Personal Loans for Debt Consolidation: The Middle-Class Escape Plan Nobody Explains Properly

Introduction

Personal Loans for Debt Consolidation are becoming the silent financial lifeline for thousands of Indian middle-class families drowning in multiple EMIs, credit card bills, and BNPL traps. One properly planned consolidation move can turn financial chaos into a manageable repayment system — but one wrong move can make your debt problem 10 times worse.

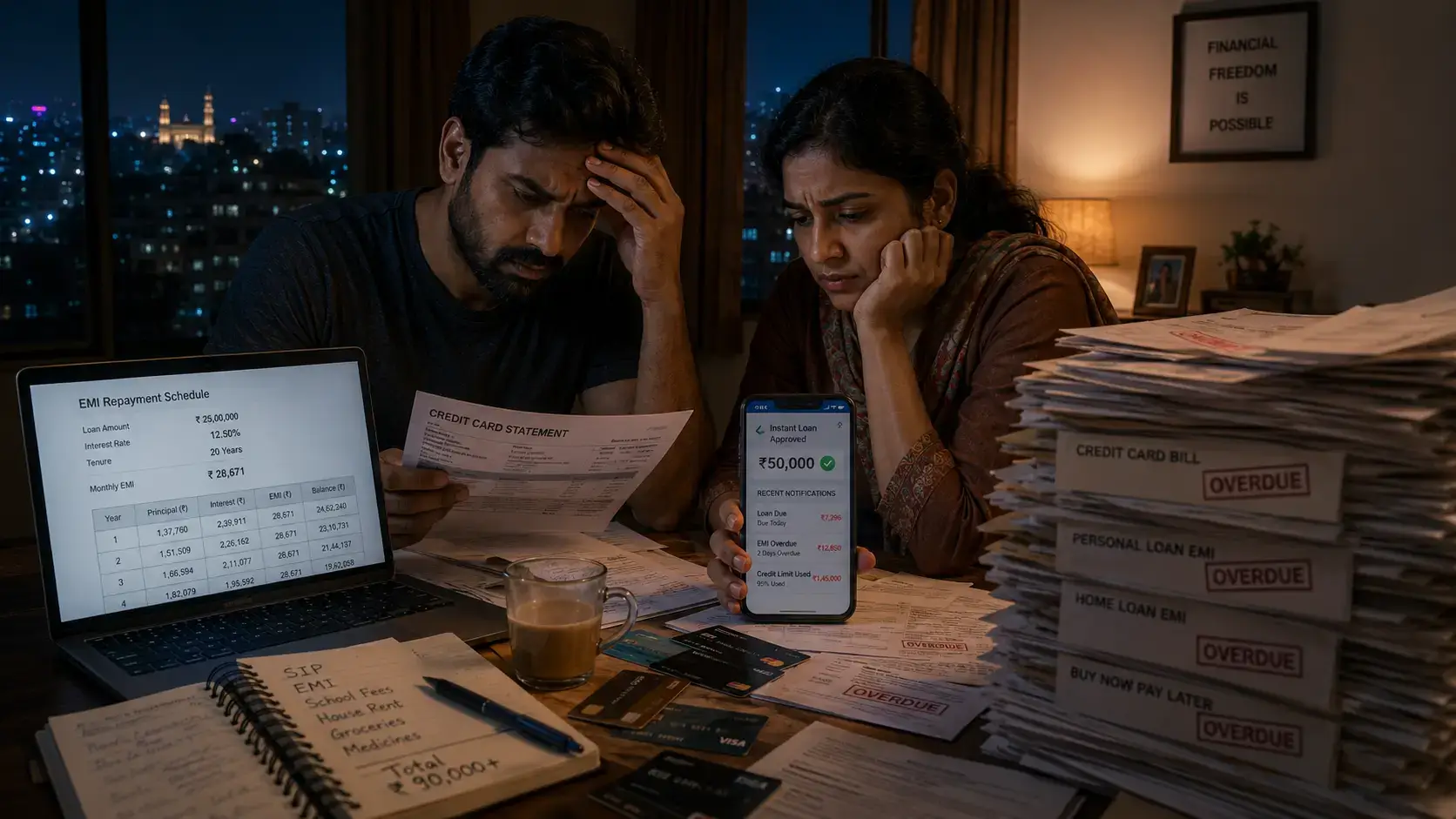

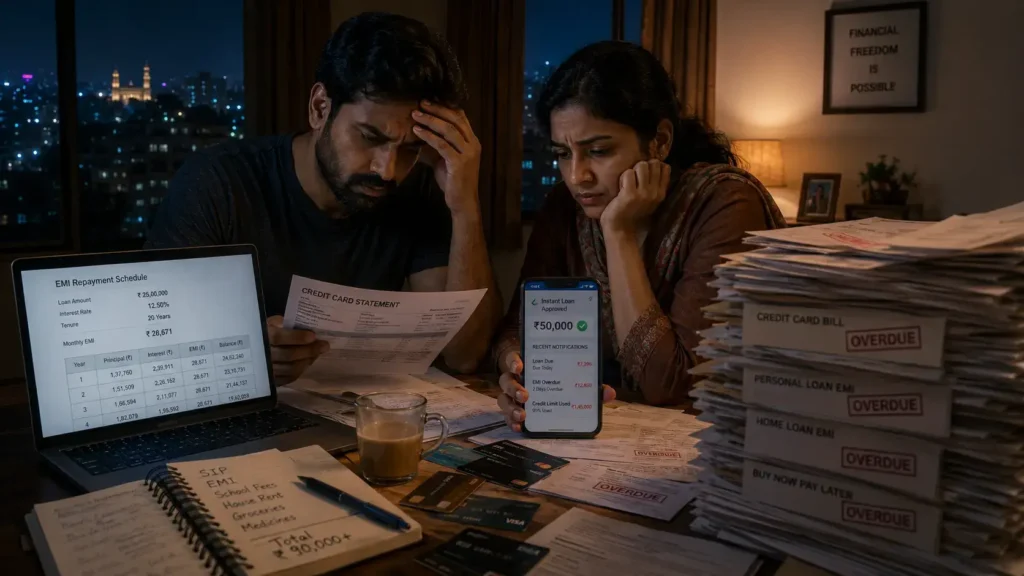

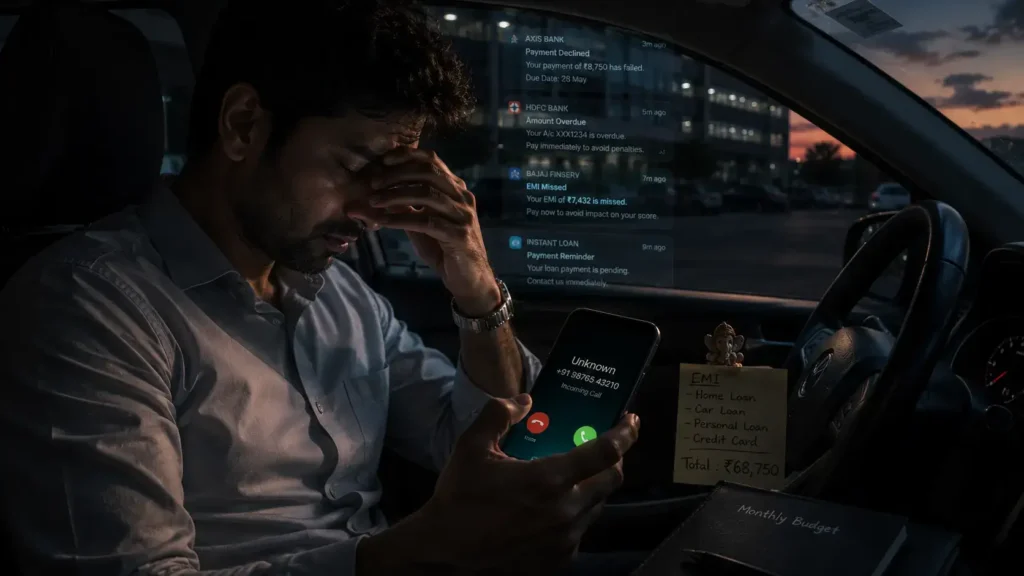

Ravi from Hyderabad thought he was “handling things.” One HDFC credit card. One Amazon Pay Later bill. One bike loan. Two app-based instant loans. Salary: ₹68,000 per month. Total monthly EMIs? ₹41,500.

Then came one delayed payment.

CIBIL dropped from 782 to 689 in six months.

Collection calls started.

His mistake wasn’t borrowing money. His mistake was treating multiple high-interest debts like separate problems instead of one financial emergency.

That’s exactly where Personal Loans for Debt Consolidation can help — if you understand the math, the risks, and the psychological traps.

According to the Reserve Bank of India, unsecured retail lending has seen massive growth in India over the last few years. At the same time, credit card outstanding balances are exploding across urban middle-class households. Many Indians are paying 30%–42% annualized interest without realizing it.

This guide breaks down:

- How Personal Loans for Debt Consolidation actually work

- When they save money

- When they quietly destroy your finances

- EMI calculations with Indian salary examples

- CIBIL score impact

- RBI-linked risks

- Common traps banks never explain

If you’re stuck between salary dates every month, this article may save you lakhs over the next few years.

Key Takeaways

✅ Personal Loans for Debt Consolidation combine multiple debts into one EMI

✅ Can reduce interest burden if used correctly

✅ Works best for credit card debt above 24% interest

✅ Poor discipline can worsen debt dramatically

✅ CIBIL score impact depends on repayment behavior

✅ Banks market convenience — but the real game is interest spread

✅ Debt consolidation is a tool, not a financial cure

What Are Personal Loans for Debt Consolidation and Why Indians Are Suddenly Using Them

Personal Loans for Debt Consolidation simply mean taking one personal loan to close multiple existing debts. Instead of juggling five different payments, you convert everything into one EMI with one lender.

Sounds simple.

But emotionally, this is where most Indians make disastrous mistakes.

Here’s the reality nobody says loudly enough:

Most debt problems in India are not income problems. They are behavior problems hidden behind convenience apps.

Swiggy. Zomato. Flipkart EMIs. iPhone upgrades. Goa trips on credit cards. Minimum due payments. BNPL apps pretending to be “smart finance.”

By the time people search for Personal Loans for Debt Consolidation, the financial fire has usually been burning for 18–36 months already.

Take Priyanka from Bengaluru.

Monthly salary: ₹92,000.

Here’s what happened slowly over two years:

| Debt Type | Outstanding | Interest Rate |

|---|---|---|

| Credit Card 1 | ₹1,85,000 | 36% |

| Credit Card 2 | ₹92,000 | 42% |

| Consumer Durable EMI | ₹48,000 | 24% |

| Instant App Loan | ₹70,000 | 32% |

Total debt: ₹3.95 lakh.

Total monthly payments: Nearly ₹29,000.

She thought she was “managing” because she never defaulted.

But here’s the brutal math:

At 36% annualized interest, ₹1 lakh debt can quietly become ₹1.9 lakh+ if only minimum dues are paid over time.

That’s the trap.

This is why Personal Loans for Debt Consolidation matter. A bank may offer her a personal loan at 13.5%–16%.

Suddenly:

- One EMI

- Lower interest

- Predictable tenure

- Better repayment visibility

Now compare the numbers.

| Scenario | Monthly EMI | Total Interest |

|---|---|---|

| Multiple Debts | ₹29,000+ | Extremely High |

| Consolidated Loan | ₹12,800 | Controlled |

This is where smart borrowers win.

But here comes the “IL Advisor” truth.

IL Advice

Most people misuse Personal Loans for Debt Consolidation.

They consolidate debt…

…and then start using credit cards AGAIN.

That’s how ₹4 lakh debt becomes ₹9 lakh debt.

Banks love these customers.

Because now:

- Old debt exists in new form

- Credit cards reopen

- Spending behavior remains unchanged

Debt consolidation without behavior correction is like mopping the floor while the tap is still running.

The RBI has repeatedly warned about rising unsecured lending exposure in India. Read official lending guidelines here:

Now let’s talk about CIBIL score impact because this is where many borrowers panic unnecessarily.

How Personal Loans for Debt Consolidation Affect CIBIL Score

Initially, your score may dip slightly because:

- New loan inquiry happens

- Fresh unsecured loan appears

But over 6–12 months, scores can improve if:

- Credit utilization falls

- Credit card balances become zero

- EMIs are paid on time

Example:

| Factor | Before Consolidation | After Consolidation |

|---|---|---|

| Credit Utilization | 88% | 12% |

| Missed Payments | Frequent | Zero |

| EMI Clarity | Poor | Structured |

| CIBIL Score | 691 | 756 |

That’s why many financially disciplined borrowers use Personal Loans for Debt Consolidation strategically instead of emotionally.

Internal resources worth reading:

Another important reality:

Not everyone should take Personal Loans for Debt Consolidation.

Avoid it if:

- Your income is unstable

- You already defaulted repeatedly

- You have gambling/spending addiction

- You plan to borrow again immediately

- Your EMI-to-income ratio already exceeds 55%

The goal is not emotional relief.

The goal is mathematical control.

And those are very different things.

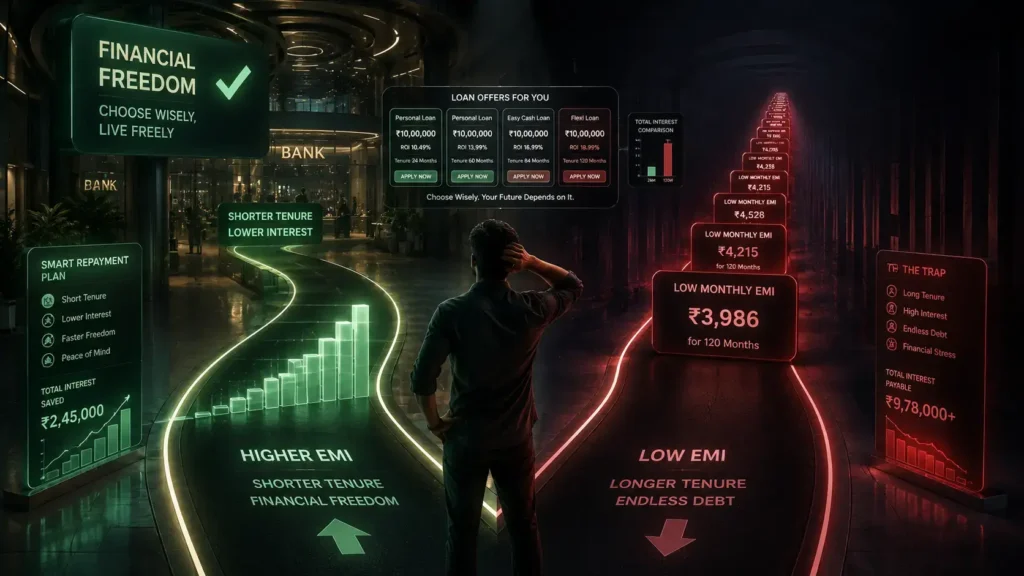

When Personal Loans for Debt Consolidation Actually Save You Money

Here’s the biggest myth in Indian personal finance:

“Lower EMI means better financial decision.”

Wrong.

Banks know middle-class Indians focus emotionally on EMI size, not total repayment cost.

That’s why understanding the real economics behind Personal Loans for Debt Consolidation matters.

Let’s use a realistic Indian scenario.

Arjun from Pune earns ₹1.1 lakh monthly after tax.

Current debts:

| Debt | Outstanding | Interest |

|---|---|---|

| Credit Card | ₹2,20,000 | 38% |

| Personal Loan | ₹1,80,000 | 16% |

| Consumer Loan | ₹75,000 | 22% |

Total debt = ₹4.75 lakh.

Current total EMI burden = ₹37,400.

Bank offers him Personal Loans for Debt Consolidation at:

- Loan Amount: ₹5 lakh

- Interest Rate: 14%

- Tenure: 5 years

New EMI = Around ₹11,634.

Immediately, Arjun feels relief.

But here’s what smart borrowers calculate before signing.

The Hard Math Behind Personal Loans for Debt Consolidation

| Scenario | Total Monthly Outflow | Total Interest Paid |

|---|---|---|

| Existing Debts | ₹37,400 | Very High |

| Consolidated Loan | ₹11,634 | ~₹1.98 lakh |

Now comes the subtle trap.

Longer tenure reduces EMI but can increase total interest if borrowers stretch repayment unnecessarily.

For example:

| Tenure | EMI | Total Interest |

|---|---|---|

| 3 Years | ₹17,099 | Lower |

| 5 Years | ₹11,634 | Higher |

| 7 Years | ₹8,560 | Much Higher |

This is where emotionally exhausted borrowers make bad decisions.

They choose comfort today instead of financial freedom faster.

Example

If your salary increases every year but your loan tenure also keeps increasing, you are not progressing financially.

You are just refinancing stress.

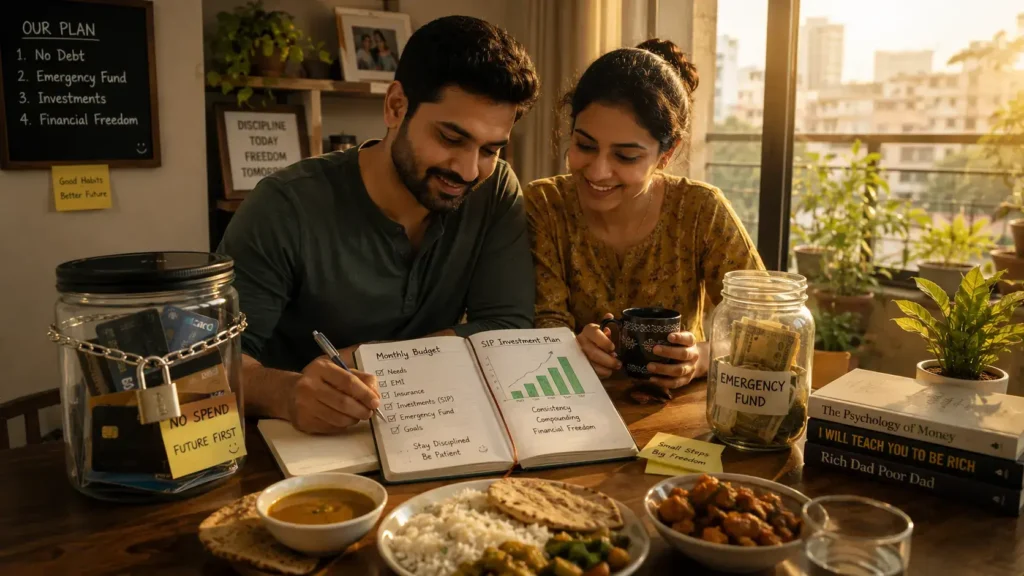

That’s why the smartest use of Personal Loans for Debt Consolidation follows this strategy:

- Consolidate high-interest debt

- Stop using credit cards temporarily

- Build emergency fund

- Increase EMI yearly

- Close loan early aggressively

Now let’s discuss something banks quietly avoid explaining.

Processing Fees and Hidden Costs

Many Indians focus only on interest rates while ignoring:

- Processing fees

- Insurance bundling

- GST charges

- Foreclosure penalties

- Bounce charges

Example:

| Hidden Charge | Approximate Cost |

|---|---|

| Processing Fee | 1%–3% |

| GST | 18% on fees |

| EMI Bounce | ₹500–₹1,200 |

| Late Payment Penalty | 2%–3% monthly |

Read official consumer lending regulations:

Now let’s talk psychology because this matters more than spreadsheets.

Why Most Debt Consolidation Plans Fail

Because people solve debt mathematically but continue spending emotionally.

Example:

- Consolidation reduces EMI by ₹18,000

- Person feels “financially relaxed”

- Starts upgrading lifestyle again

- Uses cards again within 4 months

Result?

Double debt cycle.

This is extremely common among urban salaried employees aged 28–40.

The real success formula behind Personal Loans for Debt Consolidation is behavioral restraint.

Not just lower interest.

Who Benefits Most From Personal Loans for Debt Consolidation

Usually:

- Salaried employees with stable income

- People with good repayment history

- Borrowers with high credit card interest

- Individuals with improving cash flow

Worst candidates:

- Chronic overspenders

- Job instability cases

- Serial app-loan borrowers

- People hiding debt from family

One final uncomfortable truth.

Debt consolidation does not create wealth.

It creates breathing room.

What you do with that breathing room decides whether your future improves or collapses again.

Hidden Risks of Personal Loans for Debt Consolidation Most Banks Won’t Explain

Personal Loans for Debt Consolidation can absolutely reduce financial pressure — but they can also become a long-term financial trap if borrowers misunderstand how banks make money from debt restructuring.

Here’s the uncomfortable truth:

Banks are not emotional support systems.

They are businesses.

And financially stressed borrowers are highly profitable customers.

That doesn’t mean Personal Loans for Debt Consolidation are bad. It simply means you must understand the game before entering it.

Take the case of Sameer from Mumbai.

Monthly salary: ₹78,000.

He had:

- ₹2.8 lakh credit card debt

- ₹1.2 lakh instant loan debt

- ₹65,000 BNPL liabilities

Total: ₹4.65 lakh.

A bank executive convinced him to take a 7-year debt consolidation loan because:

“Sir, EMI sirf ₹8,900 ayega.”

Emotionally, it felt like rescue.

But financially?

Disaster.

Why?

Because he focused only on EMI affordability instead of total repayment cost.

The Real Cost Trap in Personal Loans for Debt Consolidation

Here’s what Sameer didn’t calculate.

| Loan Tenure | EMI | Total Repayment |

|---|---|---|

| 3 Years | ₹15,900 | ₹5.72 lakh |

| 5 Years | ₹11,200 | ₹6.72 lakh |

| 7 Years | ₹8,900 | ₹7.47 lakh |

That “comfortable EMI” added nearly ₹1.75 lakh extra repayment compared to a shorter tenure.

This is one of the biggest hidden dangers in Personal Loans for Debt Consolidation.

Warning

Banks market emotional relief.

Smart borrowers calculate financial impact.

Those are two completely different mindsets.

Many Indians unknowingly convert short-term debt stress into decade-long repayment fatigue.

That’s why you must ask:

- Am I reducing debt?

- Or am I extending debt?

There’s another hidden issue most borrowers ignore.

Debt Consolidation Can Hurt Financial Discipline

Here’s the classic Indian middle-class cycle:

- Person consolidates debt

- Credit cards become “empty” again

- Emotional spending restarts

- Emergency fund still doesn’t exist

- New debt accumulates

Suddenly:

- Old debt still exists as personal loan

- New credit card debt returns

- Total liabilities explode

This is why Personal Loans for Debt Consolidation fail psychologically for many borrowers.

The debt wasn’t the root issue.

The lifestyle was.

Read RBI consumer lending advisories:

Helpful internal reads:

Now let’s discuss something that rarely gets discussed openly in Indian finance blogs.

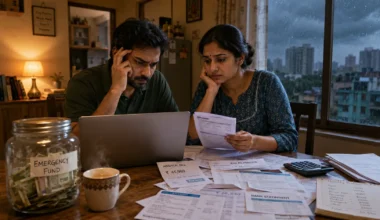

Family Pressure and Hidden Debt

In many Indian households:

- Debt is hidden from spouse

- Parents don’t know loan burden

- Financial shame delays action

This creates emotional paralysis.

Take Kavitha from Chennai.

Salary: ₹64,000.

She secretly accumulated:

- ₹1.7 lakh shopping debt

- ₹90,000 travel EMI debt

- ₹55,000 app-loan obligations

By the time she explored Personal Loans for Debt Consolidation, her monthly obligations crossed ₹31,000.

Nearly half her salary.

One delayed salary cycle triggered:

- Collection calls

- Mental stress

- Panic borrowing

- New payday loans

The consolidation loan itself wasn’t the solution.

The turning point happened when she:

- Cut discretionary spending

- Shared finances honestly with family

- Closed unused credit cards

- Built ₹50,000 emergency reserve

That’s the part many blogs ignore.

Debt recovery is emotional before it becomes mathematical.

How to Use Personal Loans for Debt Consolidation Safely

Here’s the practical framework smart borrowers use.

| Step | Action |

|---|---|

| Step 1 | List every debt clearly |

| Step 2 | Identify highest interest loans |

| Step 3 | Compare consolidation offers |

| Step 4 | Avoid long unnecessary tenures |

| Step 5 | Freeze new credit usage |

| Step 6 | Build emergency savings |

| Step 7 | Increase EMI with salary hikes |

This approach transforms Personal Loans for Debt Consolidation from a panic move into a structured financial reset.

Another major point:

Should You Close Credit Cards After Consolidation?

Not always.

Closing all cards can reduce total credit limit and affect utilization ratio.

Instead:

- Keep oldest card active

- Reduce unnecessary limits

- Disable impulsive online usage

- Use auto-pay for bills only

Smart credit behavior matters more than emotional “card cutting.”

Official consumer credit guidance:

Internal resources:

The bottom line?

Personal Loans for Debt Consolidation work brilliantly for disciplined borrowers.

But for impulsive spenders, they often become a temporary bandage over a growing financial wound.

Best Strategy to Choose Personal Loans for Debt Consolidation in India

Choosing the wrong lender for Personal Loans for Debt Consolidation can quietly cost you lakhs over time.

And unfortunately, most borrowers compare only one thing:

“Kitna EMI ayega?”

That’s it.

But experienced borrowers compare:

- Interest structure

- Processing fees

- Prepayment rules

- Floating vs fixed rates

- Foreclosure flexibility

- Insurance bundling

- Customer support quality

Because the cheapest-looking loan is not always the cheapest actual loan.

Let’s understand this with a realistic example.

Rahul from Gurgaon earns ₹1.45 lakh monthly.

Current debts:

- Credit card debt: ₹3.2 lakh

- Personal loan: ₹2 lakh

- Consumer loan: ₹1 lakh

Total liabilities: ₹6.2 lakh.

Three lenders offered him Personal Loans for Debt Consolidation.

| Lender | Interest | Processing Fee | Tenure |

|—|—|—|

| Bank A | 13% | 3% | 7 years |

| Bank B | 14.5% | 1% | 5 years |

| NBFC C | 12% | 5% | 8 years |

Most borrowers would blindly choose NBFC C because:

“Lowest interest rate.”

But after calculations?

Bank B was actually cheaper overall because:

- Lower hidden costs

- Shorter tenure

- Better foreclosure flexibility

The Real Checklist for Personal Loans for Debt Consolidation

Before signing any loan agreement, verify:

1. Effective Interest Cost

Not just advertised rate.

Ask for:

- APR

- Total repayment amount

- Processing charges

- GST impact

2. Prepayment Rules

Some lenders punish early repayment.

That’s dangerous because the smartest strategy for Personal Loans for Debt Consolidation is aggressive early closure.

3. Loan Insurance Bundling

Many lenders quietly add insurance products.

Example:

- Loan amount approved: ₹5 lakh

- Insurance deducted: ₹22,000

- Actual disbursal: ₹4.78 lakh

But EMI still calculated on ₹5 lakh.

Most borrowers don’t notice this.

Warning

Never sign loan documents in a hurry because a sales executive says:

“Offer expires today.”

Debt decisions made under urgency usually become expensive regrets.

Now let’s discuss the most important factor.

Your EMI-to-Income Ratio

This decides whether Personal Loans for Debt Consolidation help or hurt.

Ideal benchmark:

- Total EMIs below 35% of monthly income

Risk zone:

- Above 50%

Danger zone:

- Above 60%

Example:

| Salary | Safe EMI Limit |

|---|---|

| ₹50,000 | ₹17,500 |

| ₹80,000 | ₹28,000 |

| ₹1,20,000 | ₹42,000 |

This is why many debt consolidation applications get rejected despite good salaries.

Lenders care about repayment capacity more than emotions.

Useful official resources:

Internal reads:

Now here’s another brutal truth.

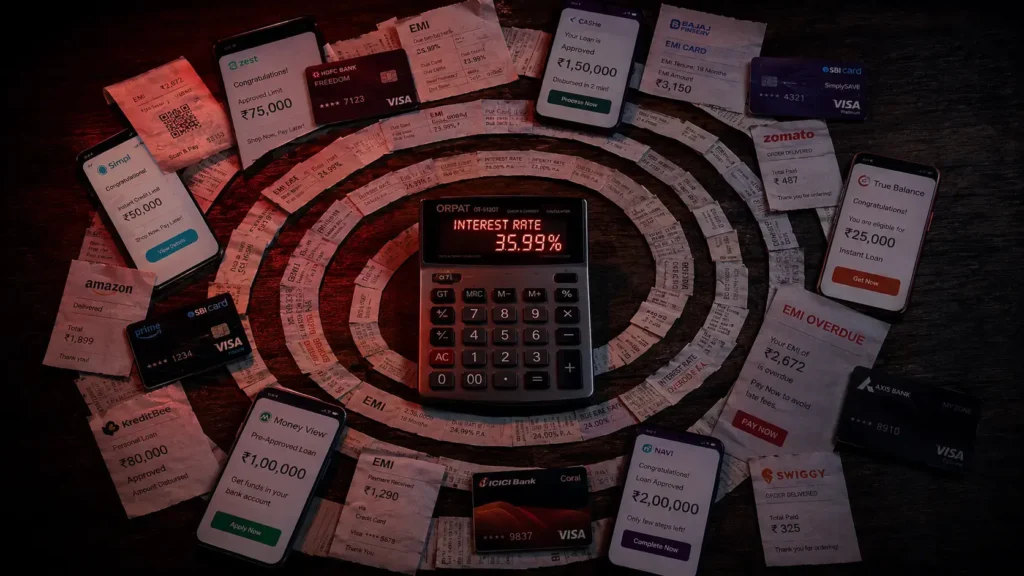

Instant Loan Apps Have Changed Indian Debt Behavior

Many Indians no longer “feel” like they’re borrowing.

Everything feels frictionless:

- One-click loans

- BNPL

- EMI cards

- App-based borrowing

That psychological disconnect is dangerous.

Because when borrowing feels painless, overspending accelerates rapidly.

This is exactly why Personal Loans for Debt Consolidation are exploding in urban India right now.

People aren’t borrowing once anymore.

They’re stacking debt layers silently.

And eventually:

- Salary gets trapped

- Savings disappear

- Investments stop

- Retirement planning collapses

The smartest borrowers use consolidation strategically to reset finances early — before financial damage becomes irreversible.

The 9-Layer Transformation Story: How Personal Loans for Debt Consolidation Changed One Family’s Financial Future

1. Status Quo

Naveen and Swathi from Hyderabad looked financially “stable” from the outside.

Combined income:

- Naveen: ₹78,000

- Swathi: ₹52,000

Total household income: ₹1.3 lakh monthly.

But beneath the surface:

- 3 credit cards

- 1 bike loan

- 2 app-based instant loans

- Consumer durable EMI

- ₹4.9 lakh total liabilities

Monthly EMI burden:

₹63,000.

Nearly half their income disappeared before the 10th of every month.

2. Trigger

One medical emergency changed everything.

Swathi’s father needed hospitalization.

Suddenly:

- Savings exhausted

- Credit cards maxed out

- New app loan taken

That’s when they realized they weren’t financially stable.

They were financially fragile.

3. Mistake

Instead of confronting the problem early, Naveen kept paying:

- Minimum dues

- Partial EMIs

- Delayed payments

His logic:

“Next appraisal ke baad sambhal lenge.”

But interest kept compounding silently.

4. Wake-Up Call

One evening, collection agents started calling repeatedly during office hours.

CIBIL score dropped below 690.

Stress entered their marriage.

That’s when they finally researched Personal Loans for Debt Consolidation.

5. Fact Check Moment

The first bank offered:

- 8-year tenure

- “Very low EMI”

Emotionally attractive.

Financially terrible.

A financially aware friend explained:

“Low EMI is not victory. Lower total interest is victory.”

That changed their approach completely.

6. The Calculation

They consolidated:

- ₹4.9 lakh debt

- 14.2% interest

- 4-year tenure

New EMI:

₹13,400.

Then they added:

- ₹5,000 monthly prepayment

- Bonus-based lump sum closures

7. The Pivot

Lifestyle changes:

- No food delivery for 6 months

- One vacation cancelled

- Credit cards frozen physically

- Emergency fund started

Not glamorous.

But transformative.

8. The Result

Within 28 months:

- Loan mostly cleared

- CIBIL improved to 771

- ₹2.4 lakh emergency fund created

- SIP investing restarted

9. The Lesson

Personal Loans for Debt Consolidation didn’t magically save them.

Behavior change did.

Debt consolidation simply gave them breathing room long enough to rebuild discipline.

And that’s the real purpose of debt consolidation in India today.

Frequently Asked Questions About Personal Loans for Debt Consolidation

1. Are Personal Loans for Debt Consolidation good for credit card debt in India?

Yes, Personal Loans for Debt Consolidation can work extremely well for high-interest credit card debt because credit cards in India often charge 30%–42% annualized interest.

If your consolidation loan comes at:

- 12%–16% interest

- Fixed EMI

- Structured repayment

…you may save significant interest over time.

But there’s a catch.

If you continue spending aggressively on credit cards after consolidation, your debt problem can become much worse.

That’s why financially disciplined borrowers benefit most from Personal Loans for Debt Consolidation.

Official guidance:

Internal reads:

2. Will Personal Loans for Debt Consolidation improve my CIBIL score?

Potentially yes.

Here’s how Personal Loans for Debt Consolidation may improve your CIBIL profile over time:

- Lower credit utilization

- Fewer missed payments

- Structured repayment history

- Reduced dependence on revolving credit

However, your score can temporarily dip because:

- New loan inquiry occurs

- Fresh unsecured loan gets added

Long-term improvement depends entirely on repayment discipline.

If you miss EMIs again after consolidation, your CIBIL score may worsen significantly.

3. Who should avoid Personal Loans for Debt Consolidation?

Not everyone is a suitable candidate for Personal Loans for Debt Consolidation.

Avoid consolidation if:

- Your income is unstable

- You already default frequently

- You continue impulsive spending

- You rely heavily on instant loan apps

- Your EMI-to-income ratio exceeds 60%

Debt consolidation is not a magic reset button.

It’s a structured financial tool that only works when spending behavior improves simultaneously.

Helpful resources:

4. What interest rate is considered good for Personal Loans for Debt Consolidation?

In India, a competitive rate for Personal Loans for Debt Consolidation usually falls between:

- 11%–15% for strong CIBIL profiles

- 15%–20% for moderate-risk borrowers

Your final rate depends on:

- Salary stability

- Employer profile

- Existing obligations

- CIBIL score

- Banking relationship

Remember:

Lower interest rate alone does not mean better loan.

Always calculate:

- Processing fees

- Total repayment amount

- Foreclosure charges

- Insurance deductions

5. Can Personal Loans for Debt Consolidation reduce monthly EMI burden?

Yes.

That’s one of the biggest reasons Indians choose Personal Loans for Debt Consolidation.

Example:

| Existing EMIs | Consolidated EMI |

|---|---|

| ₹38,000 | ₹14,000 |

But lower EMI should not become an excuse for:

- Lifestyle inflation

- New borrowing

- Spending relaxation

The smartest borrowers use reduced EMI burden to:

- Build emergency funds

- Increase investments

- Close loans early

Conclusion: Personal Loans for Debt Consolidation Can Save or Destroy Your Financial Future

Personal Loans for Debt Consolidation are neither good nor bad by default.

They are financial amplifiers.

For disciplined borrowers:

- They simplify repayments

- Reduce interest burden

- Improve cash flow

- Repair CIBIL scores

- Restore mental peace

For reckless borrowers:

- They delay accountability

- Extend repayment periods

- Encourage fresh spending

- Create larger debt cycles

That’s the harsh truth.

The Indian middle class is facing a silent debt crisis today:

- BNPL addiction

- Credit card rollover culture

- Instant loan dependency

- Lifestyle inflation without salary growth

And unfortunately, many people don’t realize the danger until collection calls begin.

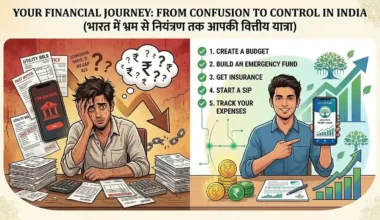

The smartest way to use Personal Loans for Debt Consolidation is:

- Consolidate expensive debt early

- Freeze unnecessary credit usage

- Build emergency savings immediately

- Increase repayment aggressively

- Focus on financial discipline, not just lower EMI

Remember:

Debt consolidation does not create wealth.

It creates breathing room.

What you do after that determines whether your financial future improves or collapses again.

Official financial awareness resources:

Internal guides:

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Loan eligibility, interest rates, and repayment outcomes vary based on individual financial situations, lender policies, and market conditions.

Author Bio

Mahesh Reddy is a personal finance educator and founder contributor at InvestingLens, focused on helping Indians make smarter decisions about money, debt, investing, and financial freedom. He writes practical, no-fluff financial content designed for real middle-class Indian households.