How To Negotiate Credit Card Debt in India Without Destroying Your CIBIL Score

Introduction

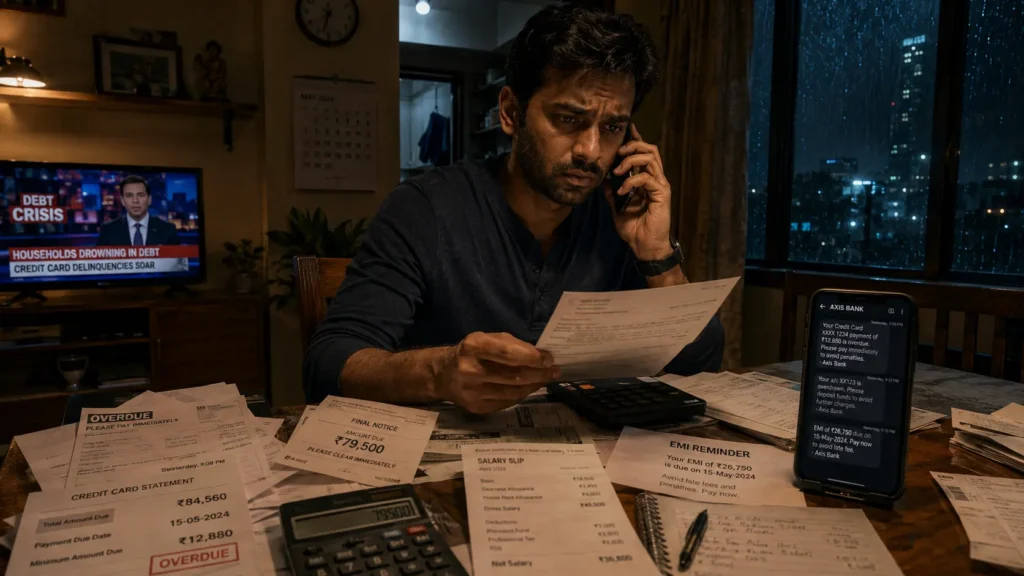

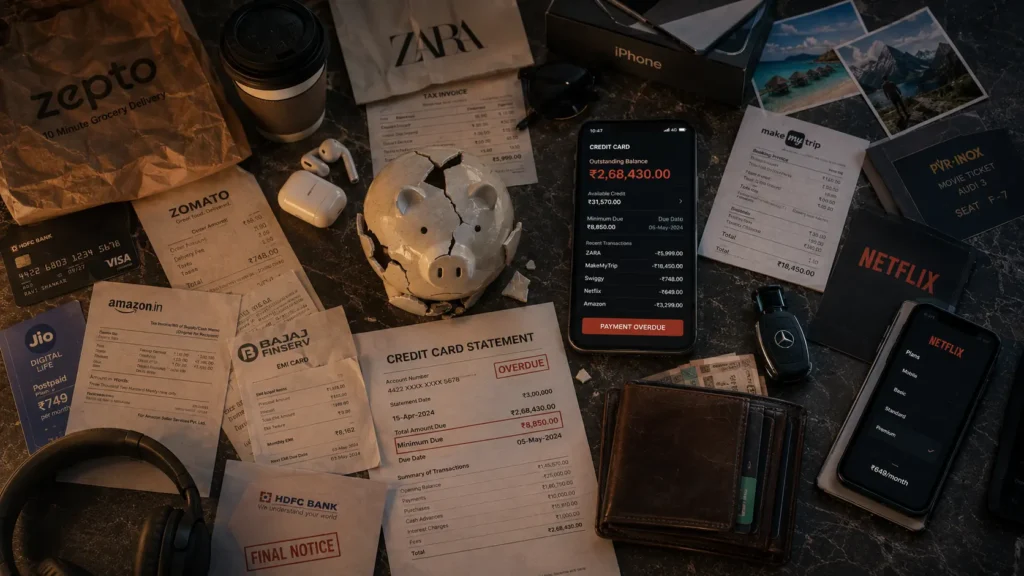

If you are searching for how to negotiate credit card debt in India, chances are the pressure has already started building.

Collection calls. Rising interest. Sleepless nights.

And here’s the reality most banks won’t openly tell you:

If you don’t learn how to negotiate credit card debt early, your outstanding amount can spiral out of control faster than you expect.

Thousands of Indians keep paying only minimum dues every month without understanding how dangerous revolving credit card interest really is.

That Rs. 1.2 lakh balance can quietly become Rs. 2 lakh.

The good news?

Learning how to negotiate credit card debt properly can reduce interest burden, stop financial stress, and help you regain control before things become legally messy.

But negotiation done the wrong way can destroy your CIBIL score for years.

This guide explains exactly how to negotiate credit card debt in India, how banks think, what RBI rules say, what settlement really means, and how to protect yourself while getting relief.

Key Takeaways

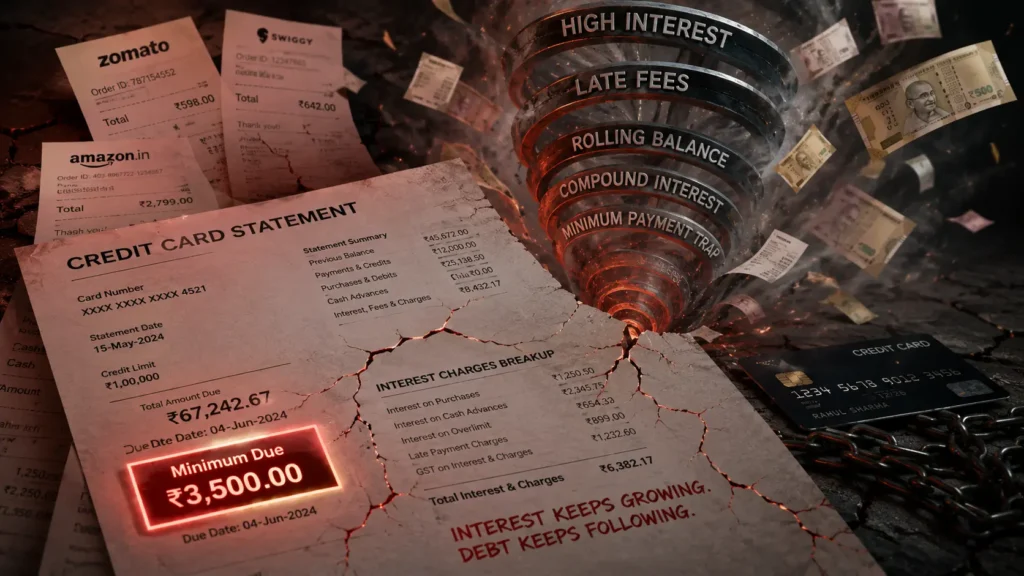

- Credit card interest in India can cross 36% annually.

- Banks are often willing to negotiate if you act early.

- Settlement hurts your CIBIL score more than structured repayment.

- RBI rules protect borrowers from harassment.

- A lump-sum offer usually works better than emotional pleading.

- Ignoring calls makes the situation worse.

- Negotiating smartly can save lakhs in interest.

Why Credit Card Debt Becomes Dangerous

Credit cards are marketed like rewards machines.

Free lounge access. Cashback. Instant discounts. EMI conversion.

But the moment you fail to pay the full bill, the game changes completely.

Most Indian credit cards charge between 30% and 42% annualized interest. That is worse than many personal loans.

Let’s make this real.

Rs. Calculation Example

Suppose Ravi from Hyderabad has:

- Credit card debt: Rs. 2,00,000

- Interest rate: 3.5% monthly

- Minimum due paid monthly: Rs. 10,000

Looks manageable?

Not really.

At 3.5% monthly interest:

A=P(1+nr)nt

PV

r(%)

n24681012141618205001000150020002500$2,653.306.7, 1385.5

Ravi could end up paying more than Rs. 3.3 lakh over time if he keeps revolving debt instead of aggressively clearing it.

That bike EMI and weekend Zomato orders suddenly become very expensive decisions.

And this is exactly why learning how to negotiate credit card debt matters before the situation explodes.

How To Negotiate Credit Card Debt With Indian Banks

Yes.

Banks negotiate all the time.

Why?

Because recovering some money is better than recovering nothing.

When borrowers stop paying for several months, banks classify accounts as stressed assets. Recovery becomes costly and uncertain.

So banks may offer:

- Reduced lump-sum settlement

- Interest waiver

- EMI restructuring

- Lower repayment plans

- Temporary hardship programs

But here’s the catch.

Banks help people who communicate early.

If you disappear for 8 months and ignore every call, your leverage drops sharply.

Best Time to Negotiate With Banks

Timing matters more than people think.

The best time to negotiate credit card debt is:

1. After Financial Hardship Starts

Examples:

- Job loss

- Salary cut

- Medical emergency

- Business slowdown

Banks respond better when hardship is genuine and documented.

2. Before Legal Escalation

If recovery agents and legal notices have already started, options become narrower.

3. When You Can Offer Lump Sum

A bank is more likely to accept:

- Rs. 80,000 today

instead of:

- Rs. 1.5 lakh uncertain over 3 years

Liquidity talks.

Emotion doesn’t.

Step-by-Step Process for how to Negotiate Credit Card Debt

Step 1: Know Your Exact Numbers

Before talking to the bank, collect:

- Total outstanding amount

- Interest charges

- Late fees

- Minimum due

- Months overdue

Never negotiate blindly.

Priya from Bengaluru thought she owed Rs. 95,000. After reviewing statements carefully, she realized nearly Rs. 28,000 was only interest and penalties.

That changed the conversation completely.

Step 2: Decide Your Goal

Are you trying to:

- Reduce interest?

- Get more time?

- Settle completely?

- Avoid legal action?

- Protect CIBIL score?

Different goals require different negotiation strategies.

Step 3: Call the Hardship or Settlement Team

Do not scream at customer care.

That accomplishes nothing.

Ask politely for:

- Retention team

- Hardship department

- Settlement desk

Be factual.

Not emotional drama.

Example Script

“I’ve had a genuine financial setback and I want to resolve this responsibly. I cannot manage the current payment structure. Can we discuss a restructuring or settlement option?”

Simple. Calm. Professional.

Step 4: Start Lower Than Your Actual Budget

If you can afford Rs. 90,000 settlement:

Do not start at Rs. 90,000.

Start lower.

Banks negotiate expecting counteroffers.

Step 5: Get Everything in Writing

This is critical.

Never trust verbal promises from collection agents.

Before paying anything, ask for:

- Settlement letter

- Final closure amount

- Payment deadline

- Written confirmation

Without documentation, future disputes can happen.+

Debt Settlement vs Restructuring

Many Indians confuse these two.

Big mistake.

Debt Settlement

You pay less than total outstanding.

Example:

- Total due: Rs. 2 lakh

- Settlement: Rs. 1.1 lakh

Sounds good initially.

But the account may be marked “Settled” instead of “Closed” in your credit report.

That hurts your CIBIL score.

Debt Restructuring

The bank modifies repayment terms.

Examples:

- Lower EMI

- Longer tenure

- Reduced interest

This is usually better for long-term credit health.

If possible, restructuring is safer than settlement.

Some Indian Scenarios

Scenario 1: Salary Cut Trap

Mahesh from Pune earned Rs. 75,000 monthly.

Then his company reduced salaries during layoffs.

He kept paying minimum dues on 3 credit cards while maintaining the same lifestyle.

Swiggy. iPhone EMI. Goa trips.

Within 14 months:

- Total debt: Rs. 4.8 lakh

- Monthly interest alone: nearly Rs. 14,000

After negotiating, he converted dues into a structured EMI at lower interest.

But he admitted the real issue wasn’t income.

It was denial.

Scenario 2: Medical Emergency

Aarti from Chennai used credit cards during her father’s hospitalization.

Debt rose to Rs. 2.3 lakh.

She immediately informed the bank, submitted medical documents, and requested hardship support.

Result:

- Interest partially waived

- EMI tenure extended

- Recovery pressure reduced

Early communication saved her from default escalation.

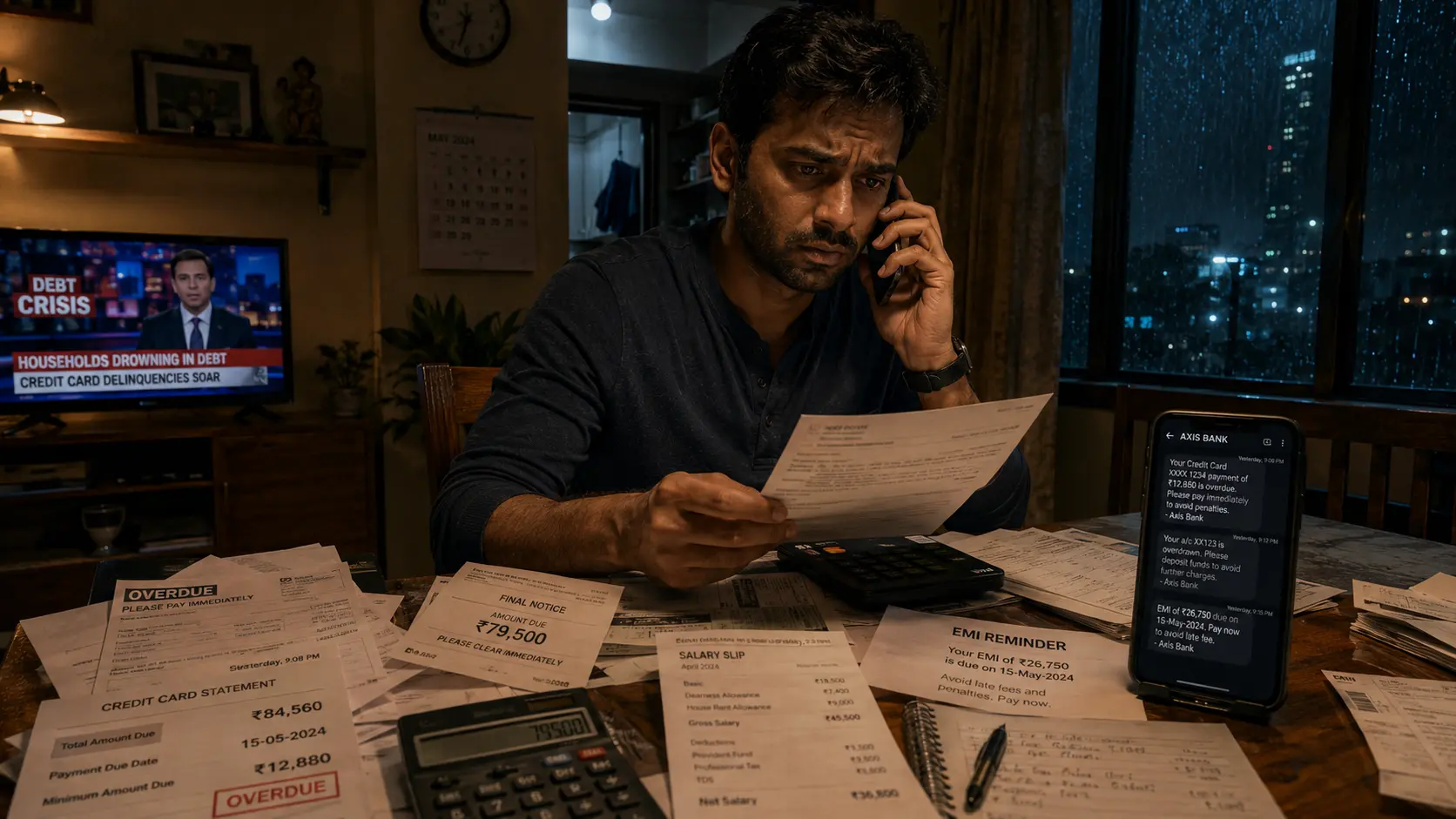

Scenario 3: Ignoring Calls Made Things Worse

Rohit from Delhi stopped answering collection calls for 7 months.

By then:

- Penalties exploded

- Legal notices started

- CIBIL damage became severe

Eventually he settled, but his credit profile suffered heavily.

Silence is expensive.

Common Mistakes People Make While Learning How To Negotiate Credit Card Debt

Paying Only Minimum Due Forever

This is the biggest trap in Indian personal finance.

Minimum due is designed to keep you in debt longer.

Not free you.

Taking New Loans to Hide Old Debt

Many people use:

- Buy Now Pay Later

- Personal loans

- New credit cards

to hide old debt temporarily.

That’s financial musical chairs.

Eventually the music stops.

Lying to Banks

Banks can often verify:

- Salary credits

- Existing loans

- Credit activity

Fake stories damage credibility.

Continuing Luxury Spending

If your Instagram shows Bali vacations while asking banks for hardship relief, don’t expect sympathy.

Banks notice spending patterns.

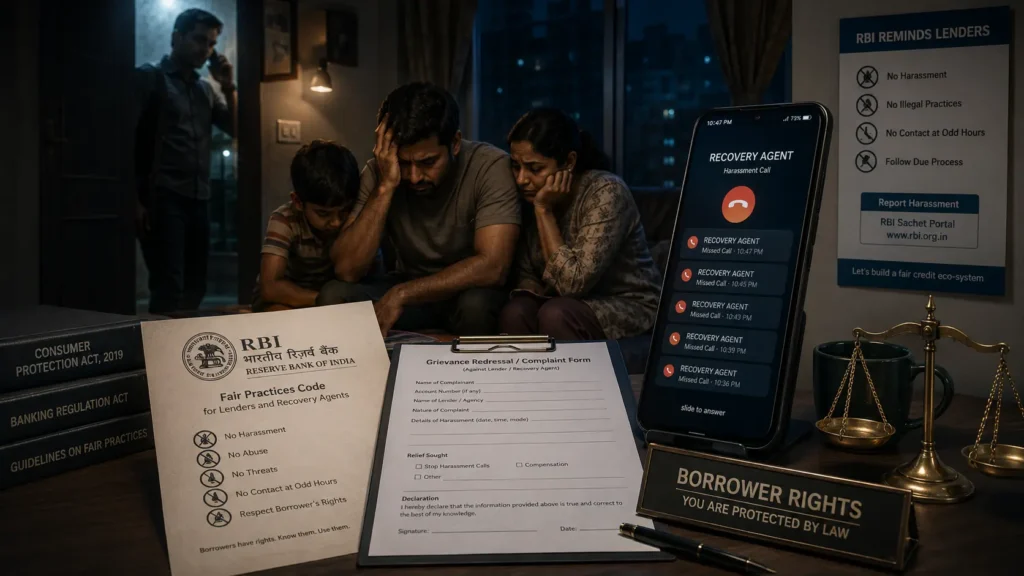

What RBI Rules Say About Recovery Agents

The Reserve Bank of India has guidelines against harassment by recovery agents.

Recovery agents cannot:

- Threaten borrowers

- Abuse family members

- Call excessively at odd hours

- Publicly shame borrowers

If harassment happens, you can complain to:

Knowing your rights matters.

But remember:

Rights do not erase debt.

You still need a repayment strategy.

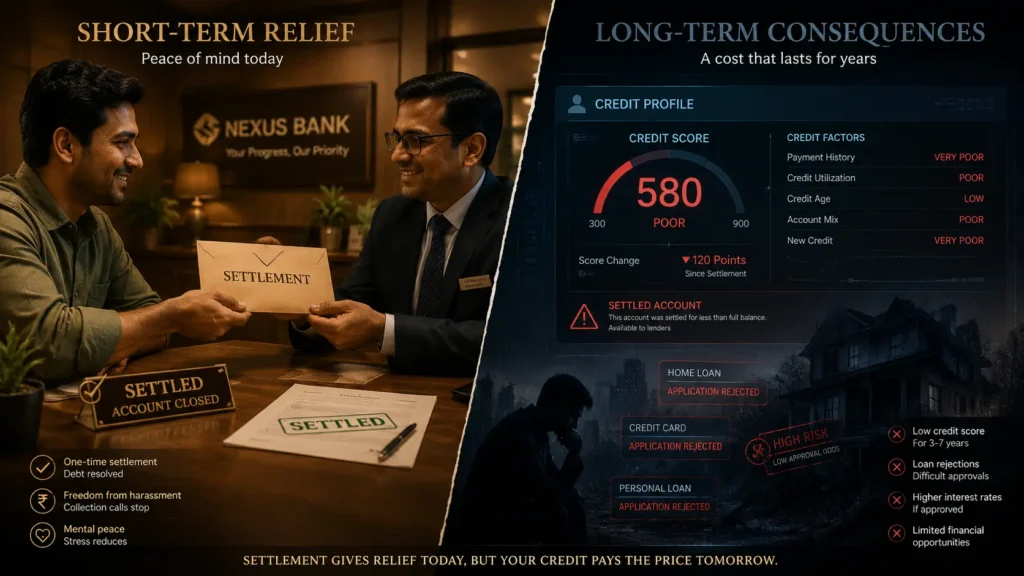

How Debt Settlement Affects CIBIL Score

This is where many people regret rushing into settlements.

If your account status becomes:

- “Settled”

instead of: - “Closed”

future lenders may see you as risky.

Possible consequences:

- Personal loan rejection

- Higher interest rates

- Lower credit card limits

- Difficulty getting home loans

Before vs After Example

Before Settlement

- CIBIL Score: 780

- Easy loan approvals

- Better credit card offers

After Poorly Managed Settlement

- CIBIL Score: 610

- Loan rejection risk

- Higher borrowing costs

A short-term escape can become a long-term penalty.

Alternatives to Credit Card Settlement

Sometimes negotiation is not the best solution.

Consider:

Personal Loan Balance Transfer

Lower interest than revolving credit cards.

Debt Snowball Method

Pay smallest debts first for momentum.

Read to Know more about Debt Snowball Method and how its work.

Debt Avalanche Method

Pay highest-interest debt first.

This mathematically saves more money.

Read to Know more about Debt Avalanche Method and how its work.

Expense Surgery

Not budgeting.

Surgery.

If you earn Rs. 55,000 and spend:

- Rs. 7,000 on food delivery

- Rs. 4,500 on subscriptions

- Rs. 9,000 on shopping EMIs

then debt is not only an income problem.

It’s a behavior problem.

That truth hurts.

But it also fixes things faster.

Frequently Asked Questions

How To Negotiate Credit Card Debt Without Hurting CIBIL Score?

The best way to handle how to negotiate credit card debt without severe CIBIL damage is to prioritize restructuring over settlement whenever possible.

Will settling credit card debt hurt my CIBIL score?

Yes, settlement can negatively impact your CIBIL score if the account is marked as “Settled” instead of “Closed.”

What is the best way to negotiate credit card debt?

The best approach is:

Know your outstanding amount

Offer realistic repayment

Stay professional

Request written confirmation

That’s the safest way to negotiate credit card debt

Can banks waive credit card interest?

Sometimes. Especially during hardship situations involving job loss, medical emergencies, or prolonged financial stress.

Should I use a personal loan to clear credit card debt?

In some cases, yes.

A lower-interest personal loan can reduce overall interest burden compared to revolving credit card debt.

But only if spending habits change too.

How long does debt settlement stay on CIBIL report?

Typically, settlement history may remain visible for several years and affect future loan approvals.

Is Hiring Agencies for How To Negotiate Credit Card Debt Worth It?

Some agencies help borrowers negotiate settlements, but many charge high fees. Always compare costs before outsourcing how to negotiate credit card debt.

Conclusion

Learning how to negotiate credit card debt is not about escaping responsibility.

It is about preventing financial collapse before interest and penalties take complete control of your income.

The earlier you understand how to negotiate credit card debt, the stronger your negotiating power usually becomes.

Ignore the problem, and banks gain leverage.

Act early, communicate professionally, and focus on fixing the spending habits that created the debt in the first place.

Because the real goal of learning how to negotiate credit card debt is not just settling dues.

It is rebuilding financial stability permanently.

Talk to the bank early.

Negotiate calmly.

Protect your CIBIL score wherever possible.

And most importantly — fix the behavior that created the debt in the first place.

Because no settlement letter can solve a spending addiction.

Disclaimer: This article is for educational purposes only and should not be considered legal or financial advice. Credit policies, settlement terms, and RBI regulations may change over time. Consult a qualified financial advisor or legal professional before making major debt decisions.

Author Bio

Mahesh Reddy is the founder and lead financial educator at InvestingLens.com. He writes practical, India-first personal finance content focused on debt management, investing psychology, budgeting, and wealth building for middle-class Indians. His writing combines behavioral finance with real-world money mistakes people actually make.