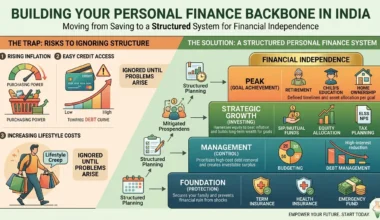

Build or Restore an Emergency Fund Before the Next Financial Shock Hits

Introduction

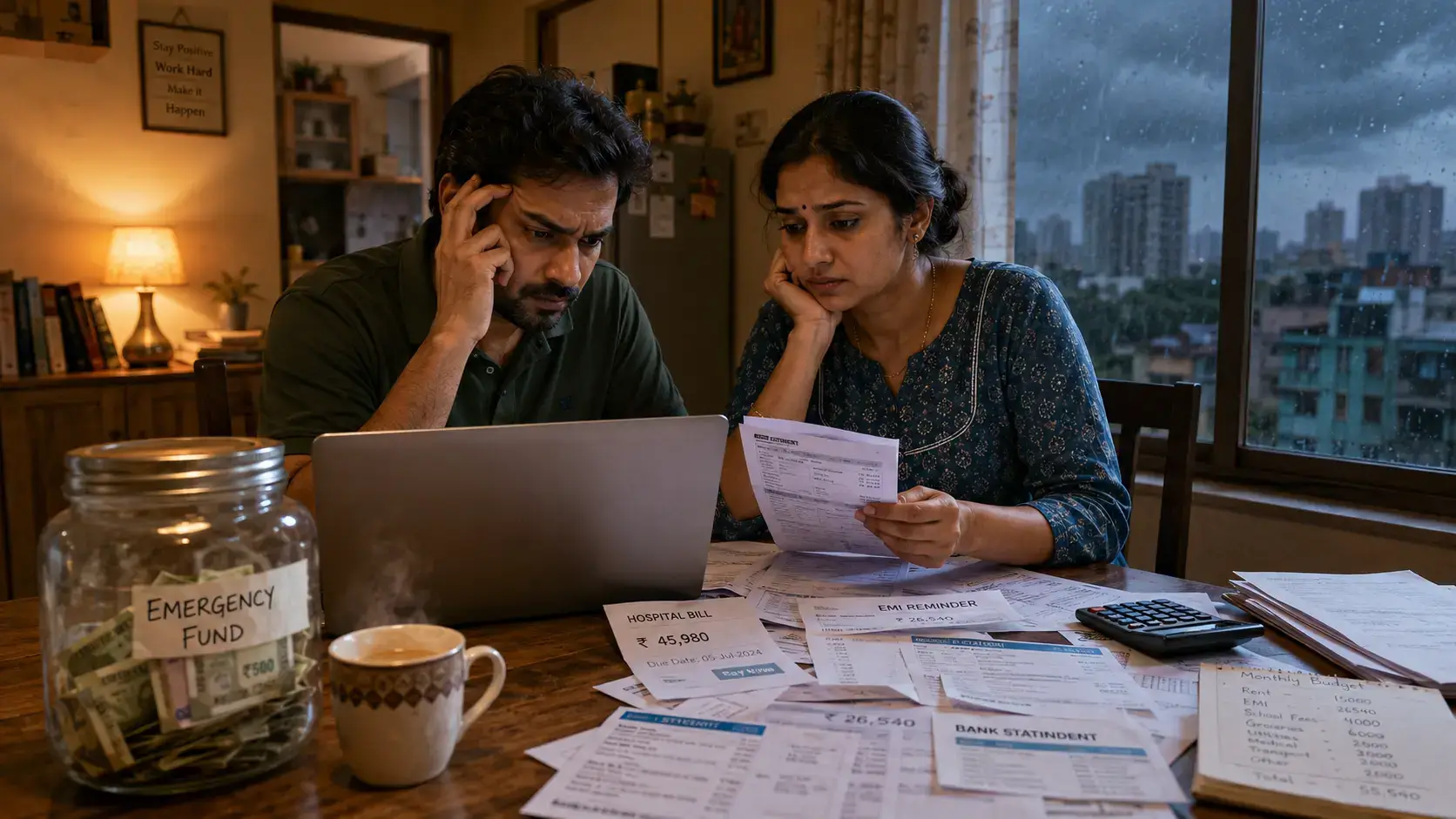

One medical emergency.

One layoff email.

One family crisis.

That’s all it takes to destroy years of financial stability if you don’t have emergency savings.

Most Indians don’t realize this until the damage is already done.

A broken bike engine becomes a credit card EMI.

A hospital bill turns into a personal loan at 16% interest.

A job loss wipes out mutual fund investments meant for long-term wealth.

Here’s the uncomfortable truth:

If your financial survival depends on next month’s salary, you are financially fragile.

And no — owning the latest iPhone on EMI while keeping Rs. 3,000 in your savings account is not “doing well.”

This guide will show you exactly how to build or restore an emergency fund in India using practical steps, real salary examples, and realistic savings systems that actually work. No motivational nonsense. No fake “save 50% of your salary” advice.

Just real money survival planning.

Key Takeaways

- An emergency fund protects you from debt traps and financial panic.

- Ideally, Indians should save 3–12 months of expenses depending on job stability.

- Start small if needed — even Rs. 500 daily habits matter.

- Don’t keep emergency savings inside risky investments.

- Rebuilding an emergency fund after job loss is possible with aggressive expense control.

- Lifestyle inflation is one of the biggest reasons people fail financially despite good salaries.

What Is an Emergency Fund?

An emergency fund is money kept aside purely for financial survival.

Not vacations.

Not gadgets.

Not IPL betting apps.

Not wedding shopping.

This money exists for situations like:

- Job loss

- Medical emergencies

- Family emergencies

- Urgent home repairs

- Sudden business losses

- Salary delays

Think of it as financial oxygen.

You only understand its importance when life punches you in the face unexpectedly.

And trust me — it eventually does.

Why Most Indians Still Don’t Have One

Let’s be brutally honest.

The problem is rarely income alone.

It’s behavior.

Many salaried Indians, even those earning a respectable Rs. 60,000 to Rs. 1.2 lakh monthly, still find themselves caught in a paycheck-to-paycheck cycle, largely because of::

- EMI addiction

- Lifestyle inflation

- Credit card misuse

- Food delivery overspending

- “YOLO” spending culture

- Zero budgeting discipline

Here’s a real-world example.

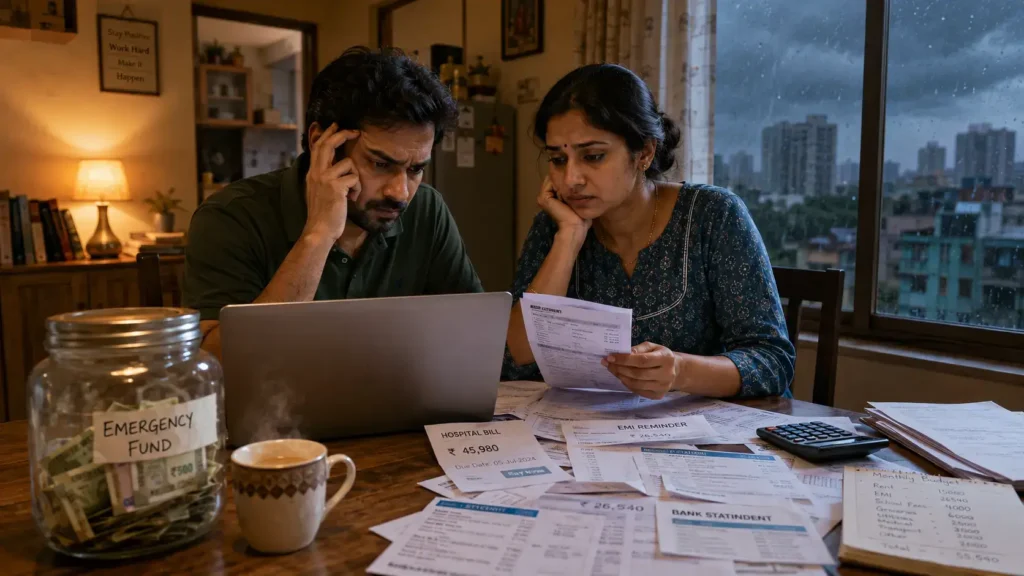

Ravi’s Financial Disaster

Ravi, a software employee based in Hyderabad, commanded a respectable monthly salary of Rs. 95,000. For many, this income level suggests a comfortable financial position, ample enough to build substantial savings and investments. However, as Ravi’s story tragically illustrates, a high salary alone doesn’t guarantee financial security if not managed with discipline.

Sounds decent, right?

But his monthly fixed commitments looked like this:

| Expense | Amount |

|---|---|

| Car EMI | Rs. 18,000 |

| Credit Card EMI | Rs. 11,000 |

| Rent | Rs. 22,000 |

| Swiggy/Zomato | Rs. 8,500 |

| Gadgets EMI | Rs. 6,000 |

| Weekend Spending | Rs. 10,000 |

Savings left?

Almost nothing.

Then layoffs hit his company.

Within 45 days:

- Credit card dues exploded

- CIBIL score dropped

- Personal loan taken at high interest

- Investments redeemed at loss

This is exactly why you need to build or restore an emergency fund before life becomes expensive.

How Much Emergency Fund Do You Actually Need?

There’s no one-size-fits-all number.

Your emergency savings target depends on:

- Job stability

- Family responsibilities

- Existing loans

- Health conditions

- Dependents

- Business volatility

General Rule for Indians

| Situation | Emergency Fund Target |

|---|---|

| Single salaried employee | 3–6 months expenses |

| Married with kids | 6–12 months |

| Business owner/freelancer | 12 months |

| Single income household | 9–12 months |

Simple Emergency Fund Calculation

Let’s say Priya’s monthly survival expenses are:

| Expense | Amount |

|---|---|

| Rent | Rs. 18,000 |

| Groceries | Rs. 10,000 |

| Utilities | Rs. 4,000 |

| EMI | Rs. 12,000 |

| Insurance | Rs. 3,000 |

| Transport | Rs. 5,000 |

Total = Rs. 52,000 monthly

For 6 months:

52000×6=312000

Priya should ideally maintain around Rs. 3.1 lakh as emergency savings.

Not in stocks.

Not in crypto.

Not in “double money” Telegram schemes.

Liquid. Accessible. Safe.

Step-by-Step Plan to Build an Emergency Fund

1. Stop Pretending Every Expense Is “Necessary”

This is where most people fail.

Netflix, premium phones, impulsive Amazon shopping, expensive cafés — these are lifestyle choices, not essentials.

If you genuinely want to build or restore an emergency fund, you need temporary discomfort.

There’s no shortcut.

2. Start With a Small Survival Goal

Don’t obsess over Rs. 10 lakh immediately.

Start with:

- Rs. 10,000

- Then Rs. 50,000

- Then 1 month expenses

- Then 3 months

- Then 6 months

Momentum matters more than perfection.

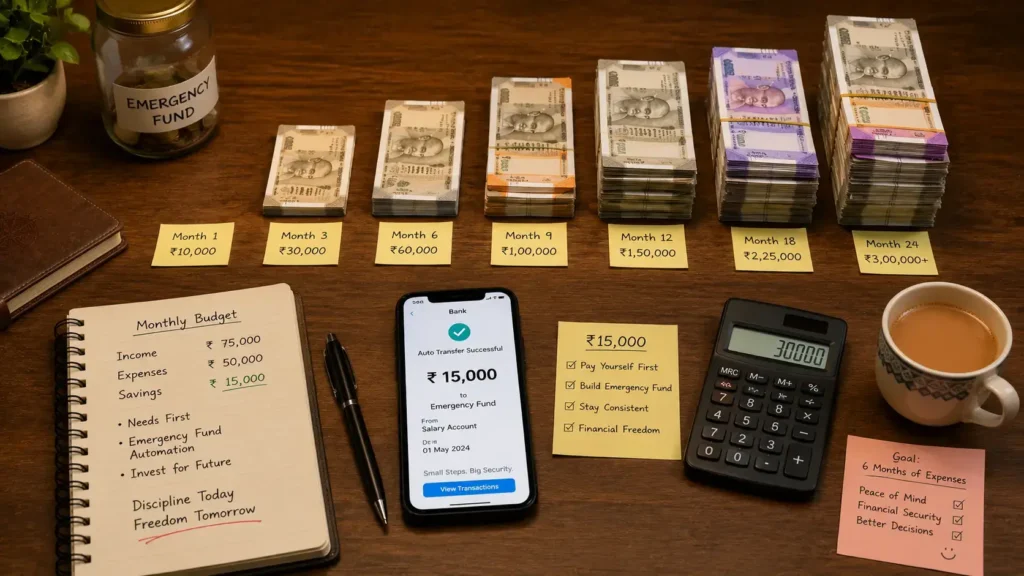

3. Automate Savings Immediately

The best emergency fund system is invisible.

Set an automatic transfer the same day salary arrives.

Example:

- Salary date: 1st

- Auto-transfer to emergency account: 2nd

Even Rs. 5,000 monthly builds discipline.

4. Use Windfalls Smartly

When Indians receive:

- Bonus

- Tax refund

- Freelance income

- Incentives

- Gifts

Most immediately upgrade lifestyle.

That’s exactly backwards.

Use at least 50% of windfall income to build emergency savings first.

5. Cut One Financial Leak Aggressively

You don’t need to suffer everywhere.

Just kill one major leak.

Examples:

- Rs. 7,000 monthly food delivery

- Rs. 15,000 unnecessary car EMI

- Rs. 4,000 unused subscriptions

That single correction can accelerate emergency fund growth massively.

How to Restore an Emergency Fund After Using It

This part matters because many people use emergency savings correctly… then never rebuild it.

That’s dangerous.

Mahesh’s Scenario

Mahesh used Rs. 2.8 lakh during his father’s surgery.

Good use of emergency money.

But afterward, he relaxed financially again.

Big mistake.

Because emergencies don’t arrive one at a time politely.

Emergency Fund Restoration Timeline

| Timeline | Action |

|---|---|

| First 30 days | Pause luxury spending |

| First 60 days | Redirect bonuses/increments |

| 3–6 months | Restore at least 50% corpus |

| 6–12 months | Fully rebuild emergency fund |

Treat rebuilding like recovering from a financial injury.

Because that’s exactly what it is.

Where Should You Keep Emergency Savings?

This is critical.

Emergency money should prioritize:

- Safety

- Liquidity

- Accessibility

Not maximum returns.

Good Places for Emergency Funds

- High-interest savings account

- Sweep-in FD

- Liquid mutual funds

- Short-term fixed deposits

Bad Places

- Stocks

- Crypto

- Real estate

- ULIPs

- Friend’s business

- Chit funds without regulation

If your emergency money falls 35% during a stock market crash exactly when you need it, that defeats the purpose.

Biggest Emergency Fund Mistakes Indians Make

Using Credit Cards as Emergency Funds

A credit card is debt.

Not savings.

There’s a massive difference.

Paying 36% annualized interest after emergencies can destroy years of progress.

Know More About What Is Debt Consolidation? Stop Paying 36% Interest on Credit Cards in India

Investing Before Building Safety

People rush into:

- Options trading

- Crypto

- penny stocks

…while having zero emergency reserve.

That’s financial gambling, not investing.

Mixing Emergency Money With Spending Account

If emergency savings sits beside your daily UPI account, you’ll slowly “borrow” from yourself.

And usually never repay it.

Separate account. Always.

Ignoring Inflation

Your emergency fund should grow over time.

A Rs. 3 lakh corpus today may not cover the same expenses five years later.

Review yearly.

Real Indian Scenarios

Scenario 1: Job Loss

An IT employee in Bengaluru loses his job during layoffs.

Without emergency savings:

- Uses credit cards

- Misses EMI payments

- CIBIL score damaged

With 6 months emergency fund:

- Pays rent calmly

- Continues SIPs selectively

- Finds better opportunity without panic

Huge difference.

Scenario 2: Medical Emergency

Priya’s mother needed urgent hospitalization costing Rs. 2.4 lakh.

Without emergency savings:

- Gold loan

- Family borrowing

- Financial stress

With emergency corpus:

- Immediate treatment

- No high-interest debt

- Faster emotional recovery

Scenario 3: Business Slowdown

A freelance designer from Pune loses clients for 4 months.

Because he had 8 months emergency savings:

- No panic selling investments

- No borrowing

- No desperate low-paying work

That’s what financial resilience looks like.

FAQs

How much should Indians ideally keep in an emergency fund?

Most salaried Indians should aim for 3–6 months of expenses. Business owners or freelancers may need 9–12 months.

Can I invest my emergency fund in mutual funds?

Only partially in highly liquid, low-risk options like liquid funds. Emergency savings should not be heavily exposed to market volatility.

Should I build or restore an emergency fund before investing?

Usually yes. Building financial safety before aggressive investing prevents panic selling and debt traps.

Is FD good for emergency funds in India?

Yes. Sweep-in FDs and short-term deposits can work well because they offer liquidity and relatively stable returns.

What if I can only save Rs. 2,000 monthly?

Start anyway.

Consistency matters more than ego.

Many people earning lakhs still have zero savings because discipline beats income alone.

Final Thoughts

To build or restore an emergency fund is not exciting.

Nobody posts Instagram reels celebrating:

“Finally saved six months of expenses.”

But this single financial habit can protect your:

- Mental peace

- Family stability

- Credit score

- Investments

- Future opportunities

The people who survive financial crises calmly are usually not the smartest investors.

They’re the most prepared.

And here’s the hard truth:

A luxury lifestyle built on zero savings is fake wealth.

Real wealth is sleeping peacefully knowing one emergency won’t destroy your life.

Disclaimer: This article is for educational purposes only and should not be considered personalized financial advice. Please consult a SEBI-registered financial advisor before making major financial decisions.

Author Bio

Mahesh Reddy

Mahesh Reddy is the founder of InvestingLens.com, where he writes practical, brutally honest personal finance content focused on Indian households. His work simplifies investing, saving, budgeting, and financial survival strategies for everyday Indians trying to build long-term wealth without falling into debt traps.