National Household Debt Statistics: A Deep Dive Into Global Debt Trends and What They Mean for Indian Families

Introduction

National Household Debt Statistics tell a story far bigger than numbers on a spreadsheet. National Household Debt Statistics reveal how families borrow, spend, survive economic shocks, and build wealth across different countries.

If you want the short answer first, here it is: household debt is rising worldwide, but not all debt is dangerous. The real issue is whether income grows faster than liabilities.

A family in Bengaluru with a ₹70 lakh home loan and rising salary may be financially healthier than a family in another country carrying high-interest credit card balances despite earning more money. That’s why understanding National Household Debt Statistics matters.

Across developed economies, household debt often exceeds annual income. In India, debt levels remain lower than many advanced economies, but consumer credit growth has accelerated rapidly over the last decade. This shift has major implications for middle-class households, financial institutions, policymakers, and investors.

For readers of InvestingLens, National Household Debt Statistics are not just macroeconomic indicators. They are early warning signals that can affect:

- Home loan affordability

- Credit card interest costs

- Personal loan approvals

- CIBIL scores

- Consumer spending

- Long-term wealth creation

External Resources

Internal Resources

Key Takeaways Box

✅ National Household Debt Statistics show debt is increasing globally.

✅ India’s household debt remains lower than many developed countries but is growing rapidly.

✅ Housing loans account for the largest share of household debt worldwide.

✅ Credit card debt creates the greatest risk due to extremely high interest rates.

✅ Debt becomes dangerous when income growth cannot keep pace with repayment obligations.

✅ Countries with high debt levels are more vulnerable during economic slowdowns.

✅ Indian families should monitor debt-to-income ratios instead of focusing only on EMI affordability.

What National Household Debt Statistics Actually Measure and Why Investors Should Care

Understanding National Household Debt Statistics starts with understanding what economists mean by “household debt.”

Most people assume debt means loans. Technically that’s correct, but National Household Debt Statistics include several categories:

- Home loans

- Personal loans

- Vehicle loans

- Education loans

- Credit card balances

- Consumer financing obligations

Every quarter, central banks and international organizations track these liabilities because they provide insights into future economic activity.

Think about it this way.

If millions of households suddenly reduce borrowing, spending usually falls shortly afterward.

If millions of households aggressively increase borrowing, spending tends to rise.

That’s why National Household Debt Statistics are often leading indicators for economic growth.

The Theory

Economists frequently compare household debt against GDP.

This metric shows whether borrowing is growing faster than the economy itself.

Countries with high household debt ratios often experience:

- Strong housing markets

- Higher consumer spending

- Greater economic sensitivity to interest rates

Countries with lower household debt ratios often have:

- More conservative borrowing cultures

- Lower financial risk

- Less exposure to housing bubbles

However, low debt is not automatically positive.

Debt often finances productive assets.

A family borrowing ₹80 lakh for a home that appreciates over twenty years may create substantial wealth.

A family borrowing ₹5 lakh on credit cards at 36% annual interest may destroy wealth.

The distinction matters enormously when analyzing National Household Debt Statistics.

The Indian Reality

Meet Rahul.

Rahul is a 35-year-old software engineer in Bengaluru earning ₹18 lakh annually.

In 2018, Rahul had:

| Item | Amount |

|---|---|

| Home Loan | ₹45 lakh |

| Car Loan | ₹6 lakh |

| Credit Card Debt | ₹0 |

| Total Debt | ₹51 lakh |

By 2026:

| Item | Amount |

| Home Loan | ₹39 lakh |

| Car Loan | ₹0 |

| Credit Card Debt | ₹20,000 |

| Total Debt | ₹39.2 lakh |

His debt actually fell despite rising asset ownership.

Now compare that with another household.

Ankit earns ₹15 lakh annually.

He carries:

| Item | Amount |

| Personal Loan | ₹8 lakh |

| Credit Card Debt | ₹4 lakh |

| Consumer Finance | ₹2 lakh |

| Total Debt | ₹14 lakh |

Despite having lower absolute debt, Ankit faces significantly greater financial stress because his borrowing costs are much higher.

This is exactly why National Household Debt Statistics require deeper interpretation than headline numbers.

IL Advisor Warning

Many Indians proudly say:

“I only pay the minimum due.”

That sentence has probably destroyed more wealth than stock market crashes.

A ₹50,000 credit card balance at roughly 36% annual interest can grow into a devastating long-term burden if repayment is delayed.

The danger isn’t borrowing.

The danger is expensive borrowing.

Global Comparison of Household Debt

The following illustration converts approximate household debt burdens into Indian Rupee equivalents for easier understanding.

| Country | Debt-to-GDP Trend | General Risk Level |

| Switzerland | Very High | Moderate |

| Australia | Very High | Moderate |

| Canada | High | Moderate |

| United States | High | Moderate |

| South Korea | High | Elevated |

| China | Rising | Elevated |

| India | Lower but Growing | Emerging Risk |

National Household Debt Statistics show that India still sits below many advanced economies, but growth rates deserve attention.

Hard Math

Suppose a household earns ₹12 lakh annually.

Financial planners often monitor debt-to-income ratios.

| Debt Level | Ratio |

| ₹6 lakh | 50% |

| ₹12 lakh | 100% |

| ₹24 lakh | 200% |

| ₹36 lakh | 300% |

The higher the ratio, the greater the vulnerability to:

- Job loss

- Medical emergencies

- Interest-rate increases

- Economic slowdowns

This relationship sits at the core of modern National Household Debt Statistics analysis.

Additional Reading

External Sources:

- Reserve Bank of India Financial Stability Reports

- Bank for International Settlements Household Credit Data

Internal Resources:

How National Household Debt Statistics Reveal Financial Risks Before They Become Crises

When economists worry about recessions, banking stress, or consumer spending slowdowns, they often look at National Household Debt Statistics before anything else.

Why?

Because households drive a massive portion of economic activity.

A government can spend more money.

Companies can invest more capital.

But if households stop spending because debt repayments consume too much income, economic growth can slow quickly.

This is why central banks worldwide closely monitor National Household Debt Statistics.

For Indian investors, understanding these numbers is becoming increasingly important because India’s household credit market has expanded dramatically over the last decade.

National Household Debt Statistics and the Global Debt Explosion

One of the biggest misconceptions about debt is that it suddenly becomes a problem.

It rarely does.

Most debt crises build quietly for years.

The pattern usually looks like this:

- Easy credit becomes available.

- Consumers borrow more.

- Asset prices rise.

- Confidence increases.

- Borrowing accelerates.

- Interest rates rise.

- Repayment stress appears.

- Defaults increase.

- Economic slowdown follows.

This cycle has repeated itself across countries and decades.

The United States experienced it before the 2008 financial crisis.

Several European countries experienced similar debt-driven stress after the Global Financial Crisis.

China’s rapid expansion in household borrowing has attracted increasing scrutiny from economists.

Even India is seeing signs that consumer borrowing is becoming a larger part of household financial behaviour.

That doesn’t mean a crisis is imminent.

It simply means National Household Debt Statistics deserve attention.

The Theory

Economists generally evaluate National Household Debt Statistics using four key metrics:

1. Debt-to-GDP Ratio

Measures total household debt relative to economic output.

Higher ratios suggest households rely heavily on borrowing.

2. Debt-to-Income Ratio

Measures how much households owe compared to annual income.

This often provides a clearer picture than debt alone.

3. Debt Service Ratio

Measures the percentage of income used for loan repayments.

This is one of the most important indicators.

4. Credit Growth Rate

Measures how quickly borrowing is expanding.

Rapid credit growth often deserves closer monitoring.

A country with moderate debt but very rapid credit growth may actually face greater risk than a country with higher but stable debt levels.

That’s one of the most important lessons hidden inside National Household Debt Statistics.

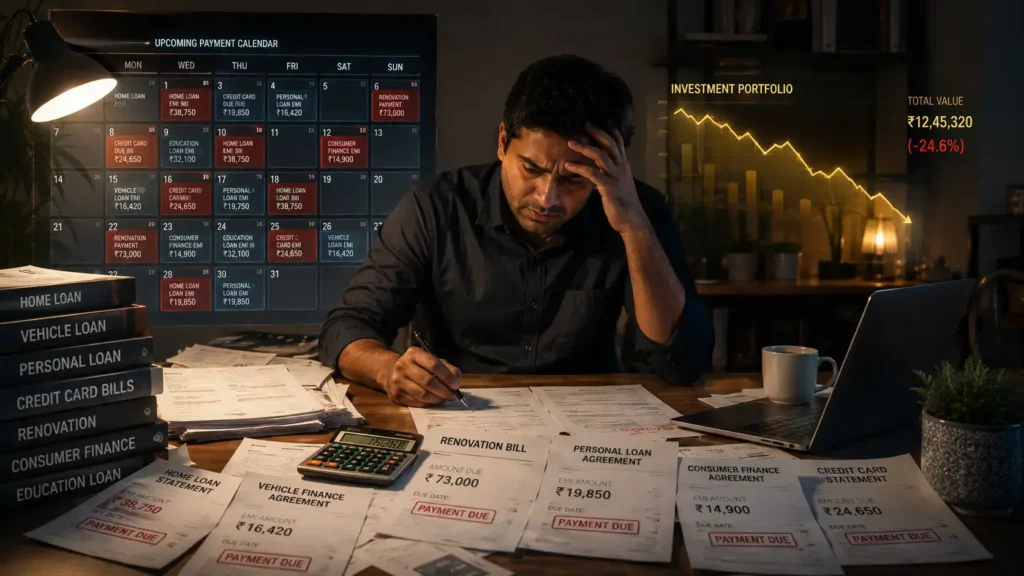

The Indian Reality: Priya’s EMI Trap

Priya works in Hyderabad.

Annual salary: ₹14 lakh.

Monthly in-hand income: approximately ₹90,000.

In 2021, her finances looked healthy.

| Category | Amount |

|---|---|

| Home Loan EMI | ₹24,000 |

| Car Loan EMI | ₹8,000 |

| Total EMI | ₹32,000 |

Debt consumed about 36% of monthly income.

Manageable.

Then things changed.

She upgraded her car.

She financed electronics.

She took a personal loan for home renovation.

Her financial picture became:

| Category | Amount |

| Home Loan EMI | ₹24,000 |

| Car Loan EMI | ₹14,000 |

| Personal Loan EMI | ₹11,000 |

| Consumer Finance EMI | ₹5,000 |

| Total EMI | ₹54,000 |

Monthly income remained ₹90,000.

Debt obligations now consumed 60% of take-home pay.

Nothing catastrophic happened.

No job loss.

No emergency.

Yet stress increased dramatically.

That’s how debt problems usually emerge.

Not through one huge mistake.

Through multiple small decisions.

Millions of households making similar decisions eventually influence National Household Debt Statistics.

IL Advisor: The EMI Illusion

Here’s a mistake I see repeatedly.

People ask:

“Can I afford the EMI?”

The better question is:

“Can I still build wealth after paying the EMI?”

Those are completely different questions.

A bank may approve a loan.

That doesn’t automatically mean the loan improves your financial future.

Consider two individuals earning ₹1 lakh monthly.

Household A

| Category | Amount |

| Total EMI | ₹25,000 |

| Savings | ₹25,000 |

| Investments | ₹20,000 |

| Lifestyle Spending | ₹30,000 |

Household B

| Category | Amount |

| Total EMI | ₹65,000 |

| Savings | ₹5,000 |

| Investments | ₹0 |

| Lifestyle Spending | ₹30,000 |

Both can technically pay EMIs.

Only one is building wealth.

This distinction rarely appears in headlines discussing National Household Debt Statistics, but it matters enormously.

Global Household Debt Comparison Through an Indian Lens

To understand the scale of borrowing globally, imagine average annual household income represented in Indian Rupees.

| Economy | General Household Debt Characteristics |

| United States | High mortgage and credit card usage |

| Canada | Significant housing debt exposure |

| Australia | Very high mortgage concentration |

| South Korea | Elevated household leverage |

| China | Rapid debt growth during urbanisation |

| India | Lower debt base but growing consumer credit |

The key takeaway from National Household Debt Statistics is not which country has the highest debt.

The key question is:

Can households comfortably service that debt?

Countries with stronger incomes, stronger employment markets, and longer mortgage maturities can often sustain higher debt levels.

Countries experiencing slower income growth may struggle with lower debt burdens.

Hard Math: What Rising Interest Rates Actually Do

Suppose a household has a ₹50 lakh floating-rate home loan.

Scenario A: 8% Interest

| Item | Value |

| Loan Amount | ₹50,00,000 |

| Tenure | 20 Years |

| EMI | Approx ₹41,800 |

Scenario B: 9% Interest

| Item | Value |

| Loan Amount | ₹50,00,000 |

| Tenure | 20 Years |

| EMI | Approx ₹45,000 |

Difference:

₹3,200 per month.

₹38,400 per year.

Over several years, that additional repayment can significantly reduce savings and investments.

When millions of households experience this simultaneously, National Household Debt Statistics begin influencing economic growth, consumer spending, and financial stability.

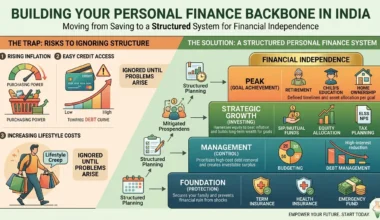

What Indian Families Should Watch Going Forward

Instead of obsessing over total debt, focus on these indicators:

✔ Debt-to-income ratio

✔ EMI-to-income ratio

✔ Credit card balances

✔ Emergency fund adequacy

✔ Interest rate exposure

✔ CIBIL score trends

The most useful lesson from National Household Debt Statistics is simple:

Debt itself isn’t the enemy.

Poorly managed debt is.

A home loan helping create long-term assets is different from rolling over high-interest credit card balances for years.

Understanding that difference is where financial resilience begins.

Further Reading

External Authority Sources

Internal InvestingLens Resources

The 9-Layer Transformation Story: How National Household Debt Statistics Became Personal for One Indian Family

Most people think National Household Debt Statistics are numbers that economists discuss on television.

Rajesh Sharma thought the same.

At age 34, Rajesh worked as a project manager in Pune earning ₹18 lakh annually. His wife Neha earned another ₹8 lakh as a school administrator. Combined income was ₹26 lakh per year.

They felt financially successful.

Yet within five years, they became a perfect example of why National Household Debt Statistics matter.

Layer 1: Status Quo

Life looked comfortable.

- ₹65 lakh home loan

- ₹7 lakh car loan

- Two credit cards

- International vacations

- EMI-funded electronics

Nothing seemed dangerous.

Their friends lived similarly.

The bank kept approving credit.

Everything felt normal.

Layer 2: Trigger

During the pandemic recovery years, property prices increased.

Friends discussed upgrading homes.

Social media amplified lifestyle pressure.

Rajesh started viewing debt differently.

Instead of seeing debt as a liability, he saw it as a shortcut to a better lifestyle.

This is often where trends inside National Household Debt Statistics begin.

Millions of households simultaneously become more comfortable borrowing.

Layer 3: Mistake

The biggest mistake wasn’t taking a home loan.

The mistake was layering debt.

First came a luxury SUV.

Then premium furniture.

Then a renovation loan.

Then vacation financing.

Individually each EMI looked manageable.

Together they became dangerous.

Monthly commitments jumped from ₹48,000 to ₹1.02 lakh.

Layer 4: Wake-Up Call

The wake-up call arrived unexpectedly.

Neha’s school reduced staff bonuses.

Rajesh’s company delayed promotions.

Income growth stalled.

Expenses did not.

For the first time, they started using credit cards to bridge monthly cash flow gaps.

That is one of the earliest warning signs hidden inside National Household Debt Statistics.

When debt begins funding consumption instead of assets, vulnerability rises.

Layer 5: IL Advisor

Here’s the uncomfortable truth.

Most debt problems are not caused by low income.

They’re caused by lifestyle inflation.

Rajesh wasn’t poor.

His household earned more than many Indian families.

Yet debt absorbed so much cash flow that wealth creation stopped.

A person earning ₹25 lakh but saving nothing is often financially weaker than someone earning ₹10 lakh and investing consistently.

That’s the brutal lesson.

Layer 6: Calculation

Let’s compare.

| Category | Before | After |

|---|---|---|

| Combined Income | ₹26 lakh | ₹26 lakh |

| Total EMI | ₹48,000 | ₹1,02,000 |

| Annual Investments | ₹4.8 lakh | ₹60,000 |

| Emergency Fund | ₹5 lakh | ₹1.5 lakh |

| Credit Card Balance | ₹0 | ₹2.8 lakh |

Investment growth suffered dramatically.

Assuming 12% annual returns:

| Annual Investment | 20-Year Value |

| ₹4.8 lakh | Approx ₹3.8 crore |

| ₹60,000 | Approx ₹47 lakh |

The difference exceeded ₹3 crore.

That wealth destruction happened without a market crash.

It happened because debt crowded out investing.

Layer 7: Pivot

Rajesh and Neha made difficult decisions.

They sold the SUV.

Cancelled expensive memberships.

Used bonuses to repay high-interest debt.

Focused on rebuilding cash reserves.

Their goal changed from appearing wealthy to becoming wealthy.

Layer 8: Result

Within three years:

- Credit card debt eliminated

- Personal loans closed

- Emergency fund restored

- SIPs increased

- Financial stress reduced

The family still had debt.

But now the debt was primarily asset-backed.

Layer 9: Lesson

The lesson isn’t “avoid all debt.”

The lesson is understanding the difference between productive debt and destructive debt.

That’s the real value of National Household Debt Statistics.

They help us understand how borrowing affects long-term financial health.

National Household Debt Statistics and the Next Decade of Global Financial Risk

The future of National Household Debt Statistics will likely be shaped by three major forces:

- Higher interest rates

- Aging populations

- Slower economic growth

These forces are already influencing household finances worldwide.

The Theory

For nearly two decades after the Global Financial Crisis, many countries experienced historically low interest rates.

Cheap borrowing encouraged:

- Housing purchases

- Consumer spending

- Asset price appreciation

As rates rise, repayment costs increase.

Households carrying excessive leverage face greater pressure.

This is why analysts carefully monitor National Household Debt Statistics during monetary tightening cycles.

A debt level that feels manageable at 5% interest may feel very different at 8%.

The Indian Reality: A Tale of Two Households

Household One: Meera and Arjun

Combined income: ₹22 lakh.

Debt profile:

| Category | Amount |

| Home Loan | ₹45 lakh |

| Credit Card Debt | ₹0 |

| Emergency Fund | ₹10 lakh |

| SIP Investment | ₹25,000/month |

Interest-rate increases affect them.

But they remain financially resilient.

Household Two: Karan and Pooja

Combined income: ₹22 lakh.

Debt profile:

| Category | Amount |

| Home Loan | ₹50 lakh |

| Personal Loan | ₹10 lakh |

| Credit Card Debt | ₹4 lakh |

| Emergency Fund | ₹50,000 |

| SIP Investment | ₹0 |

A similar income produces a very different outcome.

This distinction is central to interpreting National Household Debt Statistics.

The same amount of income does not guarantee the same financial resilience.

IL Advisor: Stop Celebrating Loan Approvals

One of the most dangerous financial myths is:

“The bank approved it, so I can afford it.”

Banks assess repayment probability.

They do not assess whether the loan helps you build wealth.

Those are different objectives.

Many households confuse access to credit with financial strength.

The result often appears years later.

Hard Math: Debt Service Stress

Assume monthly take-home income of ₹1 lakh.

| EMI Burden | Risk Level |

| ₹20,000 | Low |

| ₹35,000 | Moderate |

| ₹50,000 | Elevated |

| ₹65,000+ | High |

As EMI burdens rise:

- Savings decline

- Investments decline

- Emergency preparedness declines

Eventually, even small disruptions become serious problems.

This pattern repeatedly appears across countries whenever National Household Debt Statistics deteriorate.

What Investors Should Monitor

Over the next decade, watch:

Household Credit Growth

Rapid expansion often precedes future stress.

Housing Market Leverage

Mortgage growth drives many debt cycles.

Credit Card Balances

Often the most expensive form of household debt.

Debt Service Ratios

More important than headline debt numbers.

Wage Growth

The best antidote to rising debt burdens.

Recommended Resources

External Sources

Internal Resources

The biggest lesson from National Household Debt Statistics is surprisingly simple:

Debt isn’t automatically dangerous.

Debt becomes dangerous when it grows faster than income, savings, and financial discipline.

How India Compares in National Household Debt Statistics: The Opportunity and the Warning

When people first examine National Household Debt Statistics, they often focus on countries with the highest debt levels.

That is usually the wrong approach.

The better question is:

Which countries are seeing debt grow faster than household incomes?

That question matters because debt becomes a problem when repayment capacity cannot keep pace.

India currently occupies a unique position in global National Household Debt Statistics.

Compared to many advanced economies, Indian households still carry relatively lower debt burdens.

However, India is also one of the fastest-growing consumer credit markets in the world.

That’s both an opportunity and a warning.

For investors, policymakers, and ordinary families, understanding this trend is becoming increasingly important.

National Household Debt Statistics and India’s Next Financial Transformation

India’s economy is changing rapidly.

Twenty years ago, many households avoided formal borrowing entirely.

Today, access to credit is easier than ever.

Consumers can obtain:

- Home loans online

- Instant personal loans

- Buy Now Pay Later financing

- Credit cards through mobile apps

- Vehicle financing within hours

This transformation is reshaping National Household Debt Statistics.

Credit access supports economic growth.

Families can purchase homes earlier.

Small business owners can expand operations.

Students can finance education.

However, easy credit also creates new risks.

History shows that every major debt cycle begins with a period when borrowing feels harmless.

The United States experienced this before 2008.

Several European economies experienced it after prolonged housing booms.

China experienced rapid household leverage growth during urbanisation.

India must learn from these experiences.

The goal is not to avoid debt.

The goal is to use debt intelligently.

The Theory

Economists often divide debt into two broad categories:

Productive Debt

Debt used to acquire assets or increase future earning power.

Examples:

- Home loans

- Education loans

- Business loans

Consumptive Debt

Debt used primarily for spending.

Examples:

- Credit card balances

- Vacation loans

- Lifestyle financing

- Consumer durable financing

The healthiest National Household Debt Statistics usually contain a higher proportion of productive debt.

The most vulnerable debt profiles often contain large amounts of high-interest consumer debt.

This distinction explains why two countries can have similar debt levels but dramatically different financial risks.

The Indian Reality: Four Families, Four Outcomes

Family 1: Suresh and Kavitha (Bengaluru)

Combined Income: ₹24 lakh

Debt:

| Type | Amount |

|---|---|

| Home Loan | ₹55 lakh |

| Credit Card Debt | ₹0 |

| Investments | ₹18 lakh |

Result:

Debt supports asset creation.

Long-term financial outlook remains healthy.

Family 2: Rohit and Sneha (Mumbai)

Combined Income: ₹20 lakh

Debt:

| Type | Amount |

| Personal Loan | ₹8 lakh |

| Credit Card Debt | ₹3 lakh |

| Investments | ₹1 lakh |

Result:

High-interest debt creates financial stress.

Wealth accumulation slows significantly.

Family 3: Imran and Ayesha (Hyderabad)

Combined Income: ₹16 lakh

Debt:

| Type | Amount |

| Education Loan | ₹6 lakh |

| Home Loan | ₹32 lakh |

| Investments | ₹6 lakh |

Result:

Borrowing supports future income growth.

Risk remains manageable.

Family 4: Vikram and Pooja (Delhi)

Combined Income: ₹22 lakh

Debt:

| Type | Amount |

| Car Loan | ₹15 lakh |

| Credit Card Debt | ₹5 lakh |

| Consumer Loans | ₹4 lakh |

Result:

Lifestyle debt absorbs future wealth creation.

Financial flexibility declines rapidly.

These examples demonstrate why National Household Debt Statistics should never be viewed in isolation.

The composition of debt matters more than the headline number.

IL Advisor: The ₹10 Lakh Mistake Nobody Notices

Let’s talk honestly.

Many Indian households celebrate when they qualify for bigger loans.

But qualification is not the same as affordability.

Suppose someone receives a salary increase from ₹12 lakh to ₹18 lakh.

The common response?

Upgrade:

- Bigger apartment

- Better car

- Premium credit cards

- More EMIs

The result:

Income rises.

Debt rises faster.

Net wealth barely changes.

Over twenty years, this behaviour can destroy crores of rupees in potential wealth creation.

That’s the uncomfortable reality hidden inside National Household Debt Statistics.

The biggest financial risk often isn’t unemployment.

It’s lifestyle inflation.

Hard Math: Debt vs Investing

Consider two households.

Household A

Invests ₹25,000 monthly.

Expected return assumption: 12%.

20-year future value:

Approx ₹2.5 crore.

Household B

Uses the same ₹25,000 for unnecessary EMIs.

Investment amount: ₹0.

20-year future value: ₹0.

| Monthly Cash Flow Use | Future Value (20 Years) |

| SIP Investment | ₹2.5+ crore |

| Lifestyle EMI | ₹0 |

The opportunity cost exceeds ₹2 crore.

This is why responsible debt management matters.

The consequences extend far beyond monthly payments.

What National Household Debt Statistics Suggest About the Future

Several trends deserve attention:

1. Housing Debt Will Continue Growing

Urbanisation supports long-term mortgage demand.

2. Consumer Credit Will Expand

Digital lending platforms are accelerating access.

3. Credit Quality Will Matter More

Not all borrowing is equal.

4. Financial Literacy Will Become Essential

Easy credit without education creates risk.

5. Debt Management Will Separate Wealth Builders from Wealth Destroyers

The future winners will not necessarily be the highest earners.

They will be the households that manage debt effectively.

Key Lessons for Indian Readers

When analysing National Household Debt Statistics, remember:

✔ Debt is a tool, not a strategy.

✔ Productive debt can build wealth.

✔ High-interest consumer debt destroys wealth.

✔ Income growth matters.

✔ Emergency funds matter.

✔ Financial discipline matters most.

The next decade will likely see household debt rise across India.

The families who understand these principles today will be better positioned to benefit from opportunities while avoiding the mistakes that have repeatedly appeared throughout global National Household Debt Statistics.

Further Reading

External Authority Sources

Internal InvestingLens Resources

Frequently Asked Questions About National Household Debt Statistics

1. What are National Household Debt Statistics?

National Household Debt Statistics measure the total amount of money households owe through mortgages, personal loans, vehicle loans, education loans, credit cards, and other consumer borrowing.

Governments, central banks, and international organizations use National Household Debt Statistics to assess financial stability, consumer spending patterns, and economic risks.

For investors, National Household Debt Statistics often serve as an early indicator of future economic conditions.

2. Why are National Household Debt Statistics important?

National Household Debt Statistics help policymakers understand whether households are becoming financially stronger or more vulnerable.

Rising debt isn’t automatically bad.

For example:

- A home loan that helps a family acquire a valuable asset can improve long-term wealth.

- High-interest credit card debt can weaken household finances.

This distinction makes National Household Debt Statistics an essential economic indicator.

3. Does India have high household debt compared to other countries?

Compared with many advanced economies, India’s household debt remains relatively lower.

Countries such as:

- Switzerland

- Australia

- Canada

- South Korea

- United States

typically report higher household debt burdens than India.

However, National Household Debt Statistics show that Indian consumer borrowing has been increasing rapidly, particularly in personal loans, unsecured lending, and digital credit products.

The key issue is not the current level.

The key issue is the speed of growth.

4. What is considered a safe debt-to-income ratio?

There is no universal rule.

However, many financial planners generally consider:

| Debt-to-Income Ratio | Interpretation |

|---|---|

| Below 35% | Comfortable |

| 35%–50% | Manageable |

| 50%–60% | Caution Required |

| Above 60% | Elevated Risk |

The most important lesson from National Household Debt Statistics is that debt should remain manageable even during economic stress.

5. Are home loans good debt?

Home loans are often considered productive debt because they finance a long-term asset.

However, even productive debt can become problematic if:

- EMI obligations become excessive

- Emergency savings are insufficient

- Income becomes unstable

National Household Debt Statistics consistently show that households with balanced debt structures tend to be more financially resilient.

6. How do rising interest rates affect household debt?

Higher interest rates increase borrowing costs.

For example:

A ₹50 lakh floating-rate home loan can experience a significant EMI increase when rates rise by just 1%.

When this happens across millions of households, National Household Debt Statistics can influence:

- Consumer spending

- Housing demand

- Savings rates

- Economic growth

This is why central banks closely monitor household leverage.

7. What is the biggest risk hidden inside National Household Debt Statistics?

The biggest risk is not debt itself.

The biggest risk is debt growing faster than income.

When households rely on:

- Credit cards

- Personal loans

- Buy Now Pay Later schemes

- Consumer financing

without corresponding income growth, financial vulnerability increases.

This pattern has appeared repeatedly throughout global National Household Debt Statistics history.

Conclusion: What National Household Debt Statistics Mean for Indian Families

The most important lesson from National Household Debt Statistics is surprisingly simple.

Debt is neither good nor bad.

Debt is a financial tool.

Used wisely, debt can help families purchase homes, fund education, and create long-term wealth.

Used carelessly, debt can quietly destroy decades of financial progress.

Throughout this analysis of National Household Debt Statistics, we saw a recurring pattern across countries, income levels, and economic cycles:

The households that succeed are not necessarily the highest earners.

They are the households that:

- Borrow responsibly

- Maintain emergency reserves

- Invest consistently

- Avoid excessive lifestyle inflation

- Keep debt growth below income growth

India remains in a relatively favorable position compared with many advanced economies.

However, rising consumer credit, digital lending, and easy access to financing mean that financial discipline will become increasingly important over the next decade.

Before taking on any new debt, ask yourself:

Will this liability increase my future wealth or simply increase my monthly expenses?

That one question can dramatically improve your financial decisions.

Suggested Reading

External Authority Sources:

Internal InvestingLens Resources:

Financial Disclaimer

This article is intended solely for educational and informational purposes.

The information presented regarding National Household Debt Statistics should not be considered financial, investment, tax, or legal advice.

Financial decisions should be made after considering your personal circumstances, risk tolerance, objectives, and consulting qualified professionals where appropriate.

Past trends in National Household Debt Statistics do not guarantee future outcomes.

Author Bio

Mahesh Reddy is a personal finance educator and founder contributor at InvestingLens, focused on helping Indians make smarter decisions about money, debt, investing, and financial freedom. He writes practical, no-fluff financial content designed for real middle-class Indian households.