Signs Debt Relief Is a Scam: 11 Red Flags Indians Must Never Ignore

Introduction

When debt starts choking your monthly salary, desperation kicks in fast.

That’s exactly when scammers show up.

They promise:

- “We’ll erase your loan.”

- “Settle credit cards for 90% less.”

- “Increase your CIBIL score instantly.”

- “Stop bank recovery calls permanently.”

Sounds comforting. Until your situation becomes even worse.

Here’s the hard truth most Indians don’t realize:

One of the biggest signs debt relief is a scam is when someone promises instant financial freedom without explaining the consequences.

And sadly, thousands of middle-class Indians are falling for these traps every year — especially people struggling with personal loans, BNPL apps, credit cards, and instant loan apps.

If you’re searching for signs debt relief is a scam, this guide will help you identify the warning signals before you lose more money, damage your CIBIL score, or fall into a deeper financial hole.

Explore CIBIL Score Explained – 7 Important Facts Indians Must Know to know more about CIBIL Score.

Because once scammers have your PAN card, Aadhaar, bank details, and desperation…

You become easy prey.

Key Takeaways

- Genuine debt counselors never guarantee instant loan waivers.

- Upfront fees are one of the clearest signs debt relief is a scam.

- RBI does not authorize private companies to “erase” loans.

- Fake settlement agencies can destroy your CIBIL score for years.

- If someone pressures you emotionally or asks for secrecy, those are major signs debt relief is a scam.

- Debt problems need strategy, not magic solutions.

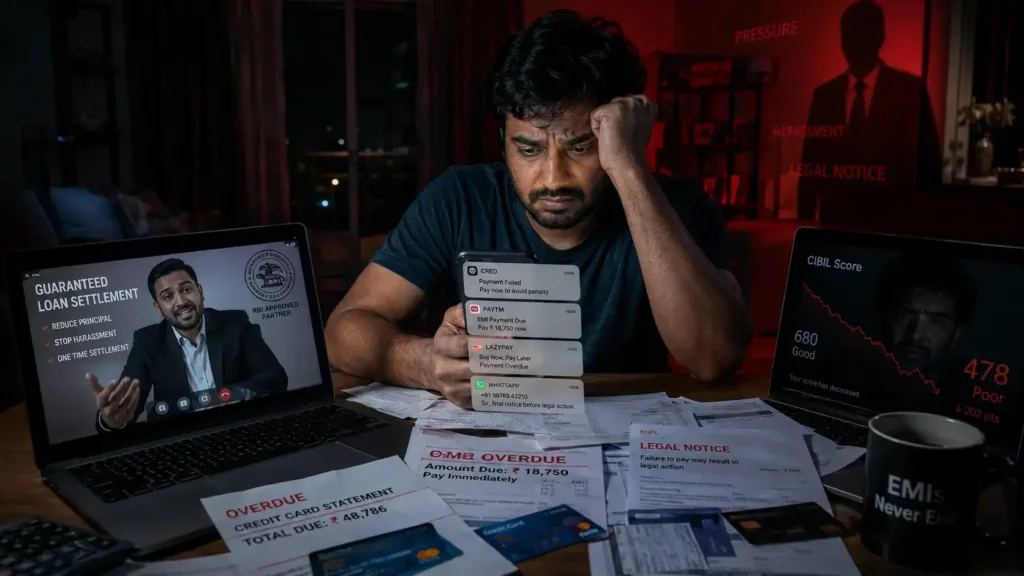

Why Debt Relief Scams Are Rising in India

India’s debt problem has exploded.

Credit cards are easier to get. Personal loans arrive in minutes. BNPL apps push spending aggressively.

But salaries?

Not growing at the same speed.

A 28-year-old earning Rs. 45,000 in Hyderabad can easily end up with:

- Rs. 12,000 personal loan EMI

- Rs. 9,000 credit card minimum dues

- Rs. 4,500 bike EMI

- Rs. 3,000 BNPL repayments

That’s already more than half the salary gone.

Now add rent, groceries, petrol, and family responsibilities.

This financial pressure creates panic.

And panic makes people vulnerable.

That’s why fake “debt settlement experts” are booming on:

- Instagram ads

- WhatsApp forwards

- YouTube comments

- Telegram groups

- Fake finance websites

Many borrowers ignore the early signs debt relief is a scam because they desperately want relief from recovery calls and mounting EMIs.

They don’t sell solutions.

They sell hope to desperate people.

And hope is expensive.

11 Signs Debt Relief Is a Scam

1. They Guarantee Complete Loan Waivers

This is one of the clearest signs debt relief is a scam.

No private company can magically erase your legal debt.

Only lenders can approve:

- settlements

- restructuring

- moratoriums

- waivers in rare cases

If someone says:

“Pay us Rs. 25,000 and we’ll close your Rs. 8 lakh loan permanently.”

Run.

That’s fantasy marketing.

Not finance.

One of the strongest signs debt relief is a scam is when the company avoids explaining how the settlement process actually works.

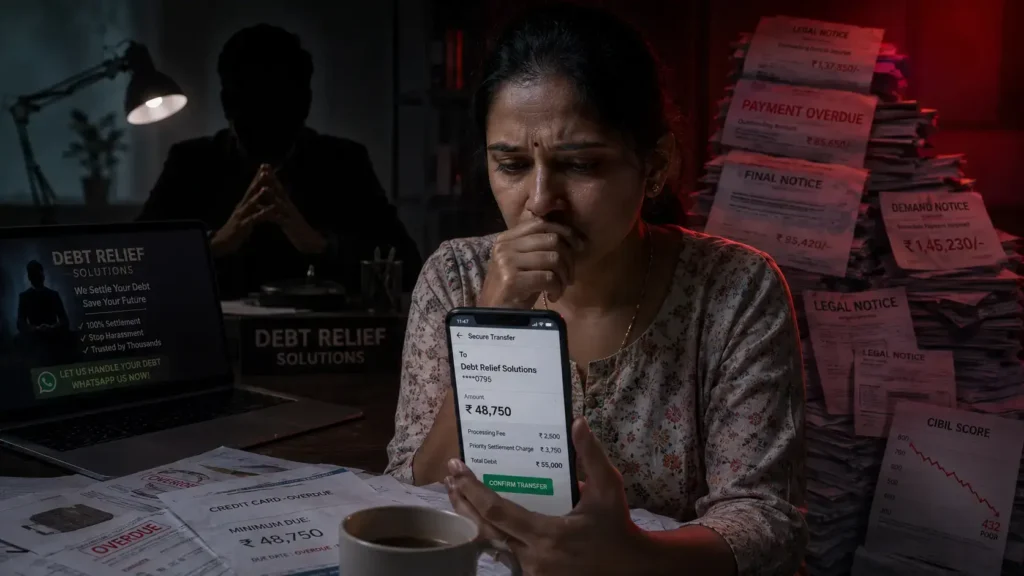

2. They Ask for Large Upfront Fees

Legitimate financial counselors usually charge transparent consultation fees.

Scammers demand aggressive advance payments.

Typical lines include:

- “Processing fee”

- “Legal activation charge”

- “Settlement token”

- “Priority filing fee”

Priya from Pune paid Rs. 40,000 upfront to a debt settlement agency for her Rs. 3 lakh credit card debt.

After payment?

The company stopped answering calls.

Meanwhile, interest and penalties continued growing.

Her debt became Rs. 4.2 lakh within 14 months.

Painful.

But common.

Large upfront charges are among the biggest signs debt relief is a scam in India today.

3. They Tell You To Stop Paying EMIs Immediately

This is dangerous advice.

Many fake agencies intentionally ask borrowers to stop paying lenders completely.

Why?

Because growing defaults increase fear.

And fearful customers stay emotionally dependent.

Here’s what actually happens:

Example Calculation

Suppose Mahesh has:

- Credit card debt: Rs. 2,50,000

- Interest rate: 36% annually

- Minimum due: Rs. 12,000/month

A fake debt company says:

“Stop paying for 6 months. Then we’ll negotiate settlement.”

After 6 months:

- Interest accumulates heavily

- Late payment penalties stack up

- Recovery calls intensify

- CIBIL score crashes

Estimated damage:

- Interest + penalties: ~Rs. 55,000

- CIBIL impact: severe

- Legal notices: possible

Now Mahesh owes around Rs. 3 lakh instead of Rs. 2.5 lakh.

This is how desperation becomes disaster.

If a company tells you to intentionally default before discussing realistic repayment plans, consider it one of the major signs debt relief is a scam.

4. They Promise “Instant CIBIL Repair”

Your CIBIL score doesn’t improve overnight.

Real score improvement takes:

- repayment discipline

- time

- reduced utilization

- corrected reporting

If someone claims:

“Increase your score from 540 to 780 in 7 days.”

That’s a scam signal.

Some fraudsters even use fake screenshots to manipulate borrowers.

Remember:

CIBIL data comes from lenders and credit bureaus — not random Instagram finance pages.

Promises of overnight score improvement are classic signs debt relief is a scam.

5. They Avoid Written Agreements

Scammers hate paperwork.

Why?

Because written commitments create evidence.

If everything happens on:

- WhatsApp calls

- Telegram chats

- verbal promises

Be careful.

A legitimate debt consultant provides:

- fee structure

- service agreement

- timelines

- risks involved

- refund policy

No paperwork = no accountability.

Simple.

And honestly, refusal to provide documentation is one of the oldest signs debt relief is a scam.

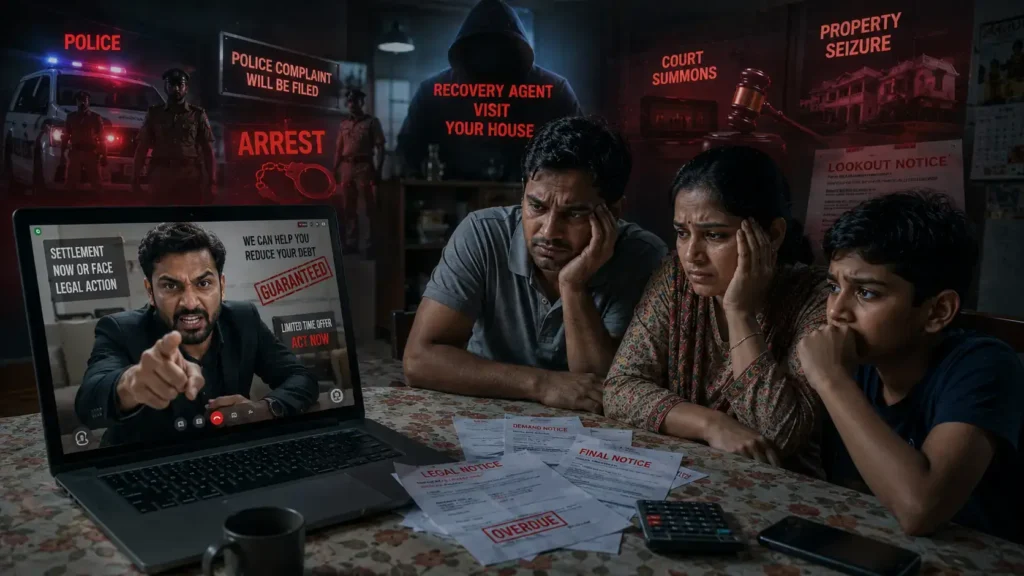

6. They Pressure You Emotionally

Watch for urgency manipulation.

Lines like:

- “Today is the last date.”

- “Your arrest warrant may come.”

- “Recovery agents will visit your house.”

- “Pay now or settlement opportunity closes.”

Classic fear tactics.

Let’s be clear.

In most civil debt cases in India, borrowers are not arrested simply for inability to pay unsecured loans.

Can legal action happen?

Yes.

But scammers exaggerate fear to force rushed payments.

That’s manipulation.

Not financial guidance.

Emotional blackmail is one of the most dangerous signs debt relief is a scam because scared people stop thinking rationally.

7. They Claim RBI Approval Without Proof

Many fake firms misuse RBI logos.

Some even add:

Sounds official.

Usually fake.

The Reserve Bank of India does not officially endorse random private debt relief firms promising guaranteed settlements.

Always verify registrations independently.

Never trust logos blindly.

Fake government branding is one of the most common signs debt relief is a scam online.

8. They Ask for Sensitive Documents Too Early

Be cautious if someone immediately asks for:

- Aadhaar

- PAN

- bank statements

- OTPs

- net banking access

Especially before any formal consultation.

Identity theft is becoming a massive issue in India.

Some scammers:

- open new loans

- misuse KYC

- sell data to telecallers

- access banking accounts

One mistake can haunt you for years.

Aggressive requests for private data are serious signs debt relief is a scam.

9. They Promise “Secret” Loan Closures

A genuine settlement process involves communication with lenders.

But scammers often say:

“Don’t talk to your bank directly.”

Why?

Because they don’t want you discovering the truth.

Real banks already have hardship mechanisms:

- restructuring

- settlement discussions

- temporary relief

- repayment restructuring

Sometimes difficult conversations are uncomfortable.

But hiding from lenders usually makes things worse.

If someone insists on secrecy, that’s one of the strongest signs debt relief is a scam.

10. Their Online Reviews Look Fake

Look carefully.

Fake debt relief companies often have:

- dozens of perfect 5-star reviews

- repeated wording

- no detailed customer stories

- brand-new Google profiles

That’s suspicious.

Real finance businesses usually have mixed reviews.

Because debt itself is emotional and messy.

Perfect reviews in finance are often manufactured.

Suspicious testimonials are underrated signs debt relief is a scam that many borrowers overlook.

11. They Sound Too Good To Be True

This final point matters most.

Debt repayment is usually:

- slow

- uncomfortable

- disciplined

- emotionally exhausting

Anyone selling “easy shortcuts” is often selling lies.

Here’s the uncomfortable truth many people avoid:

If you borrowed money irresponsibly, there is no magical escape button.

There may be:

- negotiation

- restructuring

- settlement

- better planning

But not financial magic.

And accepting reality is the first step toward recovery.

When promises sound unrealistically easy, those are usually the final signs debt relief is a scam.

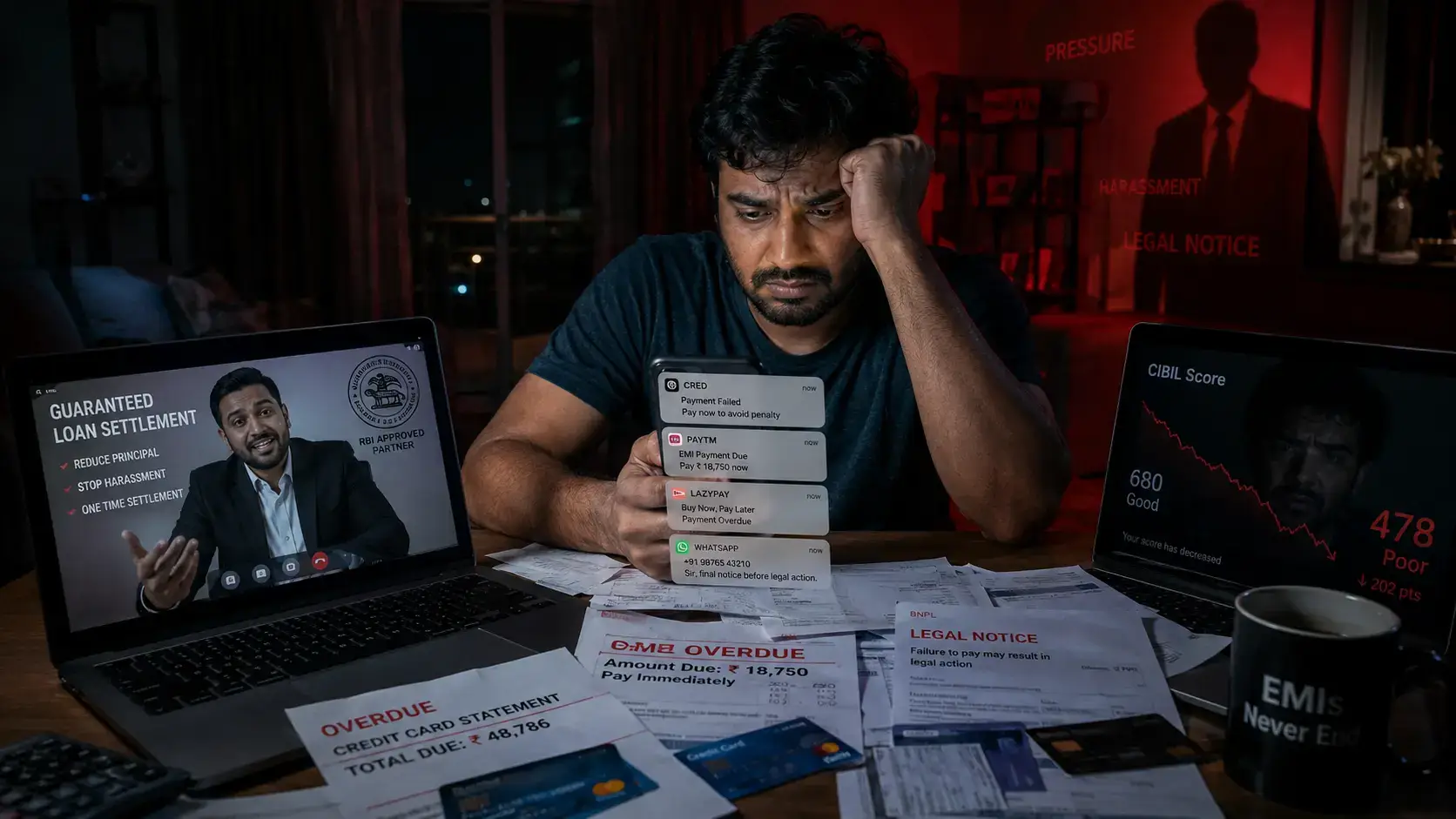

How Fake Debt Relief Companies Trap Indians

Most scams follow a predictable pattern.

Stage 1: Emotional Hook

Ads target vulnerable borrowers:

- “Harassed by recovery agents?”

- “Close loans instantly.”

- “100% settlement guaranteed.”

These emotional promises are often early signs debt relief is a scam.

Stage 2: Fear Amplification

They convince you:

- your situation is urgent

- legal danger is immediate

- lenders are “after you”

Stage 3: Upfront Payment

You pay:

- consultation charges

- legal fees

- activation fees

Usually between Rs. 10,000–Rs. 1 lakh.

Stage 4: Silence

Calls stop getting answered.

Emails bounce.

Office disappears.

Meanwhile:

- debt grows

- CIBIL drops

- stress increases

Cruel.

But extremely common.

How Ravi Lost Rs. 85,000

Ravi, a 32-year-old IT employee from Bengaluru, accumulated:

- Rs. 5 lakh credit card debt

- Rs. 2 lakh personal loan

Monthly salary: Rs. 78,000.

He panicked after receiving collection calls.

A debt settlement company promised:

“We’ll close everything for just Rs. 2 lakh.”

They demanded:

- Rs. 85,000 upfront

- complete EMI stoppage

- exclusive communication rights

Ravi ignored multiple signs debt relief is a scam because he was emotionally exhausted and desperate for relief.

Eight months later:

- no settlements happened

- banks filed recovery escalation notices

- CIBIL score collapsed below 600

- interest ballooned

What hurt most?

Not just money.

Trust.

That emotional damage stays longer than the financial one.

What Legitimate Debt Help Actually Looks Like

Real debt assistance sounds boring compared to scam promises.

That’s usually a good sign.

Legitimate help may include:

- budget restructuring

- lender negotiation

- repayment prioritization

- financial counseling

- debt consolidation guidance

Notice something?

No magic.

Just process.

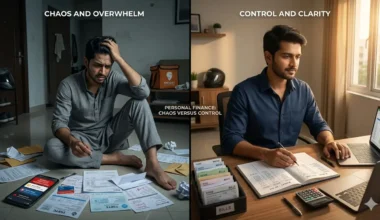

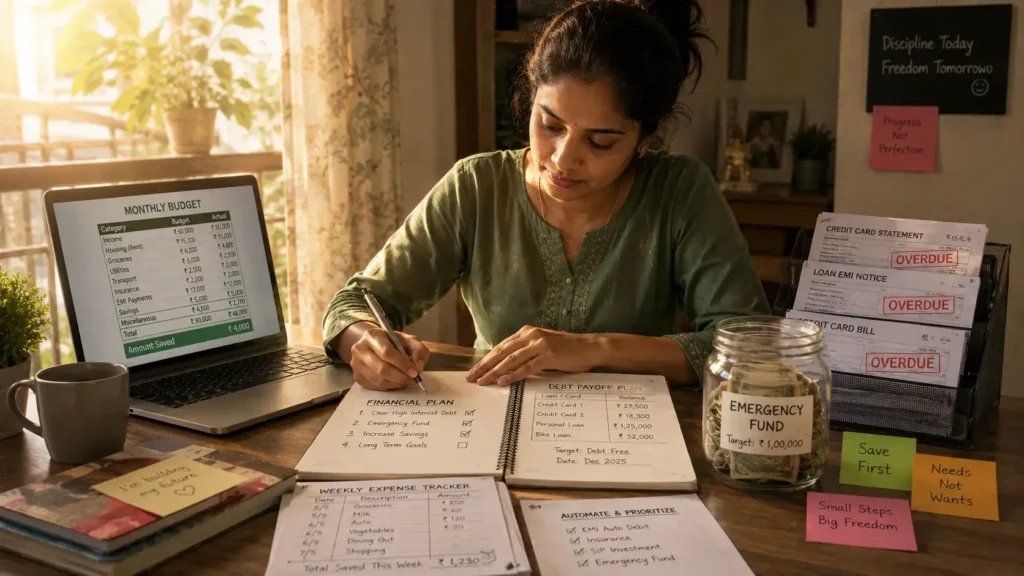

A Realistic Before vs After Scenario

Before

Anita earns Rs. 60,000/month.

Her debt:

- Rs. 3 lakh personal loan

- Rs. 1.5 lakh card debt

Monthly EMIs:

- Rs. 31,000 total

She constantly uses credit cards for groceries.

Classic debt spiral.

After Proper Financial Counseling

Actions taken:

- cut discretionary spending by Rs. 9,000

- negotiated lower EMI tenure

- stopped BNPL usage

- used debt avalanche strategy

12 months later:

- credit card debt reduced significantly

- emergency fund started

- stress reduced

- CIBIL slowly improving

Not glamorous.

But real.

That’s the difference between genuine help and the usual signs debt relief is a scam.

What To Do If You Already Paid a Scam Company

If you suspect fraud, act fast.

Step 1: Stop Further Payments

Do not send “one final fee.”

That’s how scammers squeeze more money.

Step 2: Collect Evidence

Save:

- payment receipts

- WhatsApp chats

- emails

- call recordings

- agreements

Everything matters.

Step 3: Contact Your Lender Directly

Ask:

- whether any settlement was actually initiated

- current outstanding balance

- available hardship options

You may still have time to recover.

Step 4: File Complaints

You can complain through:

- local cybercrime portal

- consumer forums

- police complaint

- RBI Sachet portal for financial fraud awareness

Step 5: Protect Your Identity

If you shared sensitive documents:

- monitor bank accounts

- check CIBIL reports regularly

- watch for unauthorized loans

Identity misuse can continue silently for months.

The faster you respond after noticing signs debt relief is a scam, the lower the long-term damage.

FAQs

What are the biggest signs debt relief is a scam?

Major red flags include upfront fees, guaranteed loan waivers, fake RBI claims, emotional pressure tactics, and requests to stop EMIs immediately.

Is debt settlement legal in India?

Yes, debt settlement itself is legal when negotiated directly with lenders. But many third-party agencies use misleading promises and unethical practices.

Can fake debt relief companies damage my CIBIL score?

Absolutely.

If they convince you to stop payments without proper negotiation, missed EMIs can severely hurt your CIBIL profile for years.

That’s why understanding the signs debt relief is a scam matters so much.

Does RBI approve debt relief companies?

Generally, no.

The RBI does not officially endorse random private firms promising guaranteed debt elimination.

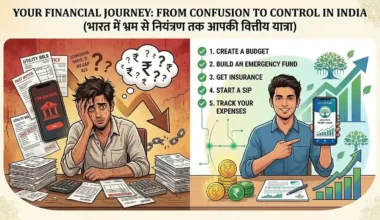

How can I safely reduce debt in India?

Start with:

- budgeting

- direct lender discussions

- structured repayment plans

- certified financial counseling

Avoid miracle promises.

That’s usually where the signs debt relief is a scam begin appearing.

Conclusion

Debt makes people emotional.

And emotional decisions are expensive.

That’s why recognizing the signs debt relief is a scam can literally save lakhs of rupees and years of stress.

Here’s the reality nobody likes hearing:

There’s no shortcut out of financial indiscipline.

No WhatsApp guru.

No “secret RBI settlement.”

No overnight CIBIL fix.

Real recovery looks slower:

- honest budgeting

- painful spending cuts

- disciplined repayment

- difficult conversations

But it works.

And unlike scams, reality doesn’t collapse after the payment clears.

If you’re already struggling with debt, don’t hide from it.

Face the numbers.

Face the habits.

Face the consequences.

That’s where financial freedom actually starts.

And the sooner you recognize the signs debt relief is a scam, the faster you can protect your money, identity, and future.

Disclaimer:

This article is for educational purposes only and should not be considered legal or financial advice. Loan settlement outcomes vary based on lender policies, borrower history, and financial circumstances.

Author Bio

Mahesh Reddy

Mahesh Reddy is a personal finance educator and founder contributor at InvestingLens, focused on helping Indians make smarter money decisions without jargon or fake promises. He writes about debt, investing, budgeting, and financial psychology with a practical India-first approach.