- GST

- Extended tenures

- High post-promo APR

- Foreclosure charges

This is why choosing among the Best Balance Transfer Cards requires calculation — not desperation.

The 5 Metrics That Actually Matter

Most comparison articles online are shallow.

They compare:

- Welcome bonus

- Lounge access

- Cashback

That’s irrelevant when you’re drowning in revolving debt.

Instead, evaluate Best Balance Transfer Cards using these five metrics:

| Metric | Why It Matters |

|---|---|

| Effective Interest Rate | Determines total repayment cost |

| Processing Fee | Hidden upfront cost |

| Promotional Period | Temporary relief duration |

| EMI Flexibility | Impacts monthly cash flow |

| Post-Promo APR | Biggest long-term danger |

The smartest borrowers calculate:

Total repayment amount — not just EMI.

Indian Story: The ₹3.8 Lakh Mistake

Amit from Bengaluru worked in tech support earning ₹1.1 lakh monthly.

He had:

- ₹1.9 lakh on Axis Bank card

- ₹82,000 on ICICI card

- ₹61,000 on Amazon Pay card

Total:

₹3.33 lakh debt.

He searched “Best Balance Transfer Cards” and immediately grabbed the first 0% offer he saw.

Big mistake.

What he ignored:

- 3% processing fee

- GST on fee

- Promo validity only 90 days

- 42% APR after expiry

He failed to clear the amount within 90 days.

Result:

His outstanding started compounding again at brutal rates.

Within 14 months:

Total dues crossed ₹3.8 lakh.

Not because the balance transfer failed.

Because he misunderstood the structure.

IL Advisor Callout

If you don’t read the “post-promotional APR” section, you are gambling with your future.

That tiny footnote is where banks make real money.

Best Balance Transfer Cards for Different Indian Salary Levels

The reality is simple:

Not every balance transfer card suits every income group.

A ₹45,000/month salaried employee should not copy strategies used by someone earning ₹2.5 lakh monthly.

That’s where most financial advice online becomes unrealistic.

Let’s break down Best Balance Transfer Cards by realistic Indian salary segments.

Salaries Below ₹50,000 Monthly

This segment is the most vulnerable.

Why?

Because even a ₹70,000 outstanding can become financially suffocating when:

- Rent consumes 35%

- Fuel prices rise

- School fees increase

- Medical emergencies hit

For this category, the ideal Best Balance Transfer Cards are:

- Short tenure

- Lowest processing fee

- Strict spending freeze

Example

Outstanding:

₹80,000

Without transfer:

- 3.5% monthly interest

- Minimum due cycle

- Repayment stretches endlessly

With transfer:

- EMI around ₹7,500–₹8,000

- Fixed repayment timeline

- Lower overall burden

But only if:

No new shopping happens.

This income category cannot afford balance transfer misuse.

Salaries Between ₹50,000–₹1.2 Lakh

This is India’s biggest urban middle-class segment.

And ironically:

This group often carries the highest lifestyle inflation.

Netflix.

Swiggy.

Weekend malls.

EMIs.

Travel loans.

iPhone upgrades.

The problem isn’t always low income.

It’s invisible leakage.

For this segment, Best Balance Transfer Cards with medium tenure work best.

Good options usually include:

- HDFC Balance Transfer EMI

- SBI Card BT

- Axis Bank EMI conversion

Hard Math Example

| Expense Category | Before Discipline | After Discipline |

|---|---|---|

| Dining Out | ₹12,000 | ₹4,000 |

| Online Shopping | ₹18,000 | ₹5,000 |

| Credit Card EMI | ₹6,500 | ₹14,000 |

| Savings | ₹0 | ₹8,000 |

This is the uncomfortable truth:

Debt recovery often requires temporary lifestyle embarrassment.

That means:

- Saying no to trips

- Delaying upgrades

- Cutting impulse spending

Most people avoid this phase.

That’s why debt survives.

Salaries Above ₹1.5 Lakh

High earners often assume they’re financially safe.

Wrong.

This segment frequently accumulates:

- Luxury lifestyle debt

- Multiple premium cards

- International travel dues

- Gadget EMIs

- BNPL overload

Many high-income professionals searching for Best Balance Transfer Cards are not poor.

They’re over-leveraged.

For them:

Long-tenure EMI structures matter more than promotional 0% periods.

Why?

Because large balances require repayment stability.

Real Indian Scenario: The Consultant Couple

Karan and Sneha from Gurgaon earned a combined ₹3.2 lakh monthly.

Outsiders assumed they were wealthy.

Reality:

- ₹72,000 car EMI

- ₹41,000 home loan EMI

- ₹58,000 credit card debt payments

- International vacation debt

- Child daycare costs

Their combined card outstanding crossed ₹6.4 lakh.

They finally used one of the Best Balance Transfer Cards through HDFC’s EMI transfer structure.

What changed:

- Consolidated payment

- Predictable tenure

- Better budgeting discipline

What didn’t change automatically:

Their spending habits.

That part required brutal honesty.

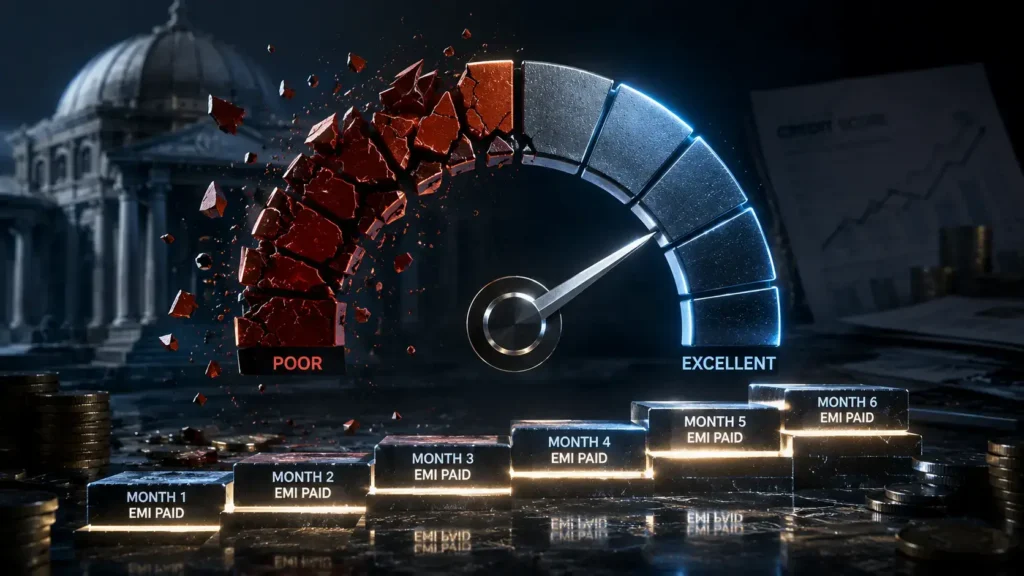

The CIBIL Score Trap

One major misunderstanding around Best Balance Transfer Cards is CIBIL impact.

Many borrowers fear:

“Will applying reduce my score?”

Short answer:

Possibly temporarily.

But long-term disciplined repayment can improve credit health significantly.

Your CIBIL score gets impacted by:

- Hard inquiry

- Credit utilization ratio

- Missed EMIs

- Outstanding balances

According to CIBIL, utilization below 30% is generally healthier for scoring models.

That’s why balance transfer strategies can actually help if they reduce revolving debt pressure responsibly.

You should also understand:

The Hidden Fees in Best Balance Transfer Cards Most Indians Ignore

This section alone can save you thousands.

Because many borrowers compare only interest rates while completely ignoring hidden costs inside Best Balance Transfer Cards.

Here are the most common traps.

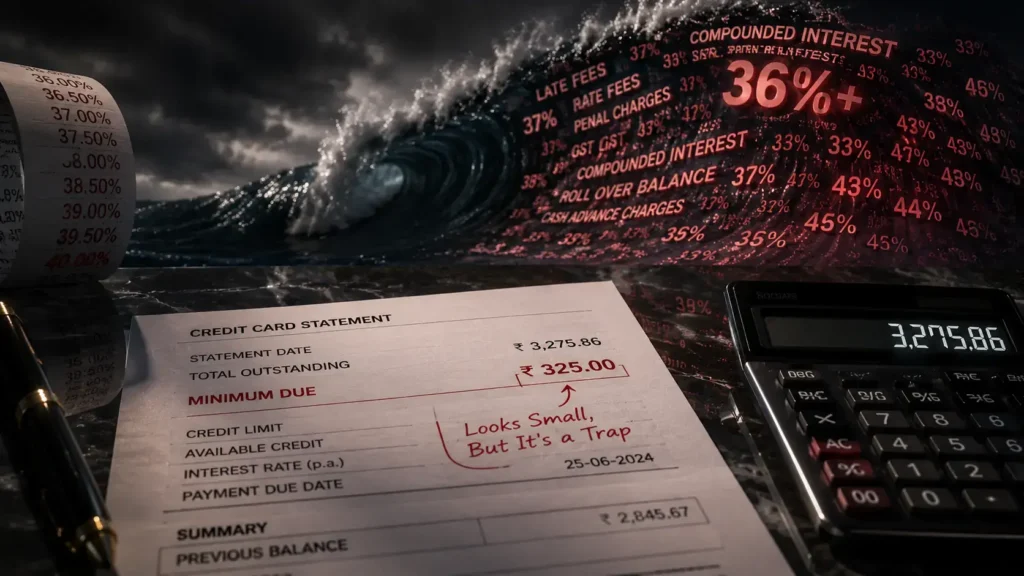

1. Processing Fee

Usually:

1%–3% of transfer amount.

Example:

₹2 lakh transfer at 3% fee:

₹6,000 upfront.

Add GST:

₹7,080 actual cost.

That’s not small.

2. GST on Fees

Most Indians forget GST applies on:

- Processing fee

- Late fee

- Finance charges

The actual effective borrowing cost becomes higher than advertised.

3. Foreclosure Charges

Some balance transfer EMI structures penalize early repayment.

Always ask:

“Can I prepay without penalty?”

4. Post-Promo APR

This is the deadliest trap in Best Balance Transfer Cards.

Banks advertise:

“0% for 90 days”

Borrowers mentally hear:

“Cheap debt”

But after expiry:

APR may jump massively.

Real Cost Breakdown Table

| Component | Amount |

|---|---|

| Transfer Amount | ₹2,50,000 |

| Processing Fee (2%) | ₹5,000 |

| GST | ₹900 |

| Effective Cost Before Interest | ₹5,900 |

| Missed EMI Penalty | Additional charges |

| Post-Promo APR Risk | Very high |

This is why blindly chasing the lowest EMI is financially dangerous.

Reality Check

If your debt exists because of emotional spending habits, no balance transfer card will permanently save you.

Not SBI.

Not HDFC.

Not Axis.

Not IDFC FIRST.

The card changes.

The psychology remains.

That’s the real battle.

The 9-Layer Transformation Story

1. Status Quo

Vikram from Chennai looked successful on Instagram.

Age: 36

Salary: ₹1.45 lakh/month

Corporate job

Weekend pub life

Two premium credit cards

But behind the scenes:

- ₹4.2 lakh outstanding debt

- Multiple BNPL payments

- ₹23,000 monthly interest burden

- Sleepless nights hiding bills from his wife

Minimum due became his survival strategy.

Emotionally, he told himself:

“Next bonus will fix everything.”

It never did.

2. Trigger

One evening, Vikram checked his annual card statement properly for the first time.

Total interest paid in 14 months:

₹1.76 lakh.

Not principal reduction.

Just interest.

That moment shattered him.

He finally started researching Best Balance Transfer Cards seriously instead of ignoring the problem.

3. Mistake

His first instinct was wrong.

He applied for another premium rewards card because it offered airport lounge access and joining perks.

Classic emotional decision.

He cared more about looking rich than becoming financially stable.

4. Wake-Up Call

Things worsened after RBI-regulated late fees and finance charges stacked up. RBI Official Portal

One missed payment triggered:

- Late fee

- GST

- Interest compounding

- Credit score damage

His CIBIL score dropped sharply.

That’s when his home loan eligibility got affected.

Now the debt had real-life consequences.

5. Devil Advisor

His friend finally told him the brutal truth:

“You don’t have an income problem.

You have a lifestyle addiction problem.”

That sentence hurt.

But it was accurate.

6. Calculation

Vikram compared:

- Continuing minimum due

vs - Using one of the Best Balance Transfer Cards

Scenario Comparison

| Option | Estimated Total Cost |

|---|---|

| Continue revolving debt | ₹7 lakh+ |

| Structured balance transfer | ₹4.9 lakh approx |

The gap shocked him.

7. Pivot

He transferred most outstanding to an EMI structure.

Then he made hard decisions:

- Cancelled one premium card

- Stopped weekend bar spending

- Paused gadget upgrades

- Redirected annual bonus into repayment

For the first time, he treated debt like an emergency instead of a temporary inconvenience.

8. Result

Within 19 months:

- Debt cleared

- CIBIL recovered gradually

- Emergency fund started

- Marriage stress reduced significantly

Most importantly:

His financial anxiety stopped controlling his life.

9. Lesson

The real power of Best Balance Transfer Cards isn’t lower interest.

It’s creating breathing room long enough for behavioral change.

Without that second part, the cycle repeats forever.

External Resources:

Internal Reading:

FAQ: Best Balance Transfer Cards in India

Which are the Best Balance Transfer Cards in India right now?

Some of the strongest contenders among Best Balance Transfer Cards in India currently include:

- SBI Card Balance Transfer

- HDFC Balance Transfer on EMI

- Axis Bank Balance Transfer

- IDFC FIRST Bank Credit Card Balance Transfer

- ICICI Bank balance transfer offers

The right choice depends on:

- Your outstanding amount

- Repayment timeline

- CIBIL score

- Monthly income

- Spending discipline

Never choose Best Balance Transfer Cards only because of “0% interest” marketing.

Always compare:

- Processing fees

- GST

- Post-promotional APR

- EMI flexibility

- Foreclosure charges

Official issuer disclosures matter more than influencer reels.

Useful official resources:

Also read:

Do Best Balance Transfer Cards affect CIBIL score?

Yes — but not always negatively.

Applying for Best Balance Transfer Cards may trigger:

- Hard inquiry

- Temporary score dip

However, if the transfer:

- Reduces utilization ratio

- Prevents missed payments

- Creates repayment structure

Then your credit profile can improve over time.

According to CIBIL, maintaining lower utilization and timely repayment are critical scoring factors.

The real danger is:

Using transferred balance space to spend again recklessly.

That creates:

- Higher utilization

- More debt

- Increased repayment stress

Read:

Are Best Balance Transfer Cards really cheaper than paying minimum due?

Usually yes — dramatically cheaper.

Here’s why.

Minimum due systems are designed to extend repayment duration.

Example:

| Scenario | Total Cost |

|---|---|

| ₹2 lakh revolving at 42% p.a. | ₹3.8–₹4 lakh+ |

| Structured balance transfer EMI | ₹2.2–₹2.6 lakh approx |

That difference can literally fund:

- Emergency savings

- Child education SIP

- Health insurance

But the savings disappear if:

- You continue spending heavily

- You miss EMIs

- You ignore post-promo interest rates

That’s why Best Balance Transfer Cards only work when paired with behavioral discipline.

Official financial literacy resources:

Also read:

What CIBIL score is needed for Best Balance Transfer Cards?

Generally:

- 750+ improves approval chances significantly

- 700–750 may still qualify depending on issuer

- Below 650 becomes difficult

But approval also depends on:

- Existing debt ratio

- Income stability

- Employer category

- Repayment history

Many borrowers assume income alone guarantees approval.

Wrong.

A ₹2 lakh salary with reckless repayment history can still create rejection risk.

This is why monitoring your report matters before applying for Best Balance Transfer Cards.

Check official resources:

Internal guides:

Should I close my old credit card after balance transfer?

Not always.

Closing old cards immediately can sometimes:

- Reduce total available credit

- Increase utilization ratio

- Temporarily affect CIBIL score

But keeping old cards active becomes dangerous if:

- You lack spending discipline

- You emotionally overspend

- You use cards for lifestyle validation

For many Indians, the smartest approach is:

- Keep oldest card active

- Reduce unnecessary premium cards

- Disable impulse-heavy cards from shopping apps

The goal is not collecting cards.

The goal is financial stability.

That’s where most users of Best Balance Transfer Cards fail psychologically.

Helpful resources:

Also read:

Conclusion: Best Balance Transfer Cards Can Save You — Or Trap You Again

The biggest myth around Best Balance Transfer Cards is that they magically solve debt problems.

They don’t.

They buy time.

That’s it.

If you use that breathing room wisely:

- You can cut interest burden

- Stabilize cash flow

- Improve repayment structure

- Recover CIBIL score gradually

- Escape the minimum due trap

But if spending habits remain unchanged, even the Best Balance Transfer Cards eventually become another layer of debt.

This is where financial maturity matters more than financial products.

A lot of Indian middle-class professionals are not financially irresponsible because they’re lazy.

They’re exhausted.

They’re juggling:

- Rent

- School fees

- Inflation

- Medical costs

- Family pressure

- Lifestyle expectations

Credit cards become emotional relief.

Then slowly become financial pressure.

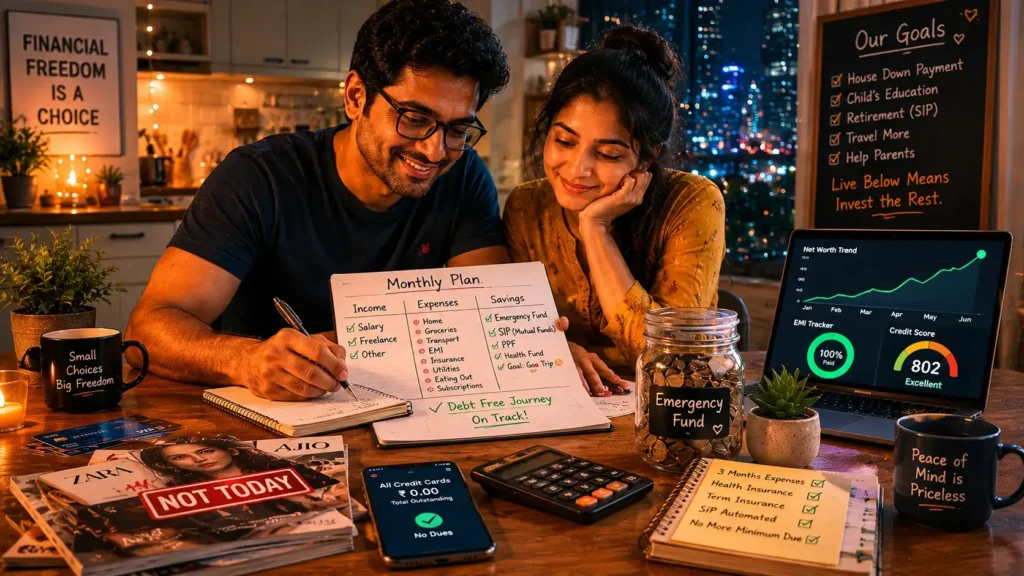

That’s why the smartest move after using Best Balance Transfer Cards is not hunting another rewards card.

It’s building:

- Emergency savings

- Budget discipline

- Spending awareness

- Long-term investing habits

Because debt freedom is not created by one bank offer.

It’s created by repeated boring decisions:

- Paying on time

- Spending less

- Avoiding lifestyle inflation

- Respecting compounding

And remember this brutally honest truth:

Minimum due is not a solution.

It’s a subscription to long-term financial stress.

Before choosing any of the Best Balance Transfer Cards, compare official terms carefully and avoid emotionally driven applications.

Official Sources:

Continue Learning:

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Loan eligibility, interest rates, and repayment outcomes vary based on individual financial situations, lender policies, and market conditions.

Author Bio

Mahesh Reddy is a personal finance educator and founder contributor at InvestingLens, focused on helping Indians make smarter decisions about money, debt, investing, and financial freedom. He writes practical, no-fluff financial content designed for real middle-class Indian households.