9 Brutal Truths About How To Pay Off Debt Faster in India. Your salary comes in.

Three days later, anxiety comes back.

One EMI gets deducted. Then another. Credit card notifications start flashing. UPI spending quietly drains the rest. By the 20th of the month, you’re calculating whether you can survive until payday without touching another loan app.

This is the part nobody talks about openly.

Many Indian families look financially stable from outside while silently drowning in debt.

A decent salary no longer guarantees peace.

And the most painful part?

Most people are not trapped because they are irresponsible. They’re trapped because modern life became expensive faster than their income grew.

Rent increased. Fuel prices increased. School fees increased. Medical costs exploded. Meanwhile, easy EMIs made everything feel “affordable.”

Until it wasn’t.

If you want to know how to pay off debt faster, the answer is not another motivational quote. You need a practical system that works in real Indian life — with real salaries, real family pressure, and real financial stress.

This guide breaks down exactly how Indians can escape debt faster without destroying their mental health in the process.

Key Takeaways

- Credit card debt is usually the most dangerous debt in India

- Paying only minimum due keeps people financially trapped for years

- The debt avalanche method saves the most money long term

- Small UPI and lifestyle leaks quietly slow debt repayment

- Temporary income boosts can dramatically speed up debt freedom

- Most Indians underestimate how much interest they are actually paying

- Emotional spending is one of the biggest hidden debt triggers

- Debt freedom starts with cash-flow control, not income alone

Why Most Indians Stay Stuck in Debt Longer Than Necessary

The problem is rarely just math.

It’s emotional exhaustion.

Rahul, a 31-year-old IT employee in Hyderabad, earned Rs. 84,000 monthly. On paper, he looked financially stable.

But reality looked different:

- Rent: Rs. 24,000

- Bike EMI: Rs. 5,200

- Credit card dues: Rs. 14,000

- Parents support: Rs. 12,000

- Food delivery + random UPI spending: Rs. 9,000+

- Fuel and groceries: constantly increasing

By month-end, he had almost nothing left.

Then one medical emergency pushed him into revolving credit card debt at nearly 40% annual interest.

That’s how debt traps begin in India now. Quietly.

Nobody teaches money management in school. Then society judges you for struggling with it later.

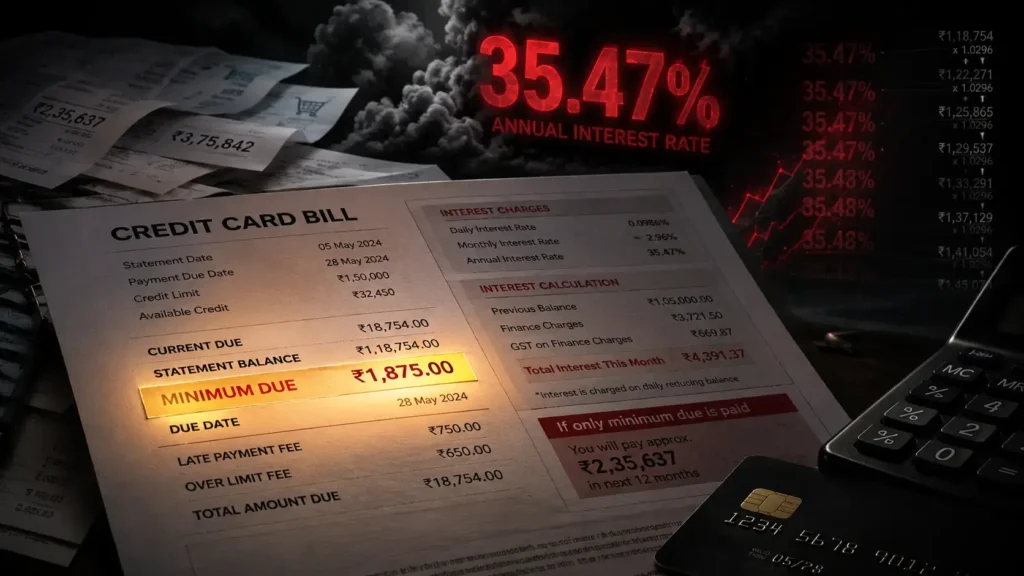

1. Stop Paying Only the Minimum Due

This is one of the biggest financial traps in India.

Banks market minimum dues like a safety option. In reality, minimum payments often keep people trapped in expensive debt cycles for years.

If your outstanding credit card balance is Rs. 1 lakh and you keep paying only the minimum amount, interest keeps compounding aggressively.

And Indian credit cards are not cheap.

Many cards charge 30%–45% annualized interest after the interest-free period ends.

That is brutally expensive debt.

Example

| Credit Card Balance | Interest Rate | Minimum Due | Real Financial Damage |

|---|---|---|---|

| Rs. 1,00,000 | 42% annually | Rs. 5,000 | Debt keeps growing silently |

Most people don’t realize how dangerous this becomes because the monthly payment initially feels “manageable.”

That illusion destroys financial progress.

What To Do Instead

- Always pay more than minimum due

- Pause unnecessary credit card usage temporarily

- Redirect every extra rupee toward high-interest debt first

According to the Reserve Bank of India (RBI), revolving credit balances can significantly increase repayment burden if users only clear minimum dues regularly.

2. Use the Debt Avalanche Method to Pay off Debt Faster

If your goal is to pay off debt faster mathematically, the debt avalanche method is usually the smartest strategy.

How It Works

You:

- Continue minimum payments on all loans

- Put every extra rupee toward the highest-interest debt first

Once that debt disappears, move aggressively to the next highest-interest loan.

Example

| Debt Type | Interest Rate |

|---|---|

| Credit Card | 42% |

| Personal Loan | 17% |

| Bike Loan | 10% |

The credit card gets attacked first.

Always.

Because high-interest debt quietly eats your future income every month.

Why This Method Works

It minimizes total interest paid over time.

Which means:

- Faster debt freedom

- Lower financial stress

- More cash-flow recovery

And honestly… when interest stops bleeding your salary every month, life starts feeling lighter again.

Explore Debt Settlement vs Debt Consolidation: Which is Better for You in 2026?

3. Track Every Rupee for 30 Days

Most people don’t actually know where their money disappears.

They assume.

That assumption is expensive.

A Bangalore startup employee once tracked his spending for one month and discovered:

- Swiggy/Zomato: Rs. 5,800

- Random Amazon purchases: Rs. 4,200

- Weekend café spending: Rs. 3,100

- Subscription apps: Rs. 1,700

That’s nearly Rs. 15,000 monthly.

Enough to dramatically accelerate debt repayment.

The Real Problem

Modern spending feels invisible now.

UPI made spending frictionless.

Tiny payments don’t feel dangerous individually. But collectively, they quietly delay financial recovery by years.

Your 30-Day Debt Reset Challenge

For the next month:

- No impulse shopping

- No unnecessary food delivery

- No gadget upgrades

- No “small reward” spending

- Track every UPI transaction

You don’t need perfection.

You need awareness.

That alone changes behavior.

4. Increase Income Temporarily – Aggressively

Sometimes budgeting alone is not enough.

Especially when debt interest is growing faster than your repayment speed.

In those situations, income expansion becomes necessary.

Not forever. Temporarily.

Practical Side Income Ideas in India

- Freelancing

- Tuition classes

- Weekend consulting

- Content writing

- Graphic design

- Video editing

- Selling digital services

- Driving weekends

- Reselling unused items online

A Pune software employee earning Rs. 92,000 monthly started weekend freelance development work and used the extra Rs. 22,000 entirely toward debt repayment.

He cleared nearly Rs. 3 lakh debt over a year earlier than planned.

That one decision changed his entire financial future.

5. Stop Trying To “Look Rich”

This is uncomfortable. But important.

Many Indians stay trapped in debt because they are financially performing for society.

- Expensive phones on EMI

- Luxury weddings

- Brand pressure

- Lifestyle inflation

- Fancy restaurants

- “Everyone else is doing it” spending

The salary increased. The stress increased too.

Because expenses expanded faster than income.

The Hard Truth

Nobody outside your home pays your EMIs for you.

Not relatives.

Not Instagram.

Not colleagues.

Temporary social validation creates long-term financial pressure.

And deep down, most people already know this.

6. Try the Debt Snowball Method if Motivation Is Your Problem

Some people quit debt repayment because progress feels invisible.

That’s where the debt snowball method helps psychologically.

How It Works

Instead of attacking the highest-interest debt first, you clear the smallest debt first.

That quick win creates emotional momentum.

Example

| Debt | Amount |

|---|---|

| BNPL App | Rs. 6,500 |

| Credit Card | Rs. 1.2 lakh |

| Personal Loan | Rs. 3 lakh |

Clearing the smallest debt first feels satisfying.

And motivation matters more than spreadsheets sometimes.

Especially when you’re mentally exhausted.

Explore Debt Settlement vs Debt Consolidation: Which is Better for You in 2026?

7. Sell Unused Assets Immediately

Most households are sitting on unused money.

Old phones.

Unused electronics.

Extra furniture.

Unused gold.

Old bikes.

Gaming consoles.

These items quietly lose value every year.

Selling them and reducing principal debt immediately saves future interest too.

Important Rule

Use the money ONLY for debt reduction.

Not celebration spending.

Not vacations.

Not “just one reward purchase.”

That discipline separates temporary relief from real recovery.

8. Negotiate With Banks

Many people never even ask.

But banks sometimes reduce:

- Interest rates

- EMI burden

- Late fees

- Settlement structures

Especially if:

- Your salary improved

- Your CIBIL score improved

- You became lower-risk financially

Always compare loan restructuring or balance transfer options directly through official bank portals before making decisions. State Bank of India provides publicly available loan restructuring information and borrower guidelines.

9. Automate Every EMI Possible

Debt becomes dangerous when repayments become inconsistent.

Missed payments trigger:

- Late fees

- Penalty interest

- CIBIL score damage

- Collection calls

- Mental stress

Automation reduces those risks significantly.

Best Automation Options

- Auto-debit

- Standing instructions

- Salary-account EMI deduction

- Credit card auto-pay

The less emotional decision-making involved, the safer your financial system becomes.

The Emotional Side of Debt Nobody Talks About

Debt changes behavior.

People stop checking bank accounts.

Avoid unknown calls.

Feel guilty spending money.

Lose sleep before EMI dates.

Financial anxiety is exhausting because it follows you everywhere — even while resting.

And many middle-class Indian families silently carry this pressure for years.

That’s why debt repayment is not just financial recovery.

It’s emotional recovery too.

Simple Debt Payoff Plan

Step 1 – List Every Debt

Write:

- Outstanding balance

- EMI

- Interest rate

- Remaining tenure

Step 2 – Choose Your Method

- Avalanche = saves more money

- Snowball = builds motivation faster

Step 3 – Cut Spending Leaks

Track:

- Food delivery

- Shopping

- UPI spending

- Subscriptions

Step 4 – Increase Income

Temporary side income can massively accelerate debt freedom.

Step 5 – Stop Taking New EMIs

This step alone changes everything.

Debt Payoff Example

| Monthly Salary | Rs. 80,000 |

|---|---|

| Essential Expenses | Rs. 42,000 |

| Existing EMIs | Rs. 18,000 |

| Extra Debt Payment | Rs. 15,000 |

| Emergency Savings | Rs. 5,000 |

Adding Rs. 15,000 extra monthly toward high-interest debt can reduce repayment timelines dramatically.

Quick Debt Recovery Checklist

Stop minimum-only payments

Attack highest-interest debt first

Track all UPI spending

Pause unnecessary shopping

Reduce food delivery spending

Build temporary side income

Automate EMIs

Avoid taking fresh loans

Sell unused assets

Monitor your CIBIL score regularly

FAQ – How To Pay Off Debt Faster

What is the fastest way to pay off debt faster in India?

The fastest way to pay off debt faster is combining aggressive repayments with reduced lifestyle spending and temporary income growth while prioritizing high-interest debt first.

Should I close my credit cards?

Not necessarily. But you should stop unnecessary spending while aggressively clearing balances.

Which method is better — avalanche or snowball?

Debt avalanche saves more money mathematically. Debt snowball helps psychologically. Both work if you stay consistent.

Is debt consolidation safe?

It can help reduce interest burden if used carefully. But it only works if spending habits improve too.

How much of salary should go toward EMIs?

Ideally, total EMIs should stay below 35%–40% of monthly income whenever possible.

Final Thoughts

Debt freedom rarely happens overnight.

It usually happens through small painful decisions repeated consistently.

Skipping one unnecessary purchase.

Making one extra payment.

Saying no to one unnecessary EMI.

Tracking spending honestly for the first time.

That’s how recovery begins.

Tonight, before sleeping, check every EMI leaving your bank account. Most people discover the real financial leak right there.

Because the truth is simple:

You do not build wealth while carrying uncontrolled high-interest debt.

You build peace first.

Then wealth becomes possible.

Money stress feels unbearable when you’re carrying it silently. But financial recovery starts the moment you stop pretending everything is fine and start taking control again.

Last verified against official RBI and Indian banking sources: May 2026

Loan Disclaimer: Interest rates, processing fees, and loan terms vary by lender and applicant profile. Verify directly with banks before applying.