How Credit Counseling Works: The Indian Middle-Class Survival Guide to Escaping Debt Traps

Introduction

How Credit Counseling Works is something most Indians only search for after the damage is already done. Usually after the third recovery call, after the credit card EMI bounces, or after realizing that the “minimum due” trap quietly doubled their debt.

Here’s the blunt truth: credit counseling is not magic. It will not erase your loans overnight. But if used correctly, it can stop financial bleeding, help restructure debt, improve repayment discipline, and slowly rebuild your CIBIL score before your finances collapse completely.

In India, millions of middle-class families are silently drowning in personal loans, Buy Now Pay Later apps, and credit card debt. RBI data already shows rising unsecured lending pressure, especially among salaried urban households. One bad year — job loss, medical emergency, startup failure, divorce, or even reckless lifestyle inflation — can push a ₹3 lakh debt into a ₹7 lakh nightmare.

This guide explains How Credit Counseling Works using real Indian stories, RBI-backed frameworks, Rupee calculations, debt settlement risks, CIBIL impact, and the brutal mistakes most families make too late.

Key Takeaways Box

- How Credit Counseling Works starts with a complete review of your income, expenses, debts, and repayment behavior.

- Good credit counseling focuses on budgeting, repayment restructuring, and financial discipline — not fake “loan waivers.”

- RBI-authorized counseling centers exist through banks and financial literacy programs.

- Credit counseling can help avoid loan defaults and long-term CIBIL damage.

- Minimum due payments on credit cards are one of the biggest financial traps in India.

- Debt settlement and credit counseling are NOT the same thing.

- Families earning ₹50,000–₹1.5 lakh monthly are the most vulnerable to lifestyle-driven debt spirals.

- Genuine counselors educate first. Scammers promise “instant debt removal.”

- Credit counseling works only if spending behavior changes permanently.

- Emotional stress, shame, and denial destroy finances faster than interest rates.

What Is Credit Counseling and Why Indians Are Suddenly Searching for It

Most people searching How Credit Counseling Works are not financially irresponsible. They are financially overwhelmed.

That’s an important difference.

A Bengaluru IT employee earning ₹1.2 lakh monthly can still end up broke. A Hyderabad couple earning ₹18 lakh annually can still default on EMIs. Why? Because debt problems in India rarely start with stupidity. They usually start with optimism.

One personal loan becomes two.

One credit card becomes four.

One EMI becomes twelve.

Then suddenly 65% of monthly salary disappears before the month even begins.

That is where understanding How Credit Counseling Works becomes critical.

Credit counseling is a structured financial guidance process where trained counselors help borrowers:

- Analyze debt

- Review spending patterns

- Create repayment plans

- Negotiate manageable structures

- Improve financial habits

- Prevent defaults

- Rebuild financial stability

Unlike social media “finance gurus,” real counselors don’t scream “invest in crypto” or “10X your money.” They focus on survival first.

In India, many counseling programs are linked to financial literacy initiatives supported by the Reserve Bank of India and banks under borrower assistance frameworks. Genuine counselors help people understand repayment obligations, interest calculations, credit behavior, and budgeting.

You can also learn more about debt management through SEBI Investor Education.

Internal resources:

The Indian Debt Explosion Nobody Wants to Admit

Let’s talk reality.

In 2012, most middle-class Indian households feared debt.

In 2026, debt has become normalized.

Swiggy installments.

iPhone EMIs.

Travel-now-pay-later schemes.

Instant personal loans on apps.

Zero-cost EMI televisions.

Wedding loans.

Bike upgrades.

Furniture financing.

The average salaried Indian today is running a mini-banking ecosystem from their phone.

That’s why searches for How Credit Counseling Works are exploding.

Rahul Story From Pune

Rahul, 33, worked in a multinational IT company earning ₹92,000 monthly after taxes.

Sounds stable, right?

Here’s where things collapsed:

| Expense Type | Monthly EMI |

|---|---|

| Car Loan | ₹16,500 |

| Credit Card EMI | ₹12,000 |

| Personal Loan | ₹14,800 |

| Furniture EMI | ₹5,500 |

| BNPL Apps | ₹4,200 |

| Bike Loan | ₹6,100 |

Total fixed obligations: ₹59,100

After rent and groceries, Rahul had almost nothing left.

Then layoffs hit.

His income dropped to ₹58,000 through freelance work.

Now the math became deadly.

He started paying only minimum dues.

His ₹1.8 lakh card balance carried nearly 36–42% annualized interest.

Within 24 months:

| Item | Amount |

|---|---|

| Original Debt | ₹1.8 lakh |

| Interest + Penalties | ₹1.1 lakh |

| Total Outstanding | ₹2.9 lakh |

This is exactly why understanding How Credit Counseling Works matters before panic begins.

A counselor eventually helped Rahul:

- Freeze unnecessary spending

- Consolidate high-interest debt

- Negotiate repayment sequencing

- Build a survival budget

- Avoid full default

But the painful part?

He could have avoided almost all damage one year earlier.

Brutal Truth

Here’s the uncomfortable truth.

Most Indians don’t have an income problem.

They have an identity problem.

People earning ₹70,000 try to look like people earning ₹2 lakh.

Instagram lifestyles are now financed through EMIs.

The real danger is not debt itself.

The real danger is normalized debt.

When people stop feeling emotional pain while borrowing, disaster starts quietly.

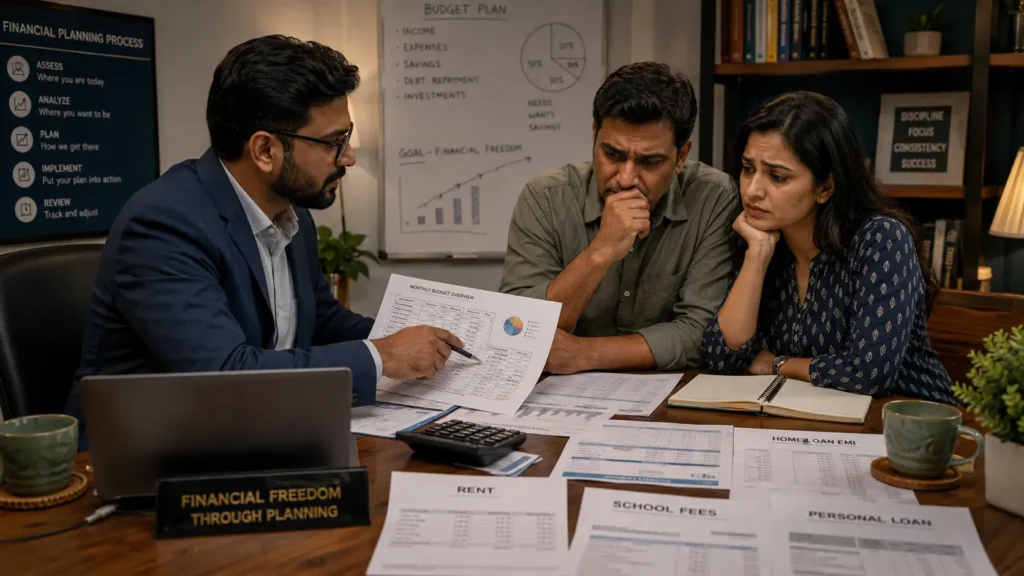

How Credit Counseling Works Inside Banks and Financial Institutions

To truly understand How Credit Counseling Works, you need to know what actually happens during a counseling session.

Most people imagine:

- a scary bank officer

- humiliation

- recovery threats

- legal notices

Good counseling is supposed to be the opposite.

The process usually includes:

- Financial Assessment

- Debt Analysis

- Budget Planning

- Repayment Strategy

- Negotiation Guidance

- Financial Education

- Credit Behavior Correction

Some banks in India offer structured borrower assistance programs aligned with RBI financial literacy frameworks.

You can check official borrower awareness initiatives through:

Internal reading:

Step 1: Full Financial Autopsy

The first thing counselors do is brutal but necessary.

They open every number.

No hiding.

No emotional excuses.

No “next month will be better.”

A proper counseling session examines:

| Category | What Gets Reviewed |

|---|---|

| Salary | In-hand income |

| Fixed Costs | Rent, EMI, school fees |

| Debt | Loans, cards, BNPL |

| Savings | Emergency reserves |

| Insurance | Health & life coverage |

| Spending Habits | Food delivery, shopping |

| Credit Score | CIBIL behavior |

| Late Payments | Existing defaults |

This stage alone shocks many borrowers.

Why?

Because most Indians never calculate their total debt burden honestly.

Sneha and Arvind Story From Hyderabad

Combined monthly salary: ₹1.85 lakh.

Looked financially successful.

Reality:

- 3 credit cards

- ₹11 lakh personal loans

- ₹28 lakh home loan

- International vacation EMI

- Wedding gold loan

They were spending ₹1.34 lakh monthly before groceries.

When the counselor mapped their finances, the couple realized:

- 72% income already committed

- savings rate nearly zero

- emergency fund = ₹18,000 only

One medical emergency could have destroyed them financially.

This is exactly where How Credit Counseling Works becomes life-changing.

Not because the counselor magically removed debt.

Because the counselor forced financial clarity.

Step 2: Debt Prioritization Strategy

Not all debt is equally dangerous.

A good counselor identifies:

- highest interest loans

- legal-risk loans

- emotionally destructive debt

- short-term survival priorities

Example:

| Debt Type | Interest Rate |

|---|---|

| Credit Card | 42% |

| Personal Loan | 18% |

| Home Loan | 9% |

| Gold Loan | 14% |

The biggest emergency is usually revolving credit card debt.

Why?

Because compounding works against you violently.

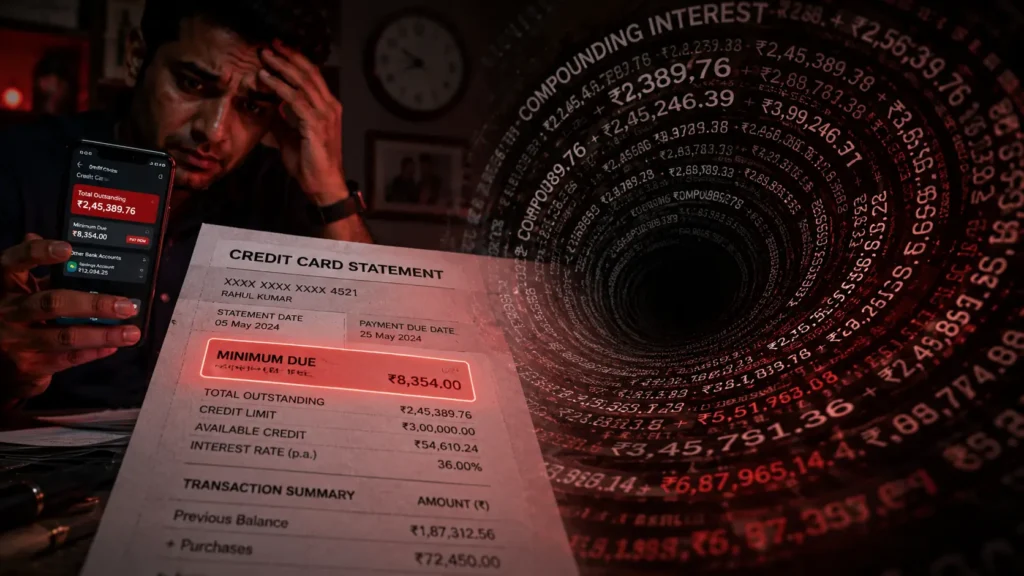

Minimum Due Trap

Suppose:

- Outstanding card balance = ₹3 lakh

- Interest = 3.5% monthly

- Minimum payment = 5%

If borrower keeps paying minimum due:

| Year | Approx Balance Paid |

|---|---|

| 1 | ₹1.1 lakh |

| 3 | ₹3.8 lakh |

| Remaining Debt | Still active |

This is financial quicksand.

Understanding How Credit Counseling Works means understanding how repayment sequencing changes outcomes dramatically.

Step 3: Budget Reconstruction

This is the part people hate most.

Because this is where lifestyle fantasies die.

Counselors often force hard conversations:

- downgrade apartment?

- sell second car?

- stop luxury subscriptions?

- reduce eating out?

- pause vacations?

- delay gadget upgrades?

Brutal Truth

The ₹450 coffee is not the real problem.

The problem is needing emotional validation through spending.

Debt counseling fails when behavior stays unchanged.

A person cannot finance:

- premium lifestyle

- luxury travel

- expensive gadgets

- high SIP goals

- social comparison

all at the same time on a middle-class salary.

Math always wins eventually.

Budget Reset Example

Before Counseling

| Category | Monthly Spend |

|---|---|

| Dining Out | ₹14,000 |

| EMI | ₹63,000 |

| Shopping | ₹11,500 |

| OTT & Apps | ₹4,200 |

| Groceries | ₹13,000 |

| Fuel | ₹9,500 |

Total = ₹1.15 lakh

After Counseling

| Category | Monthly Spend |

|---|---|

| Dining Out | ₹4,500 |

| EMI | ₹63,000 |

| Shopping | ₹2,500 |

| OTT & Apps | ₹800 |

| Groceries | ₹11,000 |

| Fuel | ₹7,000 |

Total = ₹88,800

Monthly savings improvement = ₹26,200

That single difference can prevent long-term default.

And that is one of the most practical outcomes of understanding How Credit Counseling Works properly.

The Hidden Psychology Behind Debt: Why Most Credit Counseling Fails

By now, you understand the technical side of How Credit Counseling Works. But here’s the uncomfortable reality most financial blogs avoid saying:

Debt is rarely just a math problem.

Debt is usually:

- stress

- ego

- comparison

- denial

- emotional spending

- family pressure

- lifestyle addiction

That’s why many people complete counseling sessions… and still end up back in debt two years later.

Understanding How Credit Counseling Works properly means understanding behavioral finance first.

The Emotional Debt Spiral Most Indians Never Notice

A lot of middle-class Indians don’t borrow because they’re irresponsible.

They borrow because they’re exhausted.

Long office hours.

Family obligations.

Social pressure.

Children’s school fees.

Wedding expectations.

Then spending becomes emotional relief.

A ₹3,000 Swiggy order feels “deserved.”

A ₹1.2 lakh iPhone becomes “motivation.”

A Goa trip becomes “mental health.”

The problem is not one expense.

The problem is repeated emotional borrowing.

That’s where How Credit Counseling Works becomes deeper than just budgeting.

Good counselors identify:

- emotional triggers

- impulsive spending patterns

- financial denial behavior

- lifestyle inflation habits

Without fixing those, repayment plans collapse eventually.

Official financial literacy programs from the Reserve Bank of India repeatedly stress responsible borrowing and financial awareness.

You can also study investor discipline frameworks via AMFI India.

Internal reading:

Priya (Name Changed ) Story From Chennai

Priya earned ₹78,000 monthly in a pharmaceutical company.

No major family responsibilities.

No medical emergency.

No job loss.

Yet she accumulated:

- ₹4.6 lakh credit card debt

- ₹2 lakh BNPL liabilities

- ₹1.8 lakh app-based instant loans

What happened?

Emotional spending.

Every stressful work week triggered online shopping.

Every bad month triggered vacations.

Every anxiety phase triggered food delivery spending.

When she finally explored How Credit Counseling Works, the counselor identified something shocking:

Her debt problem was actually a stress management problem.

The financial plan included:

- spending tracking

- autopay discipline

- debt snowball strategy

- removing shopping apps

- reducing credit limits

- therapy recommendation

That combination slowly stabilized her finances.

Not instantly.

But realistically.

Brutal Truth

Here’s a brutal truth.

A lot of people say:

“I deserve this.”

But debt does not care what you deserve.

Interest compounds regardless of emotions.

Banks don’t calculate EMIs based on your intentions.

They calculate based on outstanding balance.

The middle class often tries to reward itself before building financial stability.

That sequence destroys long-term wealth.

Debt Management Plans: The Core Engine Behind How Credit Counseling Works

One of the most misunderstood parts of How Credit Counseling Works is the Debt Management Plan (DMP).

People hear “debt management” and imagine:

- loan waivers

- debt cancellation

- legal escape routes

That’s not how legitimate systems work.

A Debt Management Plan is usually a structured repayment strategy designed to:

- organize debt

- reduce financial chaos

- prioritize repayments

- avoid default escalation

- improve repayment consistency

Some counseling agencies help borrowers negotiate revised payment schedules with lenders.

But understand this clearly:

No genuine counselor promises “100% debt removal.”

That’s usually a scam.

You can verify borrower protection and grievance frameworks through:

Internal resources:

How Debt Management Plans Actually Work

Here’s the typical flow inside a structured counseling process.

Step 1: Debt Mapping

All liabilities are listed.

Example:

| Debt Type | Outstanding | Interest |

|---|---|---|

| Credit Card A | ₹2.2 lakh | 42% |

| Credit Card B | ₹1.1 lakh | 39% |

| Personal Loan | ₹4.5 lakh | 17% |

| Consumer EMI | ₹85,000 | 15% |

Total debt = ₹8.65 lakh

Step 2: Essential Expense Protection

Before repayment planning, counselors calculate survival expenses.

| Essential Category | Monthly Cost |

|---|---|

| Rent | ₹18,000 |

| Groceries | ₹12,000 |

| School Fees | ₹8,000 |

| Insurance | ₹4,000 |

| Utilities | ₹5,000 |

Total essentials = ₹47,000

Suppose salary = ₹82,000.

Available for debt repayment:

₹35,000.

This becomes the realistic repayment base.

That is a core reason understanding How Credit Counseling Works matters — because most borrowers attempt impossible repayment schedules emotionally instead of mathematically.

Step 3: Repayment Prioritization

Counselors may recommend:

- highest interest first

- smallest balance first

- legal-risk first

- settlement evaluation

- restructuring requests

Different borrowers require different strategies.

Example: Avalanche Strategy

| Debt | Interest | Priority |

|---|---|---|

| Credit Card A | 42% | 1 |

| Credit Card B | 39% | 2 |

| Personal Loan | 17% | 3 |

Eliminating high-interest debt first saves huge amounts long-term.

Hard Math: Why Timing Matters

Suppose someone delays repayment action by 24 months.

Scenario A — Immediate Action

| Debt | Amount |

|---|---|

| Initial Credit Card Debt | ₹3 lakh |

| Interest Burden | ₹1.1 lakh |

| Total Repayment | ₹4.1 lakh |

Scenario B — Delayed Action

| Debt | Amount |

|---|---|

| Initial Debt | ₹3 lakh |

| Interest + Penalties | ₹3.8 lakh |

| Legal & Collection Costs | ₹60,000 |

| Total | ₹7.4 lakh |

That’s the hidden danger people ignore until too late.

This is exactly why understanding How Credit Counseling Works early matters enormously.

The 9-Layer Transformation Story

1. Status Quo

Amit Verma, 37, lived in Gurgaon with his wife and daughter. Salary: ₹1.45 lakh monthly.

Outwardly successful.

Inside? Financial collapse.

Three credit cards maxed out.

Personal loan for wedding expenses.

SUV EMI.

Luxury apartment rent.

International vacation debt.

Monthly obligations crossed ₹1.08 lakh.

Still, Amit kept telling himself:

“Next appraisal will fix this.”

2. Trigger

Then his company restructured.

Salary dropped by 28%.

Suddenly:

- EMIs bounced

- recovery calls started

- CIBIL score crashed below 650

That’s when he first searched:

How Credit Counseling Works

3. Mistake

Instead of reducing spending immediately, Amit made classic panic decisions:

- took another instant loan

- transferred balances repeatedly

- paid minimum dues

- hid debt from family

Debt climbed from ₹9 lakh to ₹14.7 lakh.

4. Wake-Up Call

One evening, his daughter asked:

“Why are bank people calling every day?”

That emotional hit broke denial.

5. Brutal Truth

The counselor told Amit something painful:

“You don’t have an income problem. You have a lifestyle alignment problem.”

That sentence changed everything.

6. Calculation

The counselor mapped his reality.

| Category | Amount |

|---|---|

| Salary | ₹1.05 lakh |

| Fixed Survival Expenses | ₹48,000 |

| Available for Debt | ₹57,000 |

Then debt prioritization began.

Luxury spending stopped completely.

Second car sold.

Vacation canceled.

Credit cards frozen.

7. Pivot

Amit followed a structured repayment plan:

- avalanche strategy

- strict budgeting

- side freelance consulting

- debt tracking spreadsheet

- emergency fund creation

Most importantly: no new debt.

8. Result

After 32 months:

- personal loan closed

- two credit cards cleared

- CIBIL improved to 742

- emergency fund reached ₹4.8 lakh

Financial peace returned slowly.

Not magically.

9. Lesson

The biggest lesson Amit learned about How Credit Counseling Works was this:

Counseling cannot save someone committed to denial.

But it can completely transform someone willing to face reality honestly.

Brutal Truth

Middle-class Indians often spend years protecting appearances while silently destroying financial stability.

The irony?

Nobody actually cares about your luxury lifestyle as much as you think.

But your future self will absolutely care about compound debt.

Frequently Asked Questions About How Credit Counseling Works

1. Does credit counseling reduce my loan amount?

Not automatically.

Understanding How Credit Counseling Works means understanding that counselors usually help with:

repayment planning

budgeting

restructuring discussions

financial discipline

lender communication

They do NOT magically erase debt.

Some lenders may offer restructuring or settlements under specific hardship situations, but settlement can severely damage your CIBIL score.

Check official borrower rights through the RBI Banking Ombudsman.

Internal reading:

How Loan Settlements Affect CIBIL Scores

Best Debt Repayment Strategies in India

2. Will credit counseling improve my CIBIL score?

A counselor may help you:

stop missing payments

reduce utilization ratio

organize repayments

avoid defaults

Those actions may gradually improve your credit profile.

But improvement takes time.

If someone promises:

“Instant CIBIL improvement”

be extremely careful.

That’s usually a red flag.

You can learn about responsible credit behavior from CIBIL and RBI Financial Literacy.

It can help indirectly.

3. Is credit counseling free in India?

Some programs are free.

Some private agencies charge fees.

Bank-linked or RBI-supported financial literacy initiatives may offer low-cost or free guidance.

Before signing anything:

verify registration

check reviews

avoid advance-payment scams

read agreements carefully

A legitimate counselor explains risks openly.

Scammers promise miracles.

That difference matters hugely when learning How Credit Counseling Works.

Internal resources:

How to Avoid Financial Scams in India

Best Financial Habits for Salaried Employees

4. Is debt settlement the same as credit counseling?

Absolutely not.

This is one of the biggest misconceptions around How Credit Counseling Works.

Credit Counseling

Focuses on:

budgeting

repayment planning

financial education

debt management

Debt Settlement

Usually involves:

negotiating reduced repayment

partial closures

settlement remarks on credit reports

Debt settlement can impact future loan eligibility negatively.

Always understand the consequences before agreeing.

You can verify consumer protections through SEBI Investor Awareness.

5. When should someone seek credit counseling?

Honestly?

Much earlier than most people do.

The best time is NOT after default.

The best time is when:

EMIs exceed 40–50% income

minimum due cycles begin

emergency savings disappear

stress starts affecting sleep

borrowing becomes routine

The earlier someone understands How Credit Counseling Works, the easier recovery becomes.

Waiting too long allows compounding interest to become financially violent.

Conclusion: The Real Truth About How Credit Counseling Works

The biggest misunderstanding about How Credit Counseling Works is believing it’s a shortcut.

It’s not.

Credit counseling is not:

- magic

- debt deletion

- instant freedom

- financial hacking

It’s structured financial honesty.

That’s what makes it powerful.

For many Indian middle-class families, the real breakthrough is not reducing debt.

The real breakthrough is finally facing the numbers honestly for the first time.

That moment changes everything.

The counselor becomes:

- part teacher

- part accountability partner

- part financial mirror

But none of it works unless behavior changes permanently.

A ₹1 lakh salary with discipline can create wealth.

A ₹3 lakh salary with denial can create disaster.

That’s the brutal math modern India is learning the hard way.

If you’re already struggling:

- stop hiding

- stop emotional borrowing

- stop minimum-due dependency

- stop pretending next month will magically fix everything

Face the numbers early.

The earlier you understand How Credit Counseling Works, the more options you still have.

Disclaimer: This article is for educational and informational purposes only and should not be treated as personalized financial, legal, or tax advice. Financial situations differ based on income, liabilities, credit profile, and lender terms. Consult certified professionals or authorized financial counsellors before making major borrowing, restructuring, or settlement decisions.