Debt Consolidation for Bad Credit: A Realistic Indian Survival Guide for 2026

Introduction

Debt Consolidation for Bad Credit is often marketed as a magic solution. It isn’t. But for many Indian families drowning in multiple EMIs, credit card bills, and app-based loans, Debt Consolidation for Bad Credit can be the difference between financial recovery and years of stress.

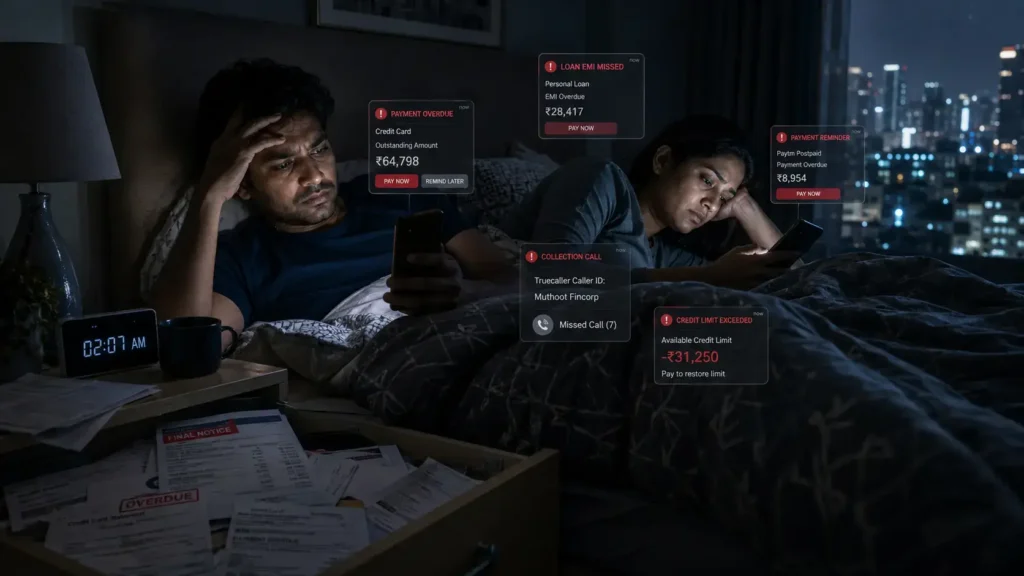

If your CIBIL score is below 650, collection calls have started, and every salary credit disappears within 48 hours, this guide is for you. Not to sell false hope. To show what actually works in India in 2026.

The reality is brutal. Many middle-class Indians are juggling:

- Credit card debt at 30%-46% annualized rates

- Personal loans from multiple NBFCs

- Buy Now Pay Later obligations

- Salary advances

- Consumer durable EMIs

According to TransUnion CIBIL, credit scores generally range between 300 and 900, with higher scores indicating stronger creditworthiness.

The problem? Most people try to fix debt emotionally instead of mathematically.

That’s where Debt Consolidation for Bad Credit enters the conversation.

Key Takeaways

Quick Summary

- Debt consolidation combines multiple debts into one repayment structure.

- Debt Consolidation for Bad Credit works best when interest rates actually reduce.

- A low CIBIL score doesn’t automatically disqualify you.

- RBI-regulated banks and NBFCs should always be preferred over unregulated loan apps.

- Paying only minimum credit card dues can become financially destructive.

- Debt Consolidation for Bad Credit is a tool, not a cure.

- Without spending control, consolidation simply creates a larger future problem.

- Debt settlement and debt consolidation are not the same thing.

- A recovery plan should include CIBIL rebuilding and emergency fund creation.

External Sources:

Internal Links:

What Is Debt Consolidation for Bad Credit and Why Indians Are Suddenly Searching for It

The theory sounds simple.

You have:

- Credit Card 1 = ₹85,000

- Credit Card 2 = ₹60,000

- Personal Loan = ₹2,40,000

- Consumer Loan = ₹55,000

Instead of paying four lenders, you combine everything into a single repayment plan.

That’s the basic idea behind Debt Consolidation for Bad Credit.

But here’s where most YouTube finance influencers stop.

The real question isn’t whether consolidation is possible.

The real question is:

Does the math actually improve your situation?

Indian Reality: Rahul’s ₹4.4 Lakh Debt Disaster

Rahul, a 34-year-old software tester from Hyderabad, earned ₹72,000 monthly.

On paper, he looked financially stable.

Then life happened.

- Father’s hospitalisation: ₹1.2 lakh

- Wedding expenses: ₹1.8 lakh

- Credit card spending during COVID recovery

- Two personal loans

Within three years:

| Debt Type | Outstanding |

|---|---|

| HDFC Credit Card | ₹1,10,000 |

| SBI Credit Card | ₹78,000 |

| Personal Loan | ₹2,10,000 |

| Consumer Loan | ₹42,000 |

Total debt:

₹4,40,000

Minimum monthly obligations:

₹28,700

Salary after PF and taxes:

₹62,000

Half his income vanished before groceries.

This is where Debt Consolidation for Bad Credit became relevant.

His CIBIL score had fallen below 640 due to delayed payments.

Most banks rejected him.

But one RBI-regulated NBFC approved a secured consolidation loan because his family owned a small plot.

Result:

| Before | After |

|---|---|

| 4 EMIs | 1 EMI |

| ₹28,700/month | ₹15,900/month |

| Multiple penalties | Fixed repayment |

| Constant stress | Manageable cash flow |

Notice something important.

The debt didn’t disappear.

The structure improved.

That’s what good Debt Consolidation for Bad Credit actually does.

IL Advisor Warning

Most Indians make this fatal mistake:

They consolidate debt.

Then they start spending again.

Six months later:

- Old debt replaced

- New credit card debt created

- Total liabilities increase

I’ve seen families convert ₹3 lakh debt into ₹7 lakh debt simply because they treated consolidation as permission to spend again.

Debt doesn’t start in the bank account.

It starts in behavior.

The Hard Math Nobody Shows You

Suppose:

| Item | Amount |

|---|---|

| Credit Card Debt | ₹2,00,000 |

| Interest Rate | 42% p.a. |

| Monthly Interest | 3.5% |

If only minimum dues are paid:

The effective repayment period can stretch for years.

A ₹2 lakh balance can ultimately cost several lakhs in interest depending on repayment behavior and revolving charges. RBI repeatedly requires transparent disclosure of annualized rates and minimum due structures because of this risk.

Now compare:

| Option | Interest |

|---|---|

| Credit Card | 36%-46% |

| Consolidation Loan | 13%-20% |

That gap is where Debt Consolidation for Bad Credit creates value.

Who Should Consider Debt Consolidation for Bad Credit?

You may qualify if:

- CIBIL score is between 550 and 700

- Income is stable

- Debt is spread across multiple lenders

- You have repayment capability

You should avoid it if:

- You continue adding fresh debt

- Income is unstable

- You already defaulted heavily

- You want a quick fix without behavioral changes

External Sources:

Internal Links:

Debt Consolidation for Bad Credit in India: Available Options in 2026

This is where things become practical.

Most articles discuss Debt Consolidation for Bad Credit like a textbook concept.

Let’s discuss what actually exists in India right now.

Option 1: Personal Loan for Debt Consolidation

This is the most common route.

You borrow one larger loan.

Then close:

- Credit cards

- Small loans

- BNPL balances

Advantages:

- Single EMI

- Lower interest

- Better planning

Disadvantages:

- Low CIBIL may cause rejection

- Higher rates for risky borrowers

Indian Case Study: Priya From Pune

Salary: ₹95,000

Debt:

| Type | Amount |

|---|---|

| Credit Cards | ₹1,70,000 |

| Personal Loan | ₹1,20,000 |

| BNPL | ₹35,000 |

Total:

₹3,25,000

CIBIL:

665

She obtained a consolidation loan at 15.75%.

Monthly savings:

Approximately ₹8,400.

More importantly:

Cash-flow pressure disappeared.

That breathing room prevented future defaults.

This is how successful Debt Consolidation for Bad Credit works.

Option 2: Loan Against Property

For homeowners, this is often the cheapest route.

Interest rates are typically lower than unsecured personal loans.

But the risk is obvious.

You are placing an asset on the line.

IL Advisor Warning

Never pledge family property to consolidate lifestyle spending unless repayment ability is crystal clear.

I’ve seen a ₹6 lakh card problem become a ₹40 lakh property risk.

That is not financial planning.

That is gambling.

Option 3: Balance Transfer Programs

Some banks offer:

- Lower introductory rates

- Transfer of existing card balances

Useful?

Yes.

Dangerous?

Also yes.

Many borrowers forget promotional rates expire.

Then interest jumps again.

Option 4: Debt Management Programs

These involve:

- Negotiation

- Restructuring

- Payment planning

Often useful when Debt Consolidation for Bad Credit loans are unavailable.

However, always verify the provider.

Stick with regulated institutions and legitimate financial entities.

Check regulatory information through:

Understanding the CIBIL Reality

Many Indians panic when they hear:

“Your CIBIL score is only 620.”

Let’s add perspective.

TransUnion CIBIL scores generally range from 300 to 900. Higher scores improve approval odds, but approval decisions also depend on income, repayment capacity, employment stability, and lender policies.

That means Debt Consolidation for Bad Credit remains possible even if your score isn’t perfect.

The Debt Consolidation Checklist

Before applying:

Ask Question #1

Will my interest rate reduce?

If not, don’t proceed.

Ask Question #2

Will my monthly cash flow improve?

If not, don’t proceed.

Ask Question #3

Am I closing old credit lines responsibly?

If not, don’t proceed.

Ask Question #4

Can I avoid new debt for 12 months?

If not, consolidation may fail.

Hard Math Example

Current Situation:

| Debt | Amount | Rate |

|---|---|---|

| Card A | ₹1,20,000 | 42% |

| Card B | ₹80,000 | 39% |

| Loan | ₹1,50,000 | 19% |

Total:

₹3,50,000

Weighted cost:

Approximately 31%+

Consolidation loan:

15%

Potential interest savings become substantial over the repayment period.

This is why Debt Consolidation for Bad Credit remains one of the few financial strategies that can create immediate cash-flow improvement when executed correctly.

Final IL Advisor Reality Check

No lender can rescue a spending problem.

Not RBI.

Not CIBIL.

Not a debt consultant.

Not a bank manager.

If monthly expenses exceed income, Debt Consolidation for Bad Credit only delays the explosion.

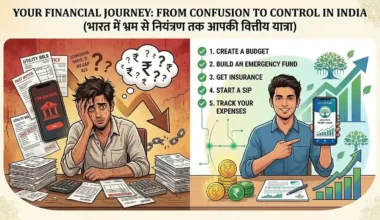

Real recovery requires:

- Budget discipline

- Emergency savings

- Credit rebuilding

- Consistent EMI payments

Only then does consolidation become a wealth-preserving tool instead of another financial trap.

External Sources:

Internal Links:

How Debt Consolidation for Bad Credit Affects Your CIBIL Score, Mental Health, and Long-Term Wealth

Most Indians think Debt Consolidation for Bad Credit is only about reducing EMIs.

That’s incomplete thinking.

The deeper impact is psychological.

When someone has:

- 5 overdue bills

- 3 collection calls daily

- Credit card penalties

- Salary disappearing instantly

their brain stops making rational financial decisions.

They start surviving month-to-month.

That’s where debt destroys wealth quietly.

The Hidden Mental Cost of Multiple Debts

Let’s take the example of Sneha and Arvind from Bengaluru.

Combined monthly income:

₹1.42 lakh.

On Instagram?

Perfect life.

Reality?

| Debt Type | Outstanding |

|---|---|

| 3 Credit Cards | ₹3.1 lakh |

| Personal Loan | ₹4.4 lakh |

| Car Loan | ₹6.8 lakh |

| Consumer EMIs | ₹72,000 |

Total obligations:

Nearly ₹31,000 monthly.

Their biggest problem wasn’t the amount.

It was unpredictability.

Different due dates.

Different penalties.

Different interest rates.

Different collection calls.

That’s the silent advantage of Debt Consolidation for Bad Credit.

It simplifies decision-making.

And simplified finances improve survival probability.

The Indian Reality Nobody Talks About

Indian middle-class households are under pressure from three directions simultaneously:

- Inflation

- Lifestyle creep

- Easy digital credit

Food delivery apps normalized overspending.

BNPL normalized future borrowing.

Credit cards normalized minimum dues.

Then one emergency arrives.

Everything collapses.

According to RBI financial awareness campaigns, borrowers should understand annualized borrowing costs and repayment obligations clearly before taking retail credit. (RBI Financial Education)

But most borrowers never calculate true interest.

That’s why Debt Consolidation for Bad Credit becomes attractive later — usually after damage has already happened.

IL Advisor Section: The ₹7 Lakh “Lifestyle EMI” Trap

Here’s a hard truth.

Many debts are not emergencies.

They’re lifestyle subscriptions.

- ₹1,800 Zomato habit

- ₹4,500 shopping EMI

- ₹2,000 gadgets

- ₹3,000 weekend outings

- ₹7,000 “reward points” credit card spending

Individually harmless.

Collectively devastating.

I’ve seen salaried employees earning ₹85,000 end up with ₹9 lakh unsecured debt because they confused affordability with EMI eligibility.

Banks approve based on probability.

You must spend based on survival.

That’s the difference.

How Debt Consolidation for Bad Credit Impacts CIBIL Score

Now let’s discuss the big fear.

“Will Debt Consolidation for Bad Credit damage my credit score?”

Short answer:

It depends on behavior after consolidation.

It Can Improve Your Score If:

- EMIs are paid on time

- Credit utilization reduces

- Old defaults stop growing

- Multiple overdue accounts close

It Can Hurt Your Score If:

- You miss new EMIs

- You apply for too many loans

- You continue credit card spending

- You enter debt settlement aggressively

According to TransUnion CIBIL, payment history is one of the largest contributors to credit score calculations. (TransUnion CIBIL)

That means repayment discipline after Debt Consolidation for Bad Credit matters more than the consolidation itself.

Hard Math: Credit Card Minimum Due Disaster

Suppose you owe:

₹1,50,000 on a card.

Interest:

3.5% monthly.

Minimum due:

5%.

Looks manageable.

But here’s the trap.

| Month | Approx Balance |

|---|---|

| Start | ₹1,50,000 |

| After Interest Cycle | ₹1,55,250 |

| After Minimum Payment | Debt Still Massive |

The debt barely moves.

Over years, borrowers may repay multiple times the original principal depending on revolving balances and penalty structures.

This is exactly why Debt Consolidation for Bad Credit can mathematically reduce financial damage.

Debt Consolidation vs Debt Settlement

Huge difference.

Many Indians confuse the two.

| Debt Consolidation | Debt Settlement |

|---|---|

| Combines debts | Negotiates reduced repayment |

| Usually less damaging | Often damages CIBIL badly |

| Focus on structured repayment | Focus on partial closure |

| Better for moderate distress | Used in severe distress |

Settlement should generally be a last resort.

Especially if future home loans matter.

The Family Impact Nobody Measures

Financial stress changes behavior.

- Couples fight more

- Sleep quality drops

- Career risks increase

- Health expenses rise

A clean repayment structure through Debt Consolidation for Bad Credit often restores emotional stability before wealth stability.

That matters.

A lot.

When Debt Consolidation for Bad Credit Is a Bad Idea

Avoid it if:

- You are unemployed

- Your EMI-to-income ratio already exceeds 60%

- You have gambling habits

- You continue lifestyle overspending

- You’re hiding debt from family

Consolidation without behavioral change is like treating diabetes while drinking cola daily.

Temporary relief.

Permanent damage.

Practical Recovery Blueprint for Indians

Month 1

- Stop fresh credit usage

- Track every rupee

- Build survival budget

Month 2

- Consolidate high-interest debt

- Automate EMIs

- Close unnecessary BNPL accounts

Month 3–6

- Create ₹50,000 emergency buffer

- Improve repayment consistency

- Reduce credit utilization below 30%

Month 6–18

- Rebuild CIBIL

- Increase SIP investments gradually

- Avoid lifestyle inflation

That’s how Debt Consolidation for Bad Credit becomes a recovery strategy instead of a temporary patch.

External Sources:

Internal Links:

The 9-Layer Transformation Story: How One Indian Family Escaped ₹11 Lakh Debt Using Debt Consolidation for Bad Credit

1. Status Quo

Vikram and Pooja from Chennai looked financially successful.

Combined salary:

₹1.78 lakh monthly.

Apartment EMI.

SUV loan.

International vacation EMI.

Three premium credit cards.

Everything looked fine until inflation and layoffs hit simultaneously.

Within 14 months:

| Liability | Outstanding |

|---|---|

| Credit Cards | ₹4.2 lakh |

| Personal Loans | ₹3.8 lakh |

| Car Loan | ₹2.5 lakh |

| Consumer EMIs | ₹65,000 |

Total debt:

₹11 lakh+.

2. Trigger

Vikram’s bonus disappeared during company restructuring.

Then Pooja required surgery costing ₹2.2 lakh.

Emergency savings?

Only ₹18,000.

That’s when minimum dues started.

The financial spiral began.

3. Mistake

Instead of reducing expenses immediately, they maintained appearances.

Weekend dining.

Online shopping.

School upgrades.

EMI mentality continued.

This is where most Indian families lose control.

Not because of one catastrophe.

Because they refuse to downgrade lifestyle early.

4. Wake-Up Call

Collection agents started calling relatives.

One credit card crossed 90+ DPD.

CIBIL score crashed below 620.

A planned home upgrade loan was rejected.

That humiliation changed everything.

5. IL Advisor

Here’s the uncomfortable truth.

The problem wasn’t low income.

The problem was emotional spending.

Middle-class Indians often spend to signal stability.

Not because they can afford it.

That behavior turns temporary debt into long-term financial imprisonment.

6. Calculation

A financial planner showed them the real numbers.

Existing Situation

| Category | Monthly Outflow |

|---|---|

| Credit Card Minimums | ₹29,000 |

| Personal Loans | ₹21,000 |

| Car EMI | ₹13,500 |

| Consumer EMIs | ₹6,800 |

Total:

₹70,300 monthly.

After Debt Consolidation for Bad Credit

Using a secured consolidation structure:

| Category | Monthly EMI |

|---|---|

| Consolidated EMI | ₹38,500 |

Monthly relief:

₹31,800.

That breathing room prevented future defaults.

7. Pivot

They implemented strict rules:

- No fresh credit cards

- Switched to UPI cash budgeting

- Sold unused electronics

- Paused vacations

- Built emergency fund first

Most importantly:

They stopped pretending to be richer than they were.

8. Result

Within 24 months:

- CIBIL recovered above 720

- Emergency fund crossed ₹3 lakh

- SIP investments restarted

- Stress reduced dramatically

That’s the real success story of Debt Consolidation for Bad Credit.

Not instant freedom.

Structured recovery.

9. Lesson

Debt consolidation does not create wealth.

Behavior change does.

But Debt Consolidation for Bad Credit can create the breathing room necessary for behavior change to actually happen.

That distinction matters more than any bank advertisement.

External Sources:

Internal Links:

Frequently Asked Questions About Debt Consolidation for Bad Credit

1. Can I get Debt Consolidation for Bad Credit with a CIBIL score below 650?

Yes, in many cases you can. Several RBI-regulated NBFCs and banks evaluate more than just your CIBIL score. They may also consider:

- Monthly salary

- Job stability

- Existing repayment history

- Secured collateral

- Banking transactions

However, lower credit scores usually mean:

- Higher interest rates

- Lower approved loan amounts

- Stricter repayment conditions

This is why Debt Consolidation for Bad Credit works best when combined with disciplined budgeting and consistent EMI repayment.

According to TransUnion CIBIL, payment consistency plays a major role in credit score recovery. (TransUnion CIBIL)

2. Does Debt Consolidation for Bad Credit reduce total debt?

No.

This is one of the biggest myths in India.

Debt Consolidation for Bad Credit does not erase debt automatically. It restructures debt into a simpler repayment format.

Benefits usually include:

- Lower interest rates

- Single EMI

- Better cash flow

- Reduced penalties

- Easier repayment tracking

But if overspending continues, total debt can actually increase.

3. Is Debt Consolidation for Bad Credit better than debt settlement?

Usually yes — especially for salaried Indians trying to protect future loan eligibility.

| Debt Consolidation | Debt Settlement |

|---|---|

| Structured repayment | Negotiated partial closure |

| Lower long-term damage | Higher CIBIL damage |

| Better for future loans | Used in severe distress |

| Focuses on repayment | Focuses on negotiation |

Debt settlement may affect future approvals for:

- Home loans

- Car loans

- Business loans

That’s why Debt Consolidation for Bad Credit is often safer for long-term financial recovery.

4. How long does Debt Consolidation for Bad Credit take to improve CIBIL score?

Typically:

- Minor improvement: 3–6 months

- Strong recovery: 12–24 months

Factors affecting recovery include:

- EMI payment consistency

- Credit utilization ratio

- Number of active accounts

- Fresh loan inquiries

- Existing defaults

One EMI paid on time consistently is often better than juggling five delayed payments.

5. What is the biggest mistake people make after Debt Consolidation for Bad Credit?

Simple.

They start using credit cards again.

This destroys the entire purpose of consolidation.

The smartest borrowers:

- Freeze unnecessary cards

- Reduce lifestyle spending

- Build emergency savings

- Avoid BNPL usage

- Focus on rebuilding financial stability

The goal is not just lower EMI.

The goal is permanent financial control.

Conclusion: Debt Consolidation for Bad Credit Is a Tool — Not a Miracle

Let’s end with the truth most finance influencers avoid saying.

Debt Consolidation for Bad Credit offers a vital lifeline for Indian families grappling with overwhelming financial pressure. When implemented strategically, it can transform a chaotic landscape of multiple high-interest debts – like credit card balances, personal loans, and BNPL obligations – into a single, more manageable repayment structure. This simplification often leads to a significantly reduced monthly EMI and a lower overall interest burden, thereby freeing up critical cash flow. Beyond the immediate financial relief, successful consolidation provides the psychological breathing room necessary to break the cycle of debt, enabling families to regain control, reduce stress, and focus on rebuilding their financial health through disciplined spending and consistent repayment.

But it only works when:

- spending behavior changes,

- repayment discipline improves,

- and lifestyle inflation stops.

A consolidation loan cannot fix emotional spending.

It cannot replace emergency savings.

It cannot solve income instability.

But it can create breathing room.

This crucial breathing room, achieved through a strategic debt consolidation, isn’t just about lower EMIs; it’s about restoring mental peace and enabling families to make rational financial decisions. It provides the necessary space to implement a sustainable budget, build an emergency fund, and address the root causes of their debt, transforming a cycle of stress into a pathway for genuine recovery and preventing a complete financial collapse.

If you are considering Debt Consolidation for Bad Credit, focus on these priorities first:

- Reduce high-interest debt immediately.

- Avoid unregulated loan apps.

- Build a survival budget.

- Create emergency savings.

- Rebuild CIBIL patiently.

Most importantly:

Never confuse approval eligibility with affordability.

That single mindset shift can save lakhs over your lifetime.

Financial Disclaimer

This article is for educational purposes only and should not be considered personalized financial advice. Loan approvals, interest rates, and repayment outcomes vary based on individual circumstances, lender policies, and market conditions. Always verify terms with RBI-regulated financial institutions before making borrowing decisions.

External Sources:

Internal Links:

Author Bio

Mahesh Reddy is a personal finance educator and founder contributor at InvestingLens, focused on helping Indians make smarter decisions about money, debt, investing, and financial freedom. He writes practical, no-fluff financial content designed for real middle-class Indian households.